PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851636

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851636

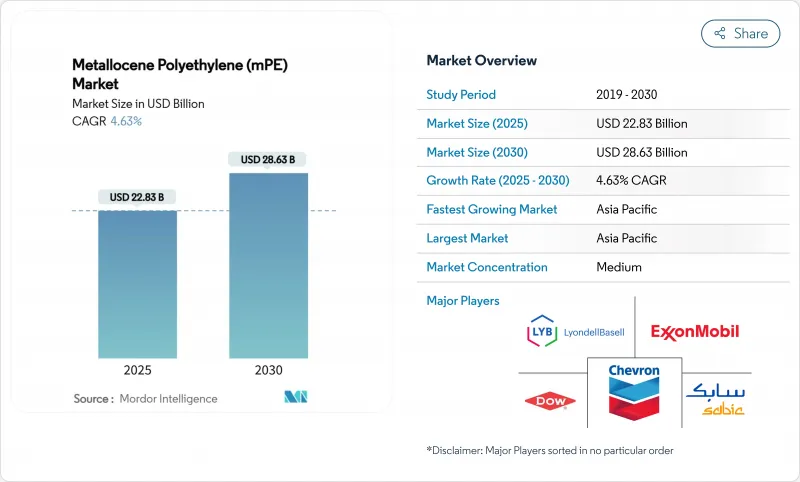

Metallocene Polyethylene (mPE) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Metallocene Polyethylene Market size is estimated at USD 22.83 billion in 2025, and is expected to reach USD 28.63 billion by 2030, at a CAGR of 4.63% during the forecast period (2025-2030).

Robust demand for high-clarity down-gauged films, the scale-up of solar panel encapsulant lines, and modernization in agriculture sustain this growth path. Producers benefit from single-site catalyst technology that yields narrow molecular weight distribution, enabling consistent mechanical strength and superior optical properties at lower gauges. China's ethylene capacity additions, India's e-commerce boom, and capacity investments in the Middle East together reinforce upstream supply security, while ongoing shifts toward circular plastics keep strategic focus on advanced recycling and bio-based feedstocks. The Metallocene polyethylene market therefore marries performance gains with sustainability objectives and positions itself as a core enabler of next-generation flexible packaging solutions.

Global Metallocene Polyethylene (mPE) Market Trends and Insights

Rising Demand for High-Clarity, Down-Gauged Packaging Films

Converters continue to migrate toward thinner films that preserve mechanical integrity, and single-site catalysts facilitate uniform comonomer distribution that yields clarity alongside dart impact strength. Typical gauge reductions of 15-20% lower material use and carbon intensity, directly supporting brand-owner sustainability pledges. Narrow molecular weight distribution also cuts edge-trim waste on blown-film lines and improves bag-making throughput, which increases operating margins for convertors. Premium metallocene grades such as Exceed XP provide year-round toughness suited to cold-chain logistics, while the rapid rise of omnichannel retail elevates parcel-handling stresses that require stronger but lighter films.

Surge in Adoption of Films and Sheets in Packaging Industry

Flexible formats replace rigid containers across food, home-care, and personal-care sectors as retailers prioritize shelf efficiency and lower logistics costs. Metallocene polyethylene delivers stronger hot-tack and wider sealing windows, reducing leakers on high-speed vertical form-fill-seal equipment. Trade bans on PVC in contact applications accelerate transition toward recyclable polyethylene blends, illustrated by PreservaWrap lines that replicate PVC clarity without chloride content. Medical device makers also pivot from PVC to metallocene polyethylene for biocompatibility, which reinforces healthcare demand and widens segment reach.

Volatile Ethylene Feedstock Costs

Swing crude and natural-gas prices cascade into ethylene swings, compressing margins for specialty resin producers who pay a 15-20% catalyst premium. Electrified crackers and carbon-capture retrofits inflate capital cost, adding pressure during feedstock spikes. Vertically integrated Middle Eastern producers retain cost leadership while Asian converters reliant on imports see steeper volatility. Bio-ethylene routes partly hedge volatility yet call for parallel infrastructure build-out, raising upfront cash needs.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Multilayer Agricultural Films and Geomembranes

- Solar-Panel Encapsulant Shift to mPE-Based Tie Layers

- Stringent Single-Use Film Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

mLLDPE commanded 59.01% Metallocene polyethylene market share in 2024. The segment retains leadership thanks to superior puncture resistance and dart impact strength that allow 15-20% down-gauging without packaging failure. Many beverage pouch producers shifted entirely to mLLDPE structures in 2024. In pipe coatings, mLLDPE's flexibility reduces cracking risk during coil-on-reel handling.

mHDPE is forecast to log a 6.65% CAGR through 2030, boosted by pressure pipe and chemical drum demand in developing economies. Stress-crack-resistant grades also penetrate fuel tank blow-molding and under-hood parts. Niche mLDPE lines serve specialty cast-film uses where melt strength is crucial. UHMWPE advances broaden reach into artificial joints and protective gear markets, fortifying value pools for the Metallocene polyethylene market.

Zirconocene catalysts held 62.75% share in 2024. Producers favor their proven operability across gas-phase and solution reactors. Strong track records shorten qualification times, essential for food-contact certifications.

Hafnocene systems, expanding at 5.25% CAGR, excel in high-temperature polymerization that enables faster gas-phase throughput. Recent ligand innovations temper activity drop-off above 90 °C, widening the commercial window. Dual-site and hybrid designs merge narrow and broad molecular fractions in one step, unlocking tailored melt rheology. These innovations further diversify offerings within the Metallocene polyethylene market.

The Metallocene Polyethylene Market Report is Segmented by Type (Metallocene Linear Low-Density Polyethylene (mLLDPE), Metallocene High-Density Polyethylene (mHDPE), and More), Catalyst Type (Single-Site Zirconocene, Hafnocene and Post-Metallocene, and More), Application (Films, Sheets, and More), End-User Industry (Packaging, Agriculture, and More), and Geography (Asia-Pacific, North America, and More).

Geography Analysis

Asia-Pacific led with 46.21% share in 2024, anchored by China's new 1.8 million t ethylene units and India's packaging upturn. These investments ensure feedstock security and shorten delivery time for regional converters. Packaging, construction membranes, and automotive fuel tanks together lifted regional off-take and are expected to keep the Metallocene polyethylene market on a 5.71% CAGR trajectory.

North America relies on shale-linked ethane cost advantages and catalyst innovation leadership. Dow's forthcoming net-zero cracker in Alberta is poised to support premium resin output with low embedded emissions. Mexico secures back-integration gains by importing feedstock from US Gulf complexes and converting into value-added films for domestic consumption and export.

Europe's strict plastic rules challenge demand yet simultaneously open space for recyclable flexible packaging. Germany's auto sector values weight reduction, and Nordic retailers champion mono-material structures that simplify mechanical recycling. TotalEnergies' Amiral complex, though Middle Eastern, channels volumes into Europe, supplementing short domestic supply. South America and the Middle East & Africa remain emerging yet fast-growing clusters. Brazil's greenhouse sector and Qatar's polymer complex expansion add incremental pull on the Metallocene polyethylene market.

- Braskem

- Chevron Phillips Chemical Company LLC.

- Dow

- Exxon Mobil Corporation

- INEOS

- LG Chem

- LyondellBasell Industries Holdings B.V.

- Mitsui Chemicals, Inc.

- Prime Polymer Co., Ltd.

- PTT Global Chemical Public Company Limited

- SABIC

- SIBUR Holding PJSC

- TotalEnergies

- Univation Technologies, LLC.

- W. R. Grace and Co.-Conn

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for high-clarity, down-gauged packaging films

- 4.2.2 Surge in Adoption of Films and Sheets in Packaging Industry

- 4.2.3 Growth of multilayer agricultural films and geomembranes

- 4.2.4 Solar-panel encapsulant shift to mPE-based tie layers

- 4.2.5 Catalyst-switch flexible crackers enabling custom grades

- 4.3 Market Restraints

- 4.3.1 Volatile ethylene feedstock costs

- 4.3.2 Stringent single-use film regulations

- 4.3.3 Post-patent IP disputes on single-site catalysts

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Metallocene Linear Low-density Polyethylene (mLLDPE)

- 5.1.2 Metallocene High-density Polyethylene (mHDPE)

- 5.1.3 Other Types (Metallocene Low-density Polyethylene (mLDPE), etc.)

- 5.2 By Catalyst Type

- 5.2.1 Single-site Zirconocene

- 5.2.2 Hafnocene and post-metallocene

- 5.2.3 Dual-site and hybrid systems

- 5.3 By Application

- 5.3.1 Films

- 5.3.2 Sheets

- 5.3.3 Other Applications (Extrusion Coatings, etc.)

- 5.4 By End-User Industry

- 5.4.1 Packaging

- 5.4.2 Agriculture

- 5.4.3 Automotive

- 5.4.4 Building and Construction

- 5.4.5 Medical and Healthcare

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Thailand

- 5.5.1.6 Indonesia

- 5.5.1.7 Vietnam

- 5.5.1.8 Malaysia

- 5.5.1.9 Philippines

- 5.5.1.10 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Turkey

- 5.5.3.9 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 South Africa

- 5.5.5.5 Nigeria

- 5.5.5.6 Egypt

- 5.5.5.7 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Braskem

- 6.4.2 Chevron Phillips Chemical Company LLC.

- 6.4.3 Dow

- 6.4.4 Exxon Mobil Corporation

- 6.4.5 INEOS

- 6.4.6 LG Chem

- 6.4.7 LyondellBasell Industries Holdings B.V.

- 6.4.8 Mitsui Chemicals, Inc.

- 6.4.9 Prime Polymer Co., Ltd.

- 6.4.10 PTT Global Chemical Public Company Limited

- 6.4.11 SABIC

- 6.4.12 SIBUR Holding PJSC

- 6.4.13 TotalEnergies

- 6.4.14 Univation Technologies, LLC.

- 6.4.15 W. R. Grace and Co.-Conn

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment