PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851648

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851648

Natural Language Processing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

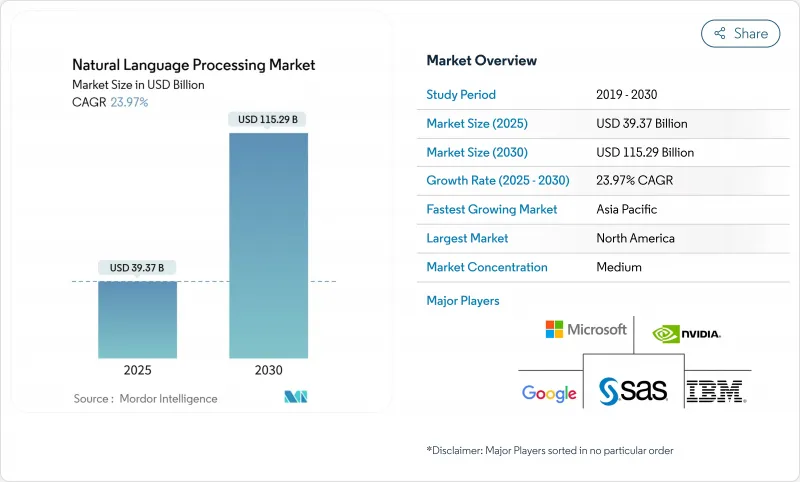

The Natural Language Processing Market size is estimated at USD 39.37 billion in 2025, and is expected to reach USD 115.29 billion by 2030, at a CAGR of 23.97% during the forecast period (2025-2030).

Continued enterprise spending on generative AI accuracy gains and conversational deployments keeps demand strong, with technology majors committing USD 300 billion to AI investments in 2025, reinforcing long-term capital availability. Cloud deployment holds 63.40% of the NLP market, and the segment is expected to post a 24.95% CAGR to 2030 as organizations favor scalable inference infrastructure. Large enterprises account for 57.80% of overall adoption, yet SME uptake is projected to climb 25.01% annually, signaling that accessible cloud APIs are lowering adoption barriers. Software remains the largest component at 46.00% share, while implementation services, expanding at 26.08% CAGR, reflect growing demand for expert model integration. North America contributes 33.30% of global revenues, though Asia Pacific is the fastest-growing region at 25.85% CAGR, thanks to local language model initiatives and supportive public funding.

Global Natural Language Processing Market Trends and Insights

Generative-AI-powered model accuracy gains

Enterprises are moving more workloads into production because newer large language models can now sustain far lower error rates in complex tasks. Anthropic's Claude family illustrates the jump: annualized revenue rose from USD 1 billion in December 2024 to USD 3 billion by May 2025 as code-generation deployments scaled inside corporations. In healthcare, the CHECK framework cut hallucinations in clinical language models from 31% to 0.3%, opening a path for compliance-ready automation in high-risk settings. Financial institutions prefer sector-tuned options such as Baichuan4-Finance, which outperforms general models on certification exams while preserving broad reasoning ability. Because accuracy drives both regulatory acceptance and ROI, firms continue allocating budgets toward fine-tuning and evaluation pipelines that squeeze incremental gains from every new model release.

Surge in conversational AI adoption in customer support

Automated agents are now resolving a majority of frontline queries, unlocking sizable labor savings. Intercom reports 86% full resolution across 45 languages after embedding Claude AI into its support stack. The Asia-Pacific conversational AI market is expanding at a 24.1% CAGR through 2032, helped by rollouts at Alibaba and HDFC Bank that serve multilingual customer bases. Teneo.ai documents USD 5.60 cost reduction for every call it automates while maintaining 95% natural-language understanding accuracy. As translation quality improves, enterprises deploy a single bot across regions rather than running siloed language teams, strengthening the business case for faster uptake.

Shortage of High-Quality, Bias-Free Training Data

Limited domain-specific datasets impede performance for specialized uses. Vietnam responded by releasing ViGPT to address local linguistic gaps. The EU AI Act further mandates bias monitoring for high-risk systems, raising compliance workloads. Healthcare and finance feel the squeeze hardest, as privacy regulations restrict usable data pools, giving firms with proprietary datasets a head start.

Other drivers and restraints analyzed in the detailed report include:

- Integration of NLP in embedded/edge devices

- Proliferation of domain-specific LLMs for regulated industries

- Escalating Inference Costs for Large Models

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud accounts for 63.40% of the NLP market share in 2024, and the segment is projected to log a 24.95% CAGR to 2030. Usage-based pricing and elastic compute underpin its lead as enterprises experiment with generative workloads without investing in on-prem hardware. Microsoft Azure AI services grew 157% year-over-year to surpass USD 13 billion annualized revenue. Hybrid models serve regulated industries where data residency rules persist, splitting inference between local clusters and public clouds. Edge deployments now supplement cloud for latency-sensitive tasks, leveraging smartphones whose aggregate compute rises 25% yearly. This mix suggests the NLP market will organize around workload-specific deployment rather than a single dominant mode.

Large enterprises held 57.80% of the NLP market share in 2024, sustained by data assets and in-house AI staff. Yet SMEs are expected to outpace with a 25.01% CAGR through 2030 as turnkey APIs make advanced models accessible. Studies note SMEs pivot first on customer support and document processing before scaling to advanced analytics. API-based pay-as-you-go removes upfront capital, allowing SMEs to prove ROI quickly. Conversely, large firms pour resources into custom fine-tuning, spinning internal LLM centers of excellence to navigate compliance and security. This divergence will keep the NLP industry balanced between volume growth from SMEs and high-value bespoke projects at larger corporations.

The Natural Language Processing Market Report is Segmented by Deployment (On-Premise and Cloud), Organization Size (Large Organizations and Small and Medium Enterprises [SMEs]), Component (Hardware, Software, and Services), Processing Type (Text, Speech/Voice, and Image/Vision), End-User Industry (BFSI, Healthcare and Life Sciences, IT and Telecom, Retail and E-Commerce, Manufacturing, and More), and Geography.

Geography Analysis

North America commanded 33.30% revenue in 2024 and remains the largest regional contributor. Microsoft Cloud revenue reached USD 42.4 billion in FY 2025 Q3, up 20% year-over-year, with AI services a key driver. Venture funding and an enabling regulatory setting combine to accelerate enterprise rollouts.

Asia Pacific is projected to post a 25.85% CAGR, propelled by sovereign AI programs and local-language model development. Japan's commitment to support Southeast Asian LLM capacity showcases efforts to cut reliance on foreign providers. Regional conversational AI revenue tracks at 24.1% CAGR to 2032, indicating sustained demand for multilingual customer engagement tools.

Europe advances under the EU AI Act, balancing innovation with stringent compliance. Germany's AI market climbed 25% year-on-year to EUR 10 billion in Q1 2025, with companies like Siemens achieving 90% automation in document workflows. The regulation's detailed risk tiers favor vendors able to document processes, and this supports steady though measured growth. South America and MEA remain nascent, yet rising public-cloud footprints and smart-device adoption foreshadow untapped potential for the NLP market.

- Microsoft Corp.

- Google LLC (Alphabet)

- Amazon Web Services

- IBM Corp.

- NVIDIA Corp.

- OpenAI LP

- Meta Platforms Inc.

- SAP SE

- Oracle Corp.

- Baidu Inc.

- Intel Corp.

- Qualcomm Inc.

- SAS Institute Inc.

- Adobe Inc.

- Salesforce Inc.

- Apple Inc.

- Verint Systems Inc.

- Nuance Communications (Microsoft)

- Cohere Inc.

- Hugging Face

- Grammarly Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Generative-AI-powered model accuracy gains

- 4.2.2 Surge in conversational AI adoption in customer support

- 4.2.3 Integration of NLP in embedded/edge devices

- 4.2.4 Proliferation of domain-specific LLMs for regulated industries

- 4.2.5 Rising demand for real-time speech recognition in automotive and smart devices

- 4.2.6 Multimodal foundation models unlocking new verticals

- 4.3 Market Restraints

- 4.3.1 Shortage of high-quality, bias-free training data

- 4.3.2 Escalating inference costs for large models

- 4.3.3 Cross-border data residency compliance barriers

- 4.3.4 Environmental footprint of large-scale training compute

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of COVID-19 and Macro Slowdown

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 On-premise

- 5.1.2 Cloud

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises (SMEs)

- 5.3 By Component

- 5.3.1 Hardware

- 5.3.2 Software

- 5.3.3 Services

- 5.4 By Processing Type

- 5.4.1 Text

- 5.4.2 Speech/Voice

- 5.4.3 Image/Vision

- 5.5 By End-user Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 IT and Telecom

- 5.5.4 Retail and E-commerce

- 5.5.5 Manufacturing

- 5.5.6 Media and Entertainment

- 5.5.7 Education

- 5.5.8 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corp.

- 6.4.2 Google LLC (Alphabet)

- 6.4.3 Amazon Web Services

- 6.4.4 IBM Corp.

- 6.4.5 NVIDIA Corp.

- 6.4.6 OpenAI LP

- 6.4.7 Meta Platforms Inc.

- 6.4.8 SAP SE

- 6.4.9 Oracle Corp.

- 6.4.10 Baidu Inc.

- 6.4.11 Intel Corp.

- 6.4.12 Qualcomm Inc.

- 6.4.13 SAS Institute Inc.

- 6.4.14 Adobe Inc.

- 6.4.15 Salesforce Inc.

- 6.4.16 Apple Inc.

- 6.4.17 Verint Systems Inc.

- 6.4.18 Nuance Communications (Microsoft)

- 6.4.19 Cohere Inc.

- 6.4.20 Hugging Face

- 6.4.21 Grammarly Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment