PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851661

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851661

In-Memory Database - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

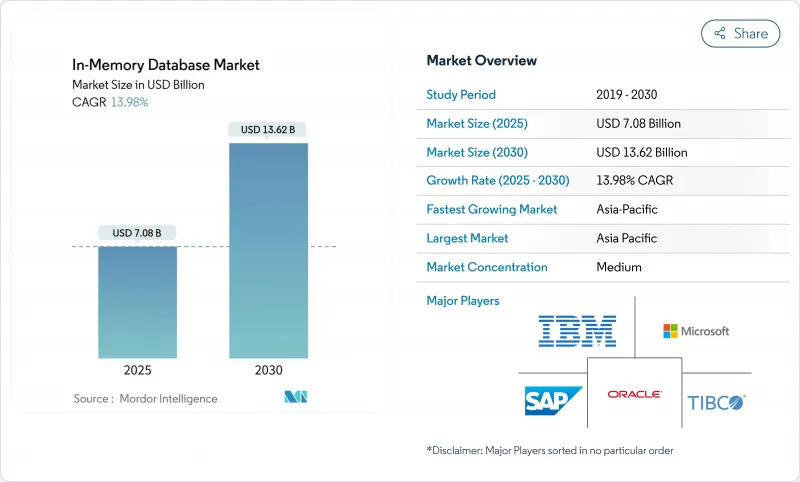

The global In-Memory Database market size stood at USD 7.08 billion in 2025 and is expected to reach USD 13.62 billion by 2030, advancing at a 13.98% CAGR over the forecast period.

Sub-millisecond performance requirements from cloud-native microservices, AI inference engines, and streaming analytics platforms continued to push enterprises toward memory-centric architectures. Lower DRAM prices and the arrival of CXL-based persistent memory modules have reduced the total cost of ownership, encouraging more workloads to migrate from disk-backed systems. Edge deployments in connected vehicles and Industrial IoT plants further expanded demand because local processing avoids network latency penalties. Competitive dynamics remained fluid as traditional vendors deepened integrations with hyperscale clouds while open-source forks gained momentum, giving buyers new paths to avoid vendor lock-in.

Global In-Memory Database Market Trends and Insights

Cloud-Native Microservices Demanding Sub-Millisecond Latency

Cloud-native adoption reshaped performance baselines as containerized microservices needed data access in microseconds. Session stores, personalization engines, and high-frequency trading platforms shifted from disk-backed databases to memory-centric stores because every millisecond of delay reduced conversion rates or trading profit. Dragonfly demonstrated 6.43 million operations per second on AWS Graviton3E silicon, highlighting the ceiling now expected from database tiers. Financial institutions and digital commerce operators that migrated monoliths to distributed systems saw response-time improvements translate into tangible revenue gains, reinforcing the driver's near-term importance.

Falling DRAM and Persistent Memory Costs Widening TCO Gap

Global spot pricing of DDR4 and DDR5 modules continued to slide, while Samsung's CXL Memory Module Hybrid prototype showed DRAM-class latency with persistence, creating a compelling cost profile. Hyperscale operators pooled memory across racks, reducing stranded capacity and backup cycles. Enterprises pivoted roadmaps toward in-memory deployment because the premium over SSD arrays narrowed, especially for analytics workloads with tight SLA windows. The effect is visible in Asia-Pacific manufacturing hubs where large historian datasets are moved into memory for real-time digital-twin analytics.

Vendor Lock-in Concerns Around Proprietary Formats

Redis's license change in 2024 heightened buyer wariness of proprietary formats, spurring AWS, Google, and Oracle to back the Valkey fork under the Linux Foundation. Enterprises budgeting multi-year database projects factored in exit costs, slowing purchase cycles. To mitigate risk, some adopted multi-database orchestration layers, but those abstractions introduced latency penalties that partially offset memory-speed gains.

Other drivers and restraints analyzed in the detailed report include:

- Streaming Analytics Adoption in BFSI and Telecom

- HTAP Architectures Accelerating AI/ML Model Serving

- High-Availability Design Complexity for Large Clusters

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The OLTP segment held 45.3% of the In-Memory Database market share in 2024, underscoring continued reliance on high-integrity transactional workloads across banking, e-commerce, and ERP systems. Demand persisted because mission-critical records still required ACID compliance, with enterprises paying a performance premium for sub-millisecond commits. OLAP deployments addressed established business-intelligence front ends but grew slowly as analytics shifted toward more flexible engines.

HTAP climbed with a 21.1% CAGR forecast from 2025 to 2030 as firms sought single-platform simplicity. GridGain's platform showed up to 1,000X speed-ups over disk-based systems while retaining ANSI SQL-99 support. Real-time risk calculations and supply-chain twins needed simultaneous read-write access, making HTAP the preferred architecture. The convergence unlocked incremental budget from departments earlier siloed between operations and analytics, pushing the In-Memory Database market toward unified designs.

On-premise installations captured 55.4% of 2024 revenue because regulated sectors required full control over data residency and tailored HA architectures. Legacy enterprise software stacks tightly integrated with on-premise databases, anchoring spending even as public clouds mature. Cloud deployments, nonetheless, have advanced as digital-native firms adopted managed services to avoid infrastructure administration.

Edge and embedded deployments displayed a 23.2% CAGR outlook, fueled by connected cars and IIoT gateways. Modern vehicles generate around 300 TB annually, which demands in-vehicle processing for autonomous features. TDengine achieved 10X compression over Elasticsearch in smart-vehicle telemetry, cutting bandwidth for upstream transfers. Manufacturers applied similar strategies on production lines to detect defects instantly. The shift signaled that performance gains once reserved for data centers were now indispensable at the edge, expanding the In-Memory Database market footprint.

In-Memory Database Market is Segmented by Processing Type (OLTP, OLAP, and HTAP), Deployment Mode (On-Premise, and More), Data Model (SQL, Nosql, and Multi-Model), Organization Size (SMEs, and Large Enterprises), Application (Real-Time Transaction Processing, and More), End-User Industry (BFSI, Telecommunications and IT, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Geography Analysis

Asia-Pacific recorded the largest regional revenue at 32.2% in 2024 and maintained a 17.1% CAGR outlook. National Industry 4.0 programs in China, Japan, and India spurred factory automation that required in-memory historian databases for sub-second MES feedback loops. General Motors linked more than 100,000 operational technology connections in its MES 4.0 rollout, illustrating the scale of edge deployments. Local vendors such as Nautilus Technologies' advanced indigenous relational engines, reducing reliance on foreign IP.

North America formed a mature but innovation-rich market centered on financial services, hyperscale clouds, and autonomous-vehicle R&D. Oracle and Google deepened their partnership to run Oracle Database services natively on Google Cloud, marrying enterprise SQL capabilities with AI accelerators. The region's venture funding supported emerging players such as Dragonfly, intensifying competitive churn.

Europe prioritized data-sovereignty compliance under GDPR, driving hybrid cloud adoption and favoring on-premise clusters combined with managed services in local data centers. Oracle expanded Database@Azure coverage to additional EU regions to satisfy residency rules. The continent also saw healthcare deployments of HTAP databases to power AI diagnostics under strict privacy frameworks.

The Middle East and Africa invested in smart-city fiber and 5G backbones, leading to pilot IIoT deployments that require real-time analytics. South America gained traction in mining operations and digital banking, where low-latency fraud detection justified premium memory-centric systems. Though absolute spend in these two regions remained modest, double-digit growth expanded the In-Memory Database market's global diversity.

- SAP SE

- Oracle Corp.

- Microsoft Corp.

- IBM Corp.

- Redis Ltd. (Redis Enterprise)

- Aerospike Inc.

- VoltDB Inc.

- Couchbase Inc.

- DataStax Inc.

- Hazelcast Inc.

- MemVerge Inc.

- Altibase Corp.

- GridGain Systems Inc.

- Raima Inc.

- McObject LLC

- Pivotal (VMware Tanzu GemFire)

- Amazon Web Services (Amazon ElastiCache & MemoryDB)

- Google Cloud (AlloyDB, Memorystore)

- Alibaba Cloud (ApsaraDB Tair)

- Huawei Cloud (GaussDB IM)

- Tencent Cloud (Tendis)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-native micro-services demanding sub-millisecond latency

- 4.2.2 Falling DRAM and persistent-memory USD/GB widening TCO gap vs. disk

- 4.2.3 Streaming analytics adoption in BFSI and telecom for fraud and network QoS

- 4.2.4 HTAP architectures accelerating AI/ML model-serving in healthcare

- 4.2.5 Edge-compute use-cases (connected vehicles, IIoT) requiring embedded IMDB

- 4.3 Market Restraints

- 4.3.1 Vendor lock-in concerns around proprietary in-memory formats

- 4.3.2 High-availability design complexity for >40 TB clusters

- 4.3.3 Data-sovereignty laws (e.g., China CSL, EU GDPR) limiting global replication

- 4.4 Value Chain Analysis

- 4.5 Regulatory or Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of macroeconomoic factors on the market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Processing Type

- 5.1.1 OLTP

- 5.1.2 OLAP

- 5.1.3 Hybrid Transactional/Analytical Processing (HTAP)

- 5.2 By Deployment Mode

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.2.3 Edge/Embedded

- 5.3 By Data Model

- 5.3.1 Relational (SQL)

- 5.3.2 NoSQL (Key-Value, Document, Graph)

- 5.3.3 Multi-model

- 5.4 By Organization Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

- 5.5 By Application

- 5.5.1 Real-time Transaction Processing

- 5.5.2 Operational Analytics and BI Dashboards

- 5.5.3 AI/ML Model Serving

- 5.5.4 Caching and Session Stores

- 5.6 By End-user Industry

- 5.6.1 BFSI

- 5.6.2 Telecommunications and IT

- 5.6.3 Retail and E-commerce

- 5.6.4 Healthcare and Life Sciences

- 5.6.5 Manufacturing and Industrial IoT

- 5.6.6 Media and Entertainment

- 5.6.7 Government and Defense

- 5.6.8 Others (Energy, Education, etc.)

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 France

- 5.7.2.3 United Kingdom

- 5.7.2.4 Nordics

- 5.7.2.5 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Taiwan

- 5.7.3.3 South Korea

- 5.7.3.4 Japan

- 5.7.3.5 India

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Mexico

- 5.7.4.3 Argentina

- 5.7.4.4 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 Saudi Arabia

- 5.7.5.1.2 United Arab Emirates

- 5.7.5.1.3 Turkey

- 5.7.5.1.4 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corp.

- 6.4.3 Microsoft Corp.

- 6.4.4 IBM Corp.

- 6.4.5 Redis Ltd. (Redis Enterprise)

- 6.4.6 Aerospike Inc.

- 6.4.7 VoltDB Inc.

- 6.4.8 Couchbase Inc.

- 6.4.9 DataStax Inc.

- 6.4.10 Hazelcast Inc.

- 6.4.11 MemVerge Inc.

- 6.4.12 Altibase Corp.

- 6.4.13 GridGain Systems Inc.

- 6.4.14 Raima Inc.

- 6.4.15 McObject LLC

- 6.4.16 Pivotal (VMware Tanzu GemFire)

- 6.4.17 Amazon Web Services (Amazon ElastiCache & MemoryDB)

- 6.4.18 Google Cloud (AlloyDB, Memorystore)

- 6.4.19 Alibaba Cloud (ApsaraDB Tair)

- 6.4.20 Huawei Cloud (GaussDB IM)

- 6.4.21 Tencent Cloud (Tendis)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment