PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910495

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910495

Gypsum Board - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

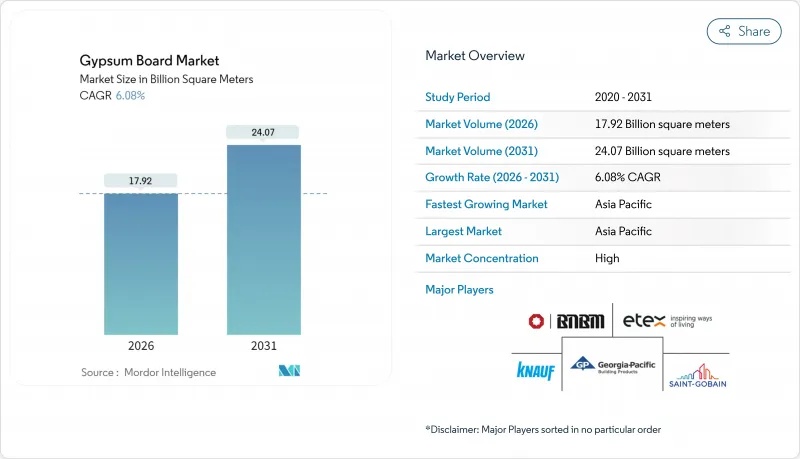

Gypsum Board Market size in 2026 is estimated at 17.92 Billion square meters, growing from 2025 value of 16.89 Billion square meters with 2031 projections showing 24.07 Billion square meters, growing at 6.08% CAGR over 2026-2031.

Ongoing fire-safety and energy-efficiency mandates anchor demand, while Asia-Pacific's construction boom, chronic housing shortages in North America, and tightening embodied-carbon rules in Europe shape the competitive field. Capacity expansion projects in Texas and Montreal illustrate how producers balance cost discipline with sustainability investments. Meanwhile, the shift toward lightweight and pre-decorated solutions helps contractors mitigate labor shortages, and recycled or synthetic feedstocks gain strategic importance as coal-powered electricity retires faster than expected. Fiber-cement's encroachment in wet areas keeps pricing rational, yet broad infrastructure renewal programs continue to backstop volume growth across the gypsum board market.

Global Gypsum Board Market Trends and Insights

Surging Residential Construction in APAC

Rapid urban migration pushes developers toward high-density housing, and gypsum board systems help shorten interior fit-out cycles compared with wet plaster. Although China's overall cement output fell 10% in 2024, wallboard volumes remained resilient because developers focused on accelerating finishing work to unlock cash flows. India's government-backed housing schemes add steady baseline demand, while Southeast Asian megaprojects specify gypsum for its proven fire resistance in schools and transit hubs. Labor shortages across the region strengthen the appeal of factory-finished boards that reduce on-site trades.

Accelerating Renovation and Remodeling Wave in Mature Markets

Renovation outlays in the United States climbed to USD 509 billion in 2025, reversing two years of contraction. Forty percent of U.S. dwellings pre-date 1970, so wall replacements align with tighter fire and insulation codes, directly lifting gypsum demand. Homeowners spent an average USD 4,700 on interior upgrades, with mold- and moisture-resistant boards ranking high on shopping lists. Similar retrofit mandates in the EU catalyze orders for high-performance panels that combine thermal and acoustic gains. These dynamics sustain a stable volume base for the gypsum board market during economic slowdowns.

Volatile Natural Gypsum and Energy Prices

Mined gypsum output touched 22 million tons in the United States during 2024, but unit costs varied widely by mine depth and haulage distance. Calcination relies heavily on natural gas, making board pricing sensitive to fuel swings. As decommissioning of coal plants removes synthetic supply, mills draw from deposits located farther afield, inflating freight bills and amplifying cost risk. Energy-efficient kilns and regional warehouse hubs partly soften the blow, yet input volatility still trims the gypsum board market growth trajectory in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Lightweight and High-Strength Drywall Solutions

- Government Incentives for Fire, Sound, and Energy-Efficient Buildings

- Rising Penetration of Fibre-Cement and Other Panel Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wall board retained 59.62% gypsum board market share in 2025, sustained by universal acceptance in residential interiors where cost and code compliance drive specification. Pre-decorated panels, however, are forecast to post 7.39% CAGR to 2031, a speed more than one percentage point above the overall gypsum board market.

Premium segments now favor mold-, moisture- or impact-modified boards such as PURPLE XP, priced at a 20-30% uplift over generic Type X, yet often selected for kitchens, baths, and healthcare corridors where downtime is costly. Manufacturers bundle these attributes with factory coatings to seize higher-margin value capture. As contractors increasingly pursue "paint-ready" delivery, pre-decorated formats are poised to widen their share within the gypsum board market.

The Gypsum Board Report is Segmented by Product Type (Wall Board, Ceiling Board, and Pre-Decorated Board), Raw Material (Natural Gypsum, Synthetic (FGD) Gypsum, and Recycled Gypsum), Application (Residential, Commercial, Institutional, and Industrial), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Units).

Geography Analysis

Asia-Pacific claimed 46.10% of 2025 shipments, thanks to China's massive real-estate backlog and India's Housing for All program. Regional growth at 7.31% CAGR through 2031 ensures the gypsum board market remains volume-weighted to this geography despite political and credit risk clouds.

North America embodies renovation-driven steadiness. Europe's pathway is more regulation-led, as RE2020 and similar frameworks reinforce demand for carbon-optimized designs despite slower macro indicators. Together, the three regions shape the competitive map, while South America, and Middle-East and Africa remain opportunity frontiers where lower per-capita penetration leaves headroom for future gypsum board market growth.

Manufacturers differentiate through environmental product declarations, often bundling recycled content to meet tender prerequisites. Although construction output is flatter than Asia-Pacific, premium ESG-minded pricing offsets slower unit growth, safeguarding revenue expansion inside the gypsum board market.

- BNBM

- Etex Group

- Everest Industries Limited

- Georgia-Pacific Gypsum LLC

- Global Gypsum Board Co LLC (Gypcore)

- Holcim

- Jason New Materials

- Knauf Group

- National Gypsum Services Company

- Osman Group

- PABCO Gypsum

- Saint-Gobain

- Shandong Taihe Dongxin Co.,Ltd

- VANS Gypsum

- Volma

- Winstone Wallboards Limited

- YOSHINO GYPSUM CO.,LTD.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Residential Construction in APAC

- 4.2.2 Accelerating Renovation and Remodeling Wave in Mature Markets

- 4.2.3 Shift Toward Lightweight and High-Strength Drywall Solutions

- 4.2.4 Government Incentives for Fire, Sound, and Energy-Efficient Buildings

- 4.2.5 Cost-Advantaged Synthetic (FGD) Gypsum Availability

- 4.3 Market Restraints

- 4.3.1 Volatile Natural Gypsum and Energy Prices

- 4.3.2 Rising Penetration of Fibre-Cement and Other Panel Alternatives

- 4.3.3 Carbon-Neutral Mandates Raising Embodied-Carbon Scrutiny

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Wall Board

- 5.1.2 Ceiling Board

- 5.1.3 Pre-decorated Board

- 5.2 By Raw Material

- 5.2.1 Natural Gypsum

- 5.2.2 Synthetic (FGD) Gypsum

- 5.2.3 Recycled Gypsum

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Institutional

- 5.3.4 Industrial

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Thailand

- 5.4.1.6 Malaysia

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Turkey

- 5.4.3.8 Nordics

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Nigeria

- 5.4.5.4 Egypt

- 5.4.5.5 Qatar

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 BNBM

- 6.4.2 Etex Group

- 6.4.3 Everest Industries Limited

- 6.4.4 Georgia-Pacific Gypsum LLC

- 6.4.5 Global Gypsum Board Co LLC (Gypcore)

- 6.4.6 Holcim

- 6.4.7 Jason New Materials

- 6.4.8 Knauf Group

- 6.4.9 National Gypsum Services Company

- 6.4.10 Osman Group

- 6.4.11 PABCO Gypsum

- 6.4.12 Saint-Gobain

- 6.4.13 Shandong Taihe Dongxin Co.,Ltd

- 6.4.14 VANS Gypsum

- 6.4.15 Volma

- 6.4.16 Winstone Wallboards Limited

- 6.4.17 YOSHINO GYPSUM CO.,LTD.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment