PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851736

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851736

Payment Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

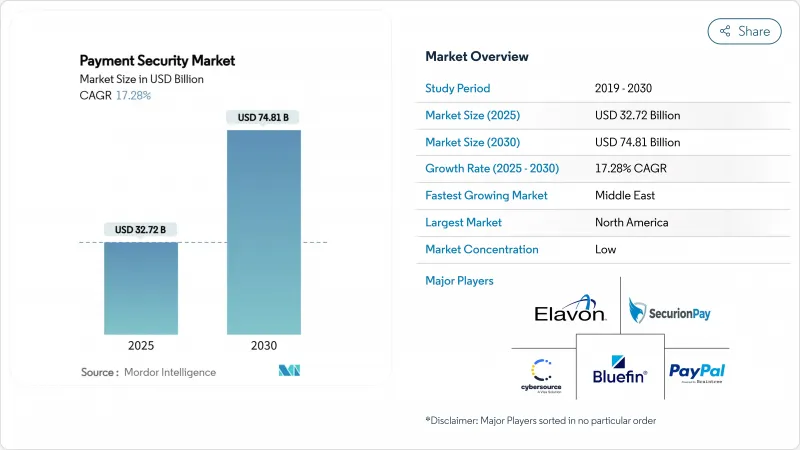

The global payment security market size holds a current value of USD 33.72 billion in 2025 and is forecast to advance to USD 74.81 billion by 2030, translating into a 17.28% CAGR.

This solid trajectory aligns with tightening regulatory mandates, rising transaction volumes across digital channels, and continued innovation in detection technologies. Continuous compliance investments linked with the final PCI DSS 4.0 deadline, wide-scale application of artificial intelligence in fraud analytics, and the proliferation of mobile-first wallets are shaping enterprise spending priorities. Tokenization and encryption remain foundational, yet real-time behavioral analytics and multi-factor authentication are taking a larger budget share as issuers and merchants confront synthetic identity attacks. Parallel to technology upgrades, competitive consolidation among networks and processors is accelerating as firms integrate threat-intelligence platforms and expand global merchant bases to defend share in the payment security market

Global Payment Security Market Trends and Insights

Regulatory push for PCI DSS 4.0 compliance

Mandatory adherence to PCI DSS 4.0 beginning in March 2025 is reshaping security budgets across North America. Enterprises face annual outlays that climb to USD 250,000 at Level 1, reflecting the standard's 64 new requirements covering continuous log analysis and payment-page script integrity. Non-compliance fines of up to USD 500,000 per month sharpen the focus on immediate remediation, prompting rapid adoption of tokenization and automated encryption services. European acquirers are already mapping PSD3 provisions to PCI controls, creating a spill-over effect that sustains investment momentum through 2027.

Surge in AI-based fraud analytics

Financial institutions increasingly pivot from rule-based engines to adaptive machine-learning models that inspect more than 100 contextual signals in real time. Visa reports that AI applications blocked USD 40 billion in fraudulent transactions during 2024, cutting false positives by 85% and improving authorization rates. Cloud processors embed these models as micro-services, allowing merchants to fine-tune risk thresholds without lengthy integrations. Emerging markets benefit from cloud scale because it removes the need for legacy on-premise infrastructure, a dynamic that supports uniform global deployment of next-generation fraud analytics.

High upfront integration costs for SMEs

Typical annual security spend for a small merchant can range from USD 5,000 to USD 50,000, an amount that strains cash flows in emerging economies where total IT budgets are modest. Complex scoping exercises push many SMEs toward bundled cloud subscriptions, yet concerns around data residency and vendor lock-in slow conversions. As a result, low-cost plug-in solutions dominate lower-volume web stores, leaving gaps in advanced risk analytics. Security vendors that can tier services according to volume thresholds are expected to capture latent SME demand once cost curves decline.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of BNPL requiring secure token vaults

- Rapid growth of IoT-enabled POS terminals

- Transaction-latency issues in 3-D Secure 2.2 roll-outs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tokenization accounted for 31% of payment security market share in 2024, underscoring its role in removing primary account numbers from merchant systems and shrinking audit scope. Visa processed 10 billion tokenized transactions in 2024, up 45% from the prior year, proving scalability in both in-store and e-commerce settings. Encryption remains mandatory for data-in-transit, particularly in banking and healthcare where breach disclosure rules impose heavy penalties. Fraud detection platforms that embed machine-learning pipelines are projected to expand at 21.03% CAGR, reflecting demand for adaptive controls that self-learn from evolving attack vectors. Other emerging solutions, including quantum-safe cryptography and distributed-ledger verification, currently capture niche use-cases but hold long-term upside as standards mature. Vendors able to interlink token services with AI-driven analytics create combined offerings that minimize manual review costs while keeping false positives in check. This capability supports upsell cycles, positioning integrated platforms for outsized contribution to overall payment security market revenue.

Growth across solution types will influence payment security market size forecasts, specifically by shifting spend from basic compliance tools to intelligent orchestration engines. Vendors competing on breadth rather than point functionality tend to secure longer-term contracts, especially with enterprises that favor consolidated dashboards for audit reporting. As token vault density increases inside acquirer environments, supply-chain chip shortages may hit hardware HSM refresh plans, thereby accelerating interest in virtualized key-management modules.

Web-based deployments led the payment security market in 2024 with a 47% share, driven by entrenched desktop shopping patterns and mature gateway integrations. However, mobile platforms are the clear growth engine at 23.15% CAGR through 2030. China already records that 82% of online baskets close via mobile wallets, while India's UPI system enables sub-second peer-to-merchant transfers that now outpace card usage. These trends elevate requirements for biometric authentication, network-token provisioning, and device attestation directly in the app layer. As a result, security roadmaps center on building SDKs that allow merchants to orchestrate common policies across native mobile, browser, and progressive web-app flows.

Omnichannel strategies are narrowing the historical gap between card-present and card-not-present security standards. In-store tap-to-phone initiatives, enabled by NFC and MPoC guidelines, introduce the same real-time risk insights present in e-commerce. The rise of mobile also acts as a forcing function for web platforms to adopt modern session integrity controls, ensuring that customer experience remains consistent across a retailer's full engagement cycle.

Payment Security Market is Segmented by Solution Type (Encryption, Tokenization and More), Platform (Mobile-Based, Web-Based, In-Store / POS), Organization Size (Small & Medium-Sized Enterprises (SMEs), Large Enterprises), End-User Industry (Retail & E-Commerce, BFSI and More), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 30% of payment security market revenue in 2024, boosted by early PCI DSS 4.0 migrations and continued upgrades among large omnichannel merchants. Enterprise budgets prioritise AI-powered risk engines, while card networks bundle value-added security services inside processing tariffs. Implementation challenges linked to 3DS 2.2 latency still influence approval ratios, yet the regulatory certainty of defined enforcement timelines underpins steady procurement pipelines. Strategic acquisitions, such as Mastercard's USD 2.65 billion purchase of Recorded Future in 2024, highlight an ongoing drive to embed native threat-intelligence feeds inside network stacks.

Asia-Pacific remains the growth nucleus. Mobile wallets now drive 70% of total ecommerce volume, supported by government-backed real-time payment rails and aggressive financial inclusion policies. Infrastructure leapfrogging lets merchants skip legacy mag-stripe systems, installing cloud-native gateways from inception. Cross-border QR alliances, typified by the linkage between Singapore's PayNow and Thailand's PromptPay, further increase transaction counts that must be secured end-to-end. As a result, regional demand skews toward lightweight SDKs that embed device binding and behavioral biometrics without adding checkout friction.

Europe balances strong consumer-protection norms with rapid POS technology refresh cycles. PCI MPoC and PSD3 create a harmonised compliance backdrop across 27 member states, spurring automotive, hospitality, and transport sectors to adopt contactless and IoT-enabled terminals. Meanwhile, the Middle East and Africa show the highest CAGR at 20.52% through 2030, driven by mobile-money platforms that serve previously unbanked populations. Regional regulators accelerate digital-identity frameworks, supporting cloud token vaults hosted in locally compliant data centres. These initiatives collectively expand regional payment security market size, although SME affordability constraints persist.

- Visa Inc. (CyberSource Corporation)

- Bluefin Payment Systems LLC

- PayPal Holdings Inc. (Braintree)

- Elavon Inc.

- SecurionPay

- Global Payments Inc.

- Worldline SA

- Broadcom Inc. (Symantec)

- Stripe Inc.

- Fiserv Inc. (First Data)

- Signifyd Inc.

- Adyen N.V.

- Shift4 Payments Inc.

- TokenEx Inc.

- Forter Ltd.

- ACI Worldwide Inc.

- RSA Security LLC

- F5 Inc. (Shape Security)

- Thales Group (Gemalto)

- Transaction Network Services (TNS)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Push for PCI-DSS 4.0 Compliance in North America

- 4.2.2 Surge in AI-based Fraud Analytics among Cloud Payment Processors

- 4.2.3 Expansion of Buy-Now-Pay-Later (BNPL) Requiring Secure Token Vaults

- 4.2.4 Rapid Growth of IoT-Enabled POS Terminals in Europe

- 4.2.5 Mobile-First Wallet Boom across Emerging Asian Markets

- 4.3 Market Restraints

- 4.3.1 High Up-front Integration Costs for Small & Mid-Sized Merchants

- 4.3.2 Transaction-Latency Issues in 3-D Secure 2.2 Roll-outs

- 4.3.3 Fragmented & Overlapping Data-Protection Statutes in Emerging Nations

- 4.3.4 Consumer Privacy Concerns over Behavioral Biometrics

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Assessment of Macro Economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Solution Type

- 5.1.1 Encryption

- 5.1.2 Tokenization

- 5.1.3 Fraud Detection & Prevention

- 5.1.4 Other Solutions

- 5.2 By Platform

- 5.2.1 Mobile-Based

- 5.2.2 Web-Based

- 5.2.3 In-Store / POS

- 5.3 By Organization Size

- 5.3.1 Small & Medium-Sized Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By End-user Industry

- 5.4.1 Retail and E-commerce

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 IT and Telecom

- 5.4.5 Travel and Hospitality

- 5.4.6 Government

- 5.4.7 Other Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Visa Inc. (CyberSource Corporation)

- 6.4.2 Bluefin Payment Systems LLC

- 6.4.3 PayPal Holdings Inc. (Braintree)

- 6.4.4 Elavon Inc.

- 6.4.5 SecurionPay

- 6.4.6 Global Payments Inc.

- 6.4.7 Worldline SA

- 6.4.8 Broadcom Inc. (Symantec)

- 6.4.9 Stripe Inc.

- 6.4.10 Fiserv Inc. (First Data)

- 6.4.11 Signifyd Inc.

- 6.4.12 Adyen N.V.

- 6.4.13 Shift4 Payments Inc.

- 6.4.14 TokenEx Inc.

- 6.4.15 Forter Ltd.

- 6.4.16 ACI Worldwide Inc.

- 6.4.17 RSA Security LLC

- 6.4.18 F5 Inc. (Shape Security)

- 6.4.19 Thales Group (Gemalto)

- 6.4.20 Transaction Network Services (TNS)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment