PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910540

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910540

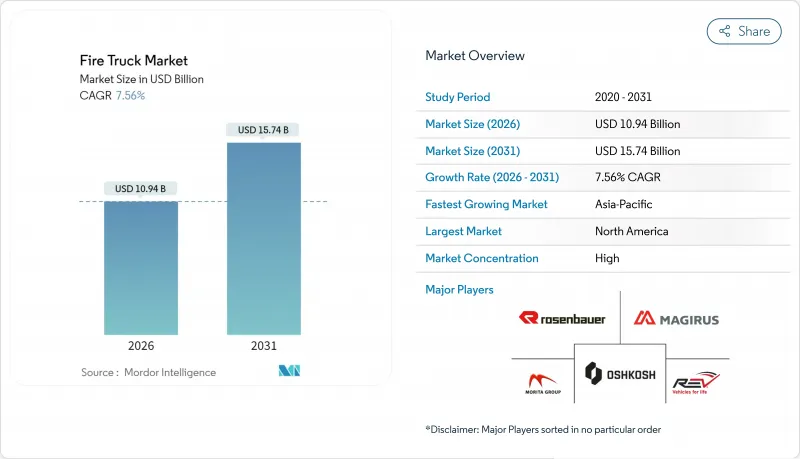

Fire Truck - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Fire Truck Market is expected to grow from USD 10.17 billion in 2025 to USD 10.94 billion in 2026 and is forecast to reach USD 15.74 billion by 2031 at 7.56% CAGR over 2026-2031.

Fleet replacement cycles, electrification momentum, and climate-driven wildfire risk are combining to lift procurement budgets despite lingering supply-chain bottlenecks. Extended order lead times of 18-33 months are prompting departments to modernize maintenance programs while they wait for new deliveries. Yet, the fire truck market continues to absorb higher unit prices as safety and performance features become non-negotiable. Battery-electric models are moving from pilot to production status in North America and Europe, supported by clean-fleet mandates and measurable savings in fuel and maintenance outlays. Meanwhile, an increase in large-scale wildfire incidents stimulates demand for specialized wildland configurations, and consolidated OEM power is drawing heightened regulatory scrutiny in the United States.

Global Fire Truck Market Trends and Insights

Stringent global & regional fire-safety regulations

The new NFPA 1900 standard unifies previous apparatus rules and introduces mandatory rear-view cameras, LED lighting and electric-vehicle guidance. By shifting from prescriptive checklists toward performance-based criteria, regulators give OEMs room to innovate while still elevating baseline safety. Harmonized requirements also support cross-border apparatus deployment, a benefit for manufacturers with global logistics footprints. Compliance costs, however, are accelerating consolidation among smaller builders, reinforcing the high-concentration profile of the fire truck market.

Rising frequency & severity of wildfires

U.S. wildfire acreage hit 7.7 million acres in 2024, outpacing the 10-year average despite fewer total incidents. Larger, more intense events drive orders for Type 1 Wildland-Urban Interface engines with auxiliary pumps that operate while the vehicle is moving. Federal and state grants aimed at wildfire readiness funnel capital into specialized equipment, keeping demand insulated from municipal budget cycles. The extended season now covers nearly the full calendar year, requiring departments to maintain year-round readiness and boosting the baseline for apparatus utilization.

High upfront cost of next-gen platforms

An electric pumper such as the RTX lists close to a million dollar, roughly double a comparable diesel engine. While operational savings improve total cost of ownership, the initial capital hurdle delays adoption for volunteer and rural departments. Grant programs partially offset costs-Boulder secured a decent amount in external funding for its second electric unit-but financing gaps persist outside well-funded metros. Battery costs are falling yet are unlikely to reach parity with diesel until production runs scale meaningfully after 2027. This two-tier dynamic slows the transition in developing regions, restraining global fire truck market growth in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Growing adoption of electric fire trucks

- Rapid replacement of ageing municipal fleets in Europe

- Semiconductor & chassis supply-chain disruptions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The pumper segment held 36.28% of the fire truck market in 2025 and is set to advance at a 7.62% CAGR to 2031. Pumper evolution adds compressed-air foam systems and modular bodywork, giving departments multi-purpose capability. Segment revenue also benefits from early electrification, with Rosenbauer's RTX platform offering identical pump-rating performance to diesel models. Tankers remain indispensable where hydrant networks are sparse, and ladder platforms satisfy growing urban skylines, including Bronto Skylift's 230-foot reach that covers 20-story buildings.

Modern rescue units embed hydraulic extrication tools and battery-powered cutting devices, reducing scene set-up time. Demand is also rising for combination apparatus that blend pumper, tanker and rescue functions to save procurement budgets and station footprints. Wildland trucks add auxiliary pumps that deliver water while the vehicle is moving, a feature vital during fast-moving fires. ARFF vehicles command premium pricing due to FAA Part 139 standards that mandate stringent acceleration and foam-delivery benchmarks. With incremental innovation, the pumper's share of the fire truck market is likely to remain above one-third through the forecast horizon.

Residential & commercial protection accounted for 56.90% of 2025 revenues, making it the largest single application inside the fire truck market. Fire service mandates for dense urban cores keep order flow steady, and new building codes continue to shift equipment needs toward higher pump capacity and integrated decontamination systems.

Wildland & forestry, however, is expanding at 7.86% CAGR as climate patterns intensify severity and length of fire seasons. Vehicle designs incorporate greater ground clearance, reinforced underbodies and pump-and-roll capacity so crews can attack advancing flames without stopping. Federal grants tied to wildfire mitigation programs sustain procurement budgets even during municipal revenue downturns. Industrial applications demand chemical-proof seals and fire suppression agents compatible with class B hazards, while airports continue ordering ARFF units compliant with fluorine-free foam requirements set by the FAA's ongoing F3 transition initiative. Taken together, these shifts demonstrate how diverse risk profiles shape the evolving fire truck market.

The Fire Truck Market Report is Segmented by Type (Pumpers, Tankers, Rescue Trucks, and More), Application (Residential and Commercial, Airports, Military, and More), Propulsion (Internal Combustion Engine (ICE), Hybrid, and More), End-User (Municipal Fire Departments and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 33.95% of 2025 revenue, benefiting from mature emergency-services funding and advanced technology trials. The region hosts the bulk of early electric deployments, reinforcing its role as a bellwether for future global adoption patterns. Ongoing federal infrastructure programs provide supplemental funding to replace apparatus older than 20 years, keeping the order pipeline resilient.

Asia-Pacific, recording a 7.72% CAGR, is rapidly scaling municipal fire services to match urbanization in China, India and Southeast Asia. China's tier-2 and tier-3 cities allocate capital to expand station networks and invest in pumpers and aerials designed for dense, high-rise districts. India issues regular tenders that prioritize local assembly, encouraging joint ventures between global OEMs and domestic chassis suppliers. Emerging interest in battery-electric commercial vehicles at a robust CAGR hints at a budding market for zero-emission apparatus once charging infrastructure matures.

Europe remains a large yet slower-growing arena focused on green compliance and replacement rather than fleet expansion. Tightening emissions rules and NFPA-aligned standards influence procurement criteria, stimulating uptake of Euro-VI engines and hybrid drives. The Middle East & Africa register steady orders linked to expanding urban footprints and industrial megaprojects, while South America's demand is tempered by macroeconomic volatility. Collectively, these regional trajectories underscore the geographic diversity underpinning the fire truck market.

- Rosenbauer International AG

- Oshkosh Corporation (Pierce)

- REV Group

- Morita Holdings Corporation

- Magirus GmbH

- W.S. Darley & Co.

- KME (Kovatch Mobile Equipment)

- Sutphen Corporation

- Gimaex GmbH

- Albert Ziegler GmbH

- Bronto Skylift Oy

- NAFFCO

- Emergency One UK Ltd

- Weihai Guangtai

- Iturri Group

- Zhongtian Heavy Industry

- Sides S.A.

- BAI Brescia Antincendi International

- Fouts Bros Fire Equipment

- Alexis Fire Equipment

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent global & regional fire-safety regulations

- 4.2.2 Rising frequency & severity of wildfires

- 4.2.3 Growing adoption of electric fire trucks

- 4.2.4 Rapid replacement of ageing municipal fleets in Europe

- 4.2.5 Urban high-rise construction boosting aerial truck demand

- 4.2.6 Integration of IoT-telematics for fleet optimisation

- 4.3 Market Restraints

- 4.3.1 High upfront cost of next-gen (EV / hybrid) platforms

- 4.3.2 Semiconductor & chassis supply-chain disruptions

- 4.3.3 Shortage of skilled emergency-vehicle operators

- 4.3.4 Tight municipal budgets in developing economies

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 Pumpers

- 5.1.2 Tankers

- 5.1.3 Rescue Trucks

- 5.1.4 Aerial / Platform Trucks

- 5.1.5 Multi-tasking Modular Trucks

- 5.1.6 Wildland Fire Trucks

- 5.1.7 Airport Crash Tender (ARFF)

- 5.2 By Application

- 5.2.1 Residential & Commercial

- 5.2.2 Industrial & Manufacturing

- 5.2.3 Airports

- 5.2.4 Military

- 5.2.5 Wildland & Forestry

- 5.3 By Propulsion

- 5.3.1 Internal Combustion Engine (ICE)

- 5.3.2 Hybrid

- 5.3.3 Battery Electric

- 5.3.4 Fuel-Cell Electric

- 5.4 By End-User

- 5.4.1 Municipal Fire Departments

- 5.4.2 Industrial Facility Brigades

- 5.4.3 Airport Authorities

- 5.4.4 Defense & Military

- 5.4.5 Contract & Private Fire Services

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Rosenbauer International AG

- 6.4.2 Oshkosh Corporation (Pierce)

- 6.4.3 REV Group

- 6.4.4 Morita Holdings Corporation

- 6.4.5 Magirus GmbH

- 6.4.6 W.S. Darley & Co.

- 6.4.7 KME (Kovatch Mobile Equipment)

- 6.4.8 Sutphen Corporation

- 6.4.9 Gimaex GmbH

- 6.4.10 Albert Ziegler GmbH

- 6.4.11 Bronto Skylift Oy

- 6.4.12 NAFFCO

- 6.4.13 Emergency One UK Ltd

- 6.4.14 Weihai Guangtai

- 6.4.15 Iturri Group

- 6.4.16 Zhongtian Heavy Industry

- 6.4.17 Sides S.A.

- 6.4.18 BAI Brescia Antincendi International

- 6.4.19 Fouts Bros Fire Equipment

- 6.4.20 Alexis Fire Equipment

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment