PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851760

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851760

Flexible Pipe - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

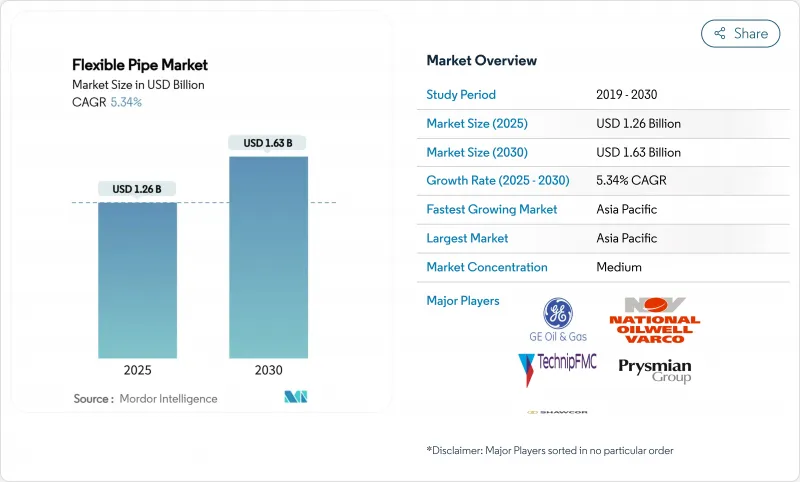

The flexible pipe market size stands at USD 1.26 billion in 2025 and is projected to climb to USD 1.63 billion by 2030, representing a 5.34% CAGR through the forecast period.

This growth is traced to deep- and ultra-deepwater exploration programs, rapid material innovation that mitigates corrosion, and expansion in pre-salt developments in Brazil and Guyana. Industry leaders are embedding fiber-optic sensors that deliver real-time integrity data, reducing downtime while lengthening asset life. Asia-Pacific holds the pre-eminent position, propelled by offshore programs in China, India, and Australia and supported by domestic manufacturing that lowers logistics costs. On the materials front, High-Density Polyethylene (HDPE) remains the default choice for operators, yet carbon-fiber and other composite solutions are gaining traction as weight-saving imperatives intensify. Accelerating vertical-integration strategies, such as the proposed Saipem-Subsea7 merger, are redrawing competitive lines by aligning engineering, procurement, construction, and installation (EPCI) capabilities inside one corporate umbrella.

Global Flexible Pipe Market Trends and Insights

Growing Deep- and Ultra-Deepwater Developments

Operators are sanctioning projects beyond 1,500 m as rigid steel systems become uneconomic in complex seabed topography. Chevron's Anchor field inaugurated 20 ksi subsea hardware that sets a new performance bar for the flexible pipe market. Brazil's pre-salt reservoirs impose CO2-driven corrosion stresses at 2,900 m depth, favoring suppliers with proven composite technology. System-level contracting models such as TechnipFMC's iEPCI compress schedules by up to 20%, reinforcing demand for integrated flexible solutions.

Replacement of Corroded Steel Lines with Composites

Annual offshore corrosion expenses reach USD 2.5 billion, elevating the economics of composite retrofits that sidestep cathodic protection. Saipem's plastic-lined pipeline technology trims costs by 40% while sustaining 1,000 bar ratings. North Sea operators confront a 10,000 km legacy grid dating back pre-1990; flexible pipe systems slot into existing corridors without heavy-lift spreads, cutting retrofit downtime. Embedded sensors inside Baker Hughes' non-metallic products feed integrity analytics that replace labor-intensive inspection rounds.

Crude-Oil Price Volatility Curbs CAPEX

Price swings in the USD 70-90 per-barrel band delay final investment decisions as boards now demand 18-24 months' price stability before greenlighting offshore projects. Higher interest rates lift hurdle thresholds, further deferring sanctioning. Mature North Sea and Gulf of Mexico fields are particularly vulnerable because flexible pipes constitute up to 20% of total project CAPEX, rendering economics price sensitive.

Other drivers and restraints analyzed in the detailed report include:

- SURF Megaproject Pipeline in Brazil and Guyana

- Embedded Fibre-Optic Health Monitoring

- Higher Upfront Cost Versus Rigid Steel

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flexible pipe market size for HDPE reached USD 0.45 billion in 2024, translating into 35.75% revenue dominance. Operators value HDPE for cost-efficient extrusion, chemical inertia, and weld-free joints. Still, Other Materials-chiefly carbon-fiber and advanced polymers-record an 8.42% CAGR, outstripping incumbents as floating production systems chase mass savings to ease topside loading. University of Sydney forecasts CFRP waste streams hitting 500,000 t by 2030, intensifying circular-economy pressures that could redirect R&D toward recyclable resins.

Material innovators push flexible pipe market share gains by enhancing fatigue life and temperature windows. Advanced PA and PVDF layers deliver 130 °C service, expanding flexible deployment into high-HTHP wells. Thermoplastic composite pipes (TCP) marry carbon-fiber tensile casing with a PA12 liner to achieve zero corrosion and low-friction flow profiles. As deepwater activity scales, composite uptake is expected to raise Other Materials' contribution to one-third of the flexible pipe market by 2030.

Unbonded architectures accounted for 45.65% of global revenue in 2024, capitalizing on multilayered armor that decouples hoop and axial loads. Their repairability underpins preference in dynamic riser applications. Yet Reinforced Thermoplastic Pipes, devoid of metallic carcasses, expand 7.34% CAGR as operators target corrosion-free performance and lighter deck loads. FlexSteel's spoolable RTP solutions eliminate anodes and coating campaigns, lowering OPEX in brownfield tie-ins.

Structural choice in the flexible pipe market hinges on fatigue, pressure, and chemical exposure profiles. Bonded pipes serve niche ultra-high-pressure flowlines but are handicapped by limited field repair options and higher cost. Innovations in aramid and glass-fiber winding, coupled with digital twins tracking fatigue accumulation, will allow RTP to penetrate riser duty where strength limits once blocked entry.

The Flexible Pipes Market Report is Segmented by Material Type (High-Density Polyethylene, Polyamide, and More), Pipe Structure Type (Unbonded Flexible Pipe, Bonded Flexible Pipe, Reinforced Thermoplastic Pipe), Functional Application (Flowlines, Risers, Jumpers and Tie-Ins, Export/Loading Hoses), Installation Environment (Offshore, Onshore), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained 38.23% of 2024 revenue on the back of South China Sea deepwater blocks and Australian LNG backfill programs. The region's flexible pipe market size is forecast to rise at an 8.35% CAGR, outpacing all others. Government policy favoring local content spurs construction of regional manufacturing hubs, such as TechnipFMC's plant in Southeast Asia that shortens reel-lay lead times for Chinese and Indian operators. Growing offshore wind deployment in Japan and Korea creates spill-over demand for subsea power cables and dynamic umbilicals, further nurturing composite capability cross-fertilization.

North America follows as the second-largest region, underpinned by Gulf of Mexico ultra-deepwater sanctions that require 20 ksi flexible jumpers. Anadarko basin gathering lines and Permian hydrogen demonstration projects drive onshore spoolable adoption. Yet regional CAGR lags Asia-Pacific because the replacement wave in the Gulf is offset by plateauing discovery rates.

Europe shows balanced growth built on North Sea life-extension projects and nascent hydrogen backbone pilots across Norway and the United Kingdom. Strict decommissioning legislation accelerates removal of ageing steel, offering retrofit openings for flexible line substitution in tie-back schemes. Recycling mandates, however, require suppliers to propose closed-loop models for polymer recovery, potentially elevating total installed cost.

Middle East and Africa register rapid adoption as QatarEnergy's North Field Compression Program and West Africa's FPSO campaigns solicit corrosion-immune composites. Saipem's USD 4 billion EPC award in Qatar confirms regional appetite for high-specification flowlines and optic-fiber-infused umbilicals. Turkey's Sakarya Phase 2 calls for 158 km of 2,200 m-rated pipe, signalling Black Sea basin maturation. South America, anchored by Brazil's pre-salt and Guyana's Stabroek block, remains a central pillar, accounting for the bulk of global SURF backlogs and reinforcing manufacturers' decision to co-locate spool-bases near Rio.

- TechnipFMC plc

- National Oilwell Varco (NOV)

- Saipem S.p.A.

- Prysmian Group

- Shawcor Ltd

- Strohm (formerly Airborne Oil & Gas)

- Magma Global Ltd

- SoluForce BV

- ContiTech AG

- Chevron Phillips Chemical Co.

- FlexSteel Pipeline Technologies Inc.

- GE Oil & Gas (Baker Hughes)

- Aker Solutions ASA

- Wellstream Processing (NOV)

- Subsea 7 S.A.

- Oceaneering International

- Hunan Great Steel Pipe Co.

- JDR Cable Systems Ltd

- Polyflow LLC

- Cosmoplast Industrial Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing deep- and ultra-deepwater developments

- 4.2.2 Replacement of corroded steel lines with composites

- 4.2.3 SURF megaproject pipeline in Brazil and Guyana

- 4.2.4 Carbon-fibre armoured pipes lighten FPSOs

- 4.2.5 Embedded fibre-optic health monitoring

- 4.2.6 Hydrogen and CO2 transport demand for flexibles

- 4.3 Market Restraints

- 4.3.1 Crude-oil price volatility curbs CAPEX

- 4.3.2 Higher upfront cost versus rigid steel

- 4.3.3 Polymer-pipe end-of-life recycling gaps

- 4.3.4 Tight capacity for 20 k-psi rated pipes

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 High-Density Polyethylene (HDPE)

- 5.1.2 Polyamide (PA)

- 5.1.3 Polyvinylidene Fluoride (PVDF)

- 5.1.4 Others Material Type

- 5.2 By Pipe Structure Type

- 5.2.1 Unbonded Flexible Pipe

- 5.2.2 Bonded Flexible Pipe

- 5.2.3 Reinforced Thermoplastic Pipe (RTP)

- 5.3 By Functional Application

- 5.3.1 Flowlines

- 5.3.2 Risers

- 5.3.3 Jumpers and Tie-ins

- 5.3.4 Export / Loading Hoses

- 5.4 By Installation Environment

- 5.4.1 Offshore

- 5.4.1.1 Shallow Water (Less than 500 m)

- 5.4.1.2 Deepwater (500-1500 m)

- 5.4.1.3 Ultra-deepwater (More than 1500 m)

- 5.4.2 Onshore

- 5.4.1 Offshore

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 United Arab Emirates

- 5.5.4.1.2 Saudi Arabia

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Nigeria

- 5.5.4.2.3 Egypt

- 5.5.4.2.4 Rest of Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 TechnipFMC plc

- 6.4.2 National Oilwell Varco (NOV)

- 6.4.3 Saipem S.p.A.

- 6.4.4 Prysmian Group

- 6.4.5 Shawcor Ltd

- 6.4.6 Strohm (formerly Airborne Oil & Gas)

- 6.4.7 Magma Global Ltd

- 6.4.8 SoluForce BV

- 6.4.9 ContiTech AG

- 6.4.10 Chevron Phillips Chemical Co.

- 6.4.11 FlexSteel Pipeline Technologies Inc.

- 6.4.12 GE Oil & Gas (Baker Hughes)

- 6.4.13 Aker Solutions ASA

- 6.4.14 Wellstream Processing (NOV)

- 6.4.15 Subsea 7 S.A.

- 6.4.16 Oceaneering International

- 6.4.17 Hunan Great Steel Pipe Co.

- 6.4.18 JDR Cable Systems Ltd

- 6.4.19 Polyflow LLC

- 6.4.20 Cosmoplast Industrial Co.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment