PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851798

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851798

Internet Of Medical Things - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

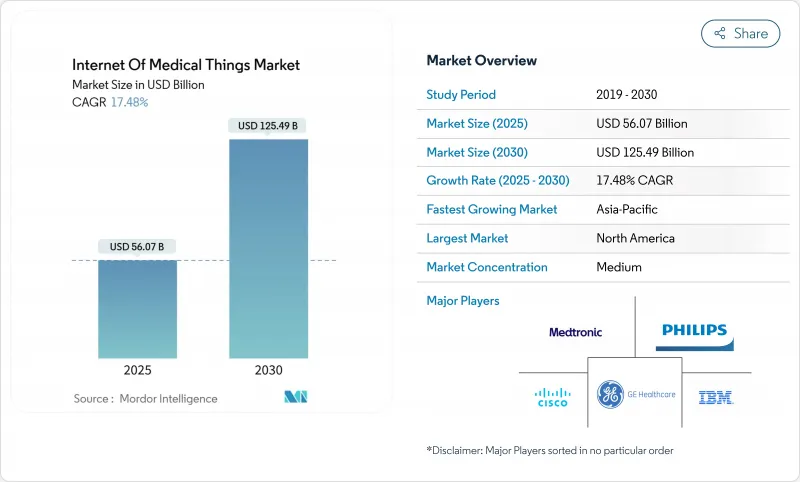

The Internet Of Medical Things Market size is estimated at USD 56.07 billion in 2025, and is expected to reach USD 125.49 billion by 2030, at a CAGR of 17.48% during the forecast period (2025-2030).

Strong momentum reflects healthcare providers' shift to connected-care models that blend real-time data analytics with remote monitoring to curb costs and improve outcomes. Growth also benefits from ultra-low-power AI sensors, private 5G rollouts across hospital campuses, and cyber-insurance requirements that compel full device visibility. New reimbursement rules that reward measurable outcome improvements keep capital flowing into connected solutions, while semiconductor shortages spur innovation in edge architectures that reduce hardware dependencies. Regionally, North America sustains leadership through mature infrastructure and favorable regulation, yet Asia Pacific registers the fastest expansion as 5G investments and government-backed digital-health programs accelerate adoption.

Global Internet Of Medical Things Market Trends and Insights

Cost-reduction Pressure on Global Healthcare Systems

Healthcare providers face steep cost escalation, with United States supply-chain disruptions pushing expenses up by 15% in 2025. Connected devices cut unplanned downtime through predictive maintenance and real-time asset tracking, as illustrated by RWJBarnabas Health's USD 9 million savings after deploying a location system that eliminated device losses. Value-based reimbursement amplifies adoption because hospitals must document outcome improvements alongside cost controls. Capital budgets consequently treat the Internet of Medical Things market as essential infrastructure, prompting multiyear procurement commitments. Insurers further link reimbursement to documented savings, reinforcing a cycle that channels operating funds to connected platforms.

Proliferation of Connected Wearables and Implantables

Breakthroughs in wireless power and miniaturized sensor arrays now permit battery-free devices that transmit only relevant data, conserving bandwidth and energy. Brown University demonstrated salt-sized sensors capable of monitoring intracranial pressure and glucose simultaneously, enabling continuous care without recurrent surgery. Consumer demand for preventive health data broadens deployment beyond clinical settings, ensuring the Internet of Medical Things market finds growth in wellness as well as disease management. Device makers embed edge AI that filters noise before transmission, reducing cloud-processing costs. Regulatory pathways are smoothing as real-world performance data accumulates, shortening approval cycles for next-generation implants.

Shortage of In-house IoT Skills in Provider Organisations

Thirty percent of healthcare enterprises cite data-security expertise shortages as an adoption hurdle. Smaller hospitals struggle to recruit cyber-literate engineers, widening the gap between resource-rich systems and rural facilities. Managed services bridge some needs but introduce vendor-lock risks and subscription overhead. Talent deficits are pronounced in Southeast Asia despite high investment intent. Without robust in-house teams, deployment timelines extend, slowing Internet of Medical Things market penetration.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Outcomes-based and Remote Patient-Monitoring Models

- Roll-out of Private 5G and Edge Networks in Hospitals

- Escalating Ransomware Premiums Diverting IoMT Budgets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Implantable devices represent the fastest-growing segment, projected to expand at 19.6% CAGR through 2030, while wearables maintained leadership with 27% share of the Internet of Medical Things market size in 2024. Wireless power transfer and sub-millimeter sensors eliminate battery replacements and support continuous multi-parameter measurement arxiv.org. Stationary in-hospital systems remain connectivity hubs for network orchestration, ensuring data integrity across thousands of endpoints.

The University of California's ultrasound-powered fluorescence sensor shows how deep-tissue imaging can guide cancer therapy without external leads. Wearables absorb these advances, combining sensor fusion with edge analytics to issue timely alerts. Emerging smart contact lenses and biodegradable probes add niche opportunities that diversify the Internet of Medical Things market. Regulatory approvals favor implants that demonstrate longitudinal safety and outcome benefits, encouraging sustained R&D spending.

Vital-sign monitoring products held a 32.5% share in 2024, demonstrating their role as baseline tools across care settings. Implantable cardiac devices are slated to grow at a 17.8% CAGR, supported by closed-loop neuromodulation that optimizes therapy based on real-time neural feedback. Respiratory monitors gain relevance due to rising COPD prevalence, while anaesthesia machines integrate connected sensors to enhance intraoperative safety.

Predictive maintenance algorithms applied to imaging systems and ventilators reduce downtime and extend asset life. Smart pill dispensers and connected rehabilitation gear broaden engagement beyond acute care, adding recurring revenue streams for vendors. Together, these dynamics elevate the Internet of Medical Things market and enhance cross-device ecosystem value.

The Internet of Medical Things Market Report is Segmented by Device Type (Wearable Devices, Stationary/In-Hospital Devices, Implantable Devices, and Other Device Types), Product Type (Vital Signs Monitoring Devices, Implantable Cardiac Devices, and More), End Users (Hospitals, Clinics, and More), Connectivity Technology (Zigbee, Bluetooth, Wi-Fi, and More), and Geography.

Geography Analysis

North America commanded a 38.7% share in 2024, propelled by mature health-IT infrastructure and regulatory pathways that encourage interoperability. Public-private alliances fast-track private-5G pilots and AI-enabled diagnostics. Canada and Mexico add momentum through government-funded telehealth initiatives, while rising cyber-insurance premiums and semiconductor shortages temper near-term device rollouts. Legacy system integration remains a capital-intensive obstacle, yet strong reimbursement models keep the Internet of Medical Things market advancing.

Asia Pacific is the fastest-growing region at a 21.36% CAGR. China's 2024 medical-informatization spending surpassed CNY 800 billion, underscoring state support. Japan and South Korea leverage advanced manufacturing to deliver next-generation sensors, and India's national EHR rollout aids standardization. Skilled-personnel shortages persist, but cross-border training and cloud-based managed services lessen the gap. Regional collaboration spreads best practices, ensuring broad participation in the expanding Internet of Medical Things market.

Europe records steady gains supported by Medical Device Regulation compliance that clarifies connected-device requirements. Germany, the United Kingdom, and France lead adoption through funded modernization programs, while Italy and Spain tap EU stimulus to upgrade infrastructure. Strict data-privacy laws elevate implementation costs yet build patient trust. Switzerland's Kantonsspital Baden installed more than 7,000 sensors with Siemens, proving the scalability of smart-hospital visions. Harmonized policies let smaller economies piggyback on regional frameworks, sustaining Internet of Medical Things market momentum across the continent.

- GE Healthcare

- Koninklijke Philips N V

- Medtronic plc

- Cisco Systems Inc.

- IBM Corporation

- Siemens Healthineers

- Hill-Rom /Welch Allyn

- Boston Scientific Corp.

- Johnson and Johnson (JandJ MedTech)

- Biotronik SE

- Abbott Laboratories

- Dexcom Inc.

- ResMed Inc.

- Apple Inc.

- Fitbit (Google LLC)

- Qualcomm Life

- Honeywell International

- Capsule Technologies

- Ordr Inc.

- Armis Security

- Cynerio Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cost-reduction pressure on global healthcare systems

- 4.2.2 Proliferation of connected wearables and implantables

- 4.2.3 Shift to outcomes-based and remote patient monitoring models

- 4.2.4 Roll-out of private-5G/edge networks in hospitals

- 4.2.5 Ultra-low-power AI sensor chips enabling multi--parameter implantables

- 4.2.6 Mandatory cyber-insurance clauses demanding IoMT visibility

- 4.3 Market Restraints

- 4.3.1 Shortage of in-house IoT skills in provider organisations

- 4.3.2 High upfront infrastructure and device costs

- 4.3.3 Fragmented data-interoperability standards

- 4.3.4 Escalating ransomware premiums diverting IoMT budgets

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Assessment of COVID-19 and Endemic Virus Impact

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Type

- 5.1.1 Wearable Devices

- 5.1.2 Stationary/In-Hospital Devices

- 5.1.3 Implantable Devices

- 5.1.4 Other Device Types

- 5.2 By Product Type

- 5.2.1 Vital Signs Monitoring Devices

- 5.2.2 Implantable Cardiac Devices

- 5.2.3 Respiratory Devices

- 5.2.4 Anaesthetic Machines

- 5.2.5 Imaging Systems

- 5.2.6 Ventilators

- 5.2.7 Other Products

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Clinics

- 5.3.3 Nursing Homes

- 5.3.4 Long-Term Care Centers

- 5.3.5 Home Care Settings

- 5.4 By Connectivity Technology

- 5.4.1 Zigbee

- 5.4.2 Bluetooth

- 5.4.3 Wi-Fi

- 5.4.4 Cellular IoT/LPWAN

- 5.4.5 Other Technologies

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Nigeria

- 5.5.4.2.3 Kenya

- 5.5.4.2.4 Rest of Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 GE Healthcare

- 6.4.2 Koninklijke Philips N V

- 6.4.3 Medtronic plc

- 6.4.4 Cisco Systems Inc.

- 6.4.5 IBM Corporation

- 6.4.6 Siemens Healthineers

- 6.4.7 Hill-Rom /Welch Allyn

- 6.4.8 Boston Scientific Corp.

- 6.4.9 Johnson and Johnson (JandJ MedTech)

- 6.4.10 Biotronik SE

- 6.4.11 Abbott Laboratories

- 6.4.12 Dexcom Inc.

- 6.4.13 ResMed Inc.

- 6.4.14 Apple Inc.

- 6.4.15 Fitbit (Google LLC)

- 6.4.16 Qualcomm Life

- 6.4.17 Honeywell International

- 6.4.18 Capsule Technologies

- 6.4.19 Ordr Inc.

- 6.4.20 Armis Security

- 6.4.21 Cynerio Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment