PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851801

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851801

Robot Operating System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

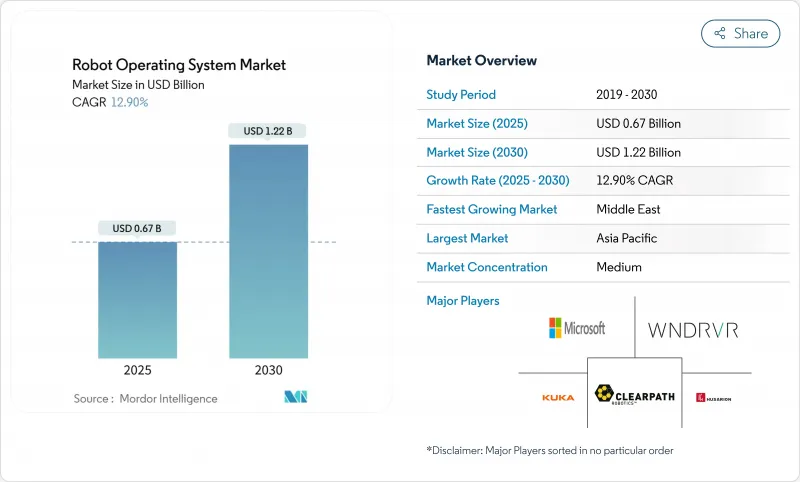

The robot operating system market size is estimated at USD 0.67 billion in 2025 and is forecast to reach USD 1.22 billion by 2030, advancing at a 12.9% CAGR.

Growth stems from rising industrial automation, wider interoperability requirements, and the shift toward open, modular software that lets robots adapt to changing floor-shop conditions without extensive re-engineering. Advances in edge computing and 5G are pulling real-time control closer to the robot, while cloud simulation and Robot-as-a-Service models lower entry barriers for firms new to robotics. The wide availability of ROS-Industrial libraries is standardizing motion, perception, and safety functions, accelerating deployment times. Automotive, electronics, and healthcare producers are leading adopters because they balance high volumes with a need for flexible tooling. Platform vendors that bundle long-term support, security hardening, and update orchestration are carving out premium service positions as ROS 1 approaches end-of-life in May 2025.

Global Robot Operating System Market Trends and Insights

Growing Adoption of ROS-enabled Cobots in Automotive Assembly Lines

Automotive groups are boosting collaborative-robot deployment to improve takt times and address skilled-labour gaps. Volkswagen, General Motors, and Tesla have integrated ROS-based cobots for gluing, inspection, and screw-fastening tasks, lifting station throughput and maintaining high first-pass yields. Stellantis demonstrated a 27% assembly-efficiency gain by synchronizing mobile manipulators with augmented-reality guidance and digital-twin feedback at its Mirafiori plant. Cobots configured with ROS 2 benefit from DDS middleware, which removes single points of failure and enables live safety-parameter updates. Growth remains linked to falling sensor costs and plug-and-play tooling that cuts integration time for mixed-model lines.

Expansion of Cloud-based Simulation Platforms

Industrial developers increasingly validate full robot workloads in virtual environments before placing hardware on a factory floor. The FogROS2-FT framework offloads compute-heavy motion-planning queries to multiple cloud endpoints, reducing simulation costs by 2.2X and strengthening fault tolerance. AWS RoboMaker and similar services attach continuous-integration hooks, so each code commit triggers automated regression tests, shortening development sprints. Developers use these pipelines to iterate perception and grasping algorithms without halting physical production lines, accelerating go-live timelines for new SKUs.

Cyber-Security Vulnerabilities in Distributed ROS Networks

ROS 1 nodes rely on unencrypted TCPROS topics that can be spoofed or replayed, exposing safety-critical actuators. Although ROS 2 embeds authentication and access-control plugins through DDS, misconfigurations remain common when fleets span multiple VLANs. Recent penetration tests revealed weak certificate management in healthcare robotics deployments, prompting operators to institute zero-trust policies, segmented networks, and real-time anomaly detection. Industry consortia now issue hardening guides, yet small and medium manufacturers often lack cyber-security personnel to apply recommended patches.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Government-Funded Robotics Testbeds

- Integration of ROS 2 with 5G and Edge-AI for AMRs

- Scarcity of Certified ROS Talent in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Industrial robots contributed 57% of 2024 revenue, reflecting long-established use in welding, palletizing, and CNC tending tasks. FANUC's one-millionth unit milestone underscores the scale and installed base maturity. Within that cohort, cobots represent one-quarter of automotive deployments, highlighting the push toward human-machine collaboration on mixed-model lines. Service robots, particularly logistics AMRs and hospital couriers, are set to post a 16.8% CAGR through 2030, propelled by e-commerce fulfilment pressures and patient-care quality initiatives.

Service-segment momentum is evident in rising deployments of navigation-ready platforms paired with AI vision for shelf-restocking and autonomous cleaning. Vendors leverage ROS 2's real-time quality-of-service settings to keep SLAM maps consistent across large facilities. The Robot operating system market size for service units serving professional environments is forecast to expand rapidly as subscription pricing aligns with facility-management budgets. Industrial manufacturers increasingly bundle analytics dashboards, adding predictive-maintenance overlays that sharpen uptime metrics.

Automotive producers accounted for a commanding 24% slice of 2024 revenue, using ROS-based motion planning and quality-inspection pipelines to manage higher model variants without line stoppages. Hexapod alignment systems support headlamp calibration and optical-sensor positioning needed for driver-assistance features. Connected automated vehicle demonstrators further show how AMR tuggers synchronized by ROS 2 can replenish parts bins just-in-time, lifting throughput across end-of-line stations.

Healthcare records the steepest ascent with a 15.91% CAGR. ROS-based surgical assistants employ deterministic loop timing to coordinate multi-axis tool paths, meeting stringent kinematic accuracy targets. Hospital logistics platforms such as PeTRA combine ROS 2 with advanced HRI modules to navigate crowds and respond to patient vitals in real time. As providers digitize operating rooms, the Robot operating system market size for healthcare robotics is expected to broaden into diagnostics and rehabilitation.

Robot Operating System Market Segmented by Robot Type (Industrial Robots, Service Robots), End-User Industry (Automotive, and More), Component (Software Stack, Services), Deployment Mode (On-Premise, Cloud), Operating System Distribution (ROS 1, and More), Hardware Architecture Support (x86, and More) and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 38% of global revenue in 2024 due to heavy automation investment in China, Japan, and South Korea. Shanghai's ROSCon China attracted more than 200 firms, signifying local community depth. Government funding accelerates adoption: South Korea's Tech Valley subsidies underwrite AI inference accelerators for small-batch electronics plants, while Singapore's ART C testbeds trial advanced 3D vision libraries. The Robot operating system market size in the region is projected to keep pace as domestic suppliers extend low-cost arms into ASEAN manufacturing corridors.

The Middle East records the fastest 17.1% CAGR through 2030. National programs such as Saudi Arabia's Vision 2030 and the UAE's Operation 300bn lean on robotics to diversify away from hydrocarbons. Government-backed demonstration zones in Dubai simplify regulatory compliance, allowing rapid pilot launch for warehouse and surgical robots. Regional system integrators partner with European component makers to localize supply chains, reinforcing self-sufficiency goals.

North America remains an innovation nucleus, hosting core ROS maintainers and hyperscale cloud providers. The ROS-Industrial Consortium Americas showcases open-source quality-assurance pipelines to a membership spanning aerospace, oil & gas, and food processing. Universities funnel research on adaptive manipulation into spin-offs that secure venture capital, sustaining a rich start-up pipeline. Demand is further buoyed by reshoring initiatives and tax incentives for advanced manufacturing equipment.

Europe combines strong industrial-robot density with government mandates for cyber-secure automation. Germany alone houses one-third of Europe's installed base and pushes ROS-based retrofits as part of its Industrie 4.0 framework. Countries such as Spain and Hungary logged double-digit robot-stock growth in 2024. Conferences in Odense underscore collaborative R&D, linking Danish cobot makers with AI researchers to commercialize adaptive pick-and-place functions.

- Microsoft Corporation

- Amazon Web Services Inc.

- Clearpath Robotics Inc.

- KUKA AG

- Bosch Rexroth AG

- ABB Ltd.

- FANUC Corp.

- Yaskawa Electric Corp.

- Universal Robots A/S

- Open Robotics (Intrinsic)

- Wind River Systems Inc.

- Husarion Inc.

- Brain Corporation

- Neobotix GmbH

- PAL Robotics SL

- Locus Robotics Corp.

- Milvus Robotics

- iRobot Corporation

- Omron Corporation

- Siasun Robot & Automation

- Fetch Robotics (Zebra)

- Teradyne Mobility (AGV)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of ROS-enabled Cobots in Automotive Assembly Lines (Asia)

- 4.2.2 Expansion of Cloud-based Simulation Platforms (North America and Europe)

- 4.2.3 Surge in Government-funded Robotics Testbeds (APAC and Middle East)

- 4.2.4 Integration of ROS 2 with 5G & Edge-AI for AMRs (Global)

- 4.2.5 Rapid Proliferation of Open-Source Industrial Libraries (ROS-Industrial)

- 4.2.6 Vendor Shift toward Long-Term Support (LTS) Distributions

- 4.3 Market Restraints

- 4.3.1 Cyber-Security Vulnerabilities in Distributed ROS Networks

- 4.3.2 Fragmented Hardware Abstraction Layers Across OEMs

- 4.3.3 Scarcity of Certified ROS Talent in Emerging Markets

- 4.3.4 Real-Time Determinism Challenges in Safety-Critical Apps

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Robot Type

- 5.1.1 Industrial Robots

- 5.1.1.1 Articulated

- 5.1.1.2 SCARA

- 5.1.1.3 Parallel/Delta

- 5.1.1.4 Cartesian/Linear

- 5.1.1.5 Collaborative Robots (Cobots)

- 5.1.2 Service Robots

- 5.1.2.1 Professional Service Robots

- 5.1.2.1.1 Logistics Robots

- 5.1.2.1.2 Healthcare and Medical Robots

- 5.1.2.1.3 Defense and Security Robots

- 5.1.2.1.4 Agricultural Robots

- 5.1.2.2 Personal and Domestic Service Robots

- 5.1.1 Industrial Robots

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.2 Electrical and Electronics

- 5.2.3 Healthcare and Life Sciences

- 5.2.4 E-commerce and Logistics

- 5.2.5 Aerospace and Defense

- 5.2.6 Food and Beverage

- 5.2.7 Agriculture

- 5.2.8 Education and Research

- 5.2.9 Others (Metal, Plastics, etc.)

- 5.3 By Component

- 5.3.1 Software Stack

- 5.3.1.1 Core ROS Libraries

- 5.3.1.2 Middleware / Communication Tools

- 5.3.1.3 Simulation & Visualization (Gazebo, RViz)

- 5.3.2 Services

- 5.3.2.1 System Integration and Consulting

- 5.3.2.2 Support and Maintenance

- 5.3.2.3 Training and Certification

- 5.3.1 Software Stack

- 5.4 By Operating System Distribution

- 5.4.1 ROS 1

- 5.4.2 ROS 2

- 5.4.3 Other Variants (ROS-Industrial, micro-ROS)

- 5.5 By Hardware Architecture Support

- 5.5.1 x86

- 5.5.2 ARM

- 5.5.3 RISC-V and Others

- 5.6 By Deployment Mode

- 5.6.1 On-premise

- 5.6.2 Cloud-based (ROS-aaS)

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Rest of Europe

- 5.7.4 Nordics

- 5.7.4.1 Sweden

- 5.7.4.2 Norway

- 5.7.4.3 Denmark

- 5.7.4.4 Finland

- 5.7.4.5 Iceland

- 5.7.5 Middle East

- 5.7.5.1 GCC

- 5.7.5.2 Turkey

- 5.7.5.3 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Rest of Africa

- 5.7.7 Asia-Pacific

- 5.7.7.1 China

- 5.7.7.2 Japan

- 5.7.7.3 South Korea

- 5.7.7.4 India

- 5.7.7.5 Indonesia

- 5.7.7.6 Rest of Asia-Pacific

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Amazon Web Services Inc.

- 6.4.3 Clearpath Robotics Inc.

- 6.4.4 KUKA AG

- 6.4.5 Bosch Rexroth AG

- 6.4.6 ABB Ltd.

- 6.4.7 FANUC Corp.

- 6.4.8 Yaskawa Electric Corp.

- 6.4.9 Universal Robots A/S

- 6.4.10 Open Robotics (Intrinsic)

- 6.4.11 Wind River Systems Inc.

- 6.4.12 Husarion Inc.

- 6.4.13 Brain Corporation

- 6.4.14 Neobotix GmbH

- 6.4.15 PAL Robotics SL

- 6.4.16 Locus Robotics Corp.

- 6.4.17 Milvus Robotics

- 6.4.18 iRobot Corporation

- 6.4.19 Omron Corporation

- 6.4.20 Siasun Robot & Automation

- 6.4.21 Fetch Robotics (Zebra)

- 6.4.22 Teradyne Mobility (AGV)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment