PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940570

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940570

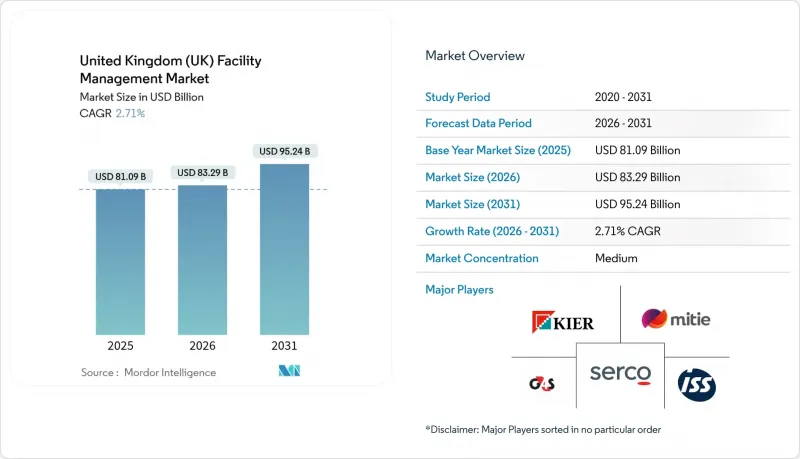

United Kingdom (UK) Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The United Kingdom facility management market was valued at USD 81.09 billion in 2025 and estimated to grow from USD 83.29 billion in 2026 to reach USD 95.24 billion by 2031, at a CAGR of 2.71% during the forecast period (2026-2031).

The measured trajectory signals a mature sector advancing under energy-efficiency mandates, digital transformation, and a sustained preference for outsourced service models. Hard services hold prime importance because ageing building stock demands strict mechanical, electrical, and plumbing upkeep to meet Minimum Energy Efficiency Standards, while soft services evolve quickly to address workplace well-being and stringent hygiene rules. Technology integration from IoT sensor grids to AI-powered analytics-cuts response times, trims energy consumption, and enables outcome-based contracts that grow revenue without proportionate head-count expansion. Outsourcing momentum continues as public and private clients seek specialist expertise that guarantees compliance and delivers cost certainty amid volatile input prices. Although Brexit-linked labour shortages and cost inflation compress margins, rising public-sector refurbishment funding and the spread of flexible workspaces offer expansion lanes for providers that innovate fast.

United Kingdom (UK) Facility Management Market Trends and Insights

Technology Integration (IoT, AI, Automation)

AI-driven building-management platforms are redefining service delivery, with the Intellectual Property Office cutting maintenance response times from 14 days to seconds after launching a digital work-order portal. Smart sensors relay live occupancy, temperature, and air-quality data, letting providers shift from reactive to predictive maintenance while lowering energy use and elevating employee comfort. CBRE's entry into hyperscale data-center facilities management underscores the high-margin potential in segments that demand 24-hour analytical monitoring. Healthcare and education clients lead adoption because compliance regimes mandate continuous environmental monitoring. As digital dashboards merge soft and hard services, providers package cleaning, security, office support, and asset maintenance into data-rich contracts that command price premiums.

Rapid Commercial Real Estate Expansion

Royal Institution of Chartered Surveyors data show occupier demand turned positive in Q1 2025, and prime office rents in Central London are projected to rise nearly 5% in the year. Industrial assets register the strongest investment appetite, with an +18% net balance in investor demand, propelled by e-commerce and near-shoring. New developments increase demand for commissioning, lifecycle asset management, and ongoing compliance auditing. Facility managers partnering early with developers secure multi-year revenue streams in smart-ready buildings that integrate ESG dashboards from day one. Logistics growth similarly drives tailored FM packages that combine inventory tracking technologies, dock management, and advanced fire-suppression maintenance for high-throughput warehouses.

Labor Shortages and Skill Gaps

Hospitality, cleaning, and catering units face 132,000 job vacancies post-Brexit, straining FM rosters. The 2025 Immigration White Paper raises the Skilled Worker visa threshold to RQF Level 6, curtailing access to international staff for entry-level FM roles. Employer training investment has fallen 28% since 2005, creating a skills deficit just as buildings adopt sophisticated digital systems. Firms counteract with supervisor academies such as JPC by Samsic's 12-module Next Gen programme focusing on leadership and technical upskilling. Nonetheless, high turnover and an aging workforce continue to limit sector capacity.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Outsourcing Trend

- Rising Focus on Workplace Experience and Employee Well-being

- Margin Pressure from Rising Operational Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard services held 60.12% of United Kingdom facility management market share in 2025, anchored by the NHS's GBP 11.6 billion (USD 3.19 billion) maintenance backlog and stringent EPC upgrade timelines. The United Kingdom facility management market size for hard-service contracts is poised to expand as 28% of commercial properties still rate D or lower on EPC scale, forcing accelerated mechanical, electrical, and plumbing overhauls. MEP and HVAC segments benefit from regulatory pathways to net-zero that mandate 47%-62% emissions cuts by 2035. Asset digitization further lifts demand for predictive-maintenance analytics, letting providers intervene before asset failure while meeting compliance reporting needs.

Soft services, while smaller today, are forecast to grow 2.78% CAGR through 2031, propelled by hospital-grade cleaning standards and workplace-experience innovations. Heightened infection-control rules elevate the premium for robotic disinfection systems and sensor-verified hygiene protocols. Co-working operators require smart access control, driving security-service modernization. Fire-safety upgrades tied to post-Grenfell legislation amplify demand for integrated alarm testing and evacuation-planning services. Together, these forces shift provider offerings toward comprehensive packages that merge soft-service excellence with data-backed compliance.

The United Kingdom Facility Management Market Report is Segmented by Service Type (Hard Services, Soft Services), Offering Type (In-House, Outsourced), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process, Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ISS UK

- Mitie Group PLC

- Serco Group PLC

- Kier Group PLC

- G4S Facilities Management UK Limited

- Sodexo Facilities Management Services

- Compass Group

- Equans

- VINCI Facilities Limited

- Aramark Facilities Services

- Andron Facilities Management

- CSM Facilities Management Group

- Orton Group

- Global Facilities.

- BGIS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.1.1 Current Occupancy Rates

- 4.1.2 Profitability Rates of Major FM Players

- 4.1.3 Workforce Indicators - Labor Participation

- 4.1.4 Facility Management Market Share (%), by Service Type

- 4.1.5 Facility Management Market Share (%), by Hard Services

- 4.1.6 Facility Management Market Share (%), by Soft Services

- 4.1.7 Urbanization and Population Growth in Major Metros

- 4.1.8 Sector Investment Priorities in United Kingdom's Infrastructure Pipeline

- 4.1.9 Regulatory Drivers Specific to Labour and Safety Standards

- 4.2 Market Drivers

- 4.2.1 Rapid Commercial Real Estate Expansion

- 4.2.2 Technology Integration (IoT, AI, Automation)

- 4.2.3 Increasing Outsourcing Trend

- 4.2.4 Rising Focus on Workplace Experience and Employee Well-being

- 4.2.5 Stringent Energy-Efficiency and Net-Zero Regulations

- 4.2.6 Rise of Flexible Workspaces Requiring Agile FM Contracts

- 4.3 Market Restraints

- 4.3.1 Labor Shortages and Skill Gaps

- 4.3.2 Margin Pressure from Rising Operational Costs

- 4.3.3 Fragmented Supplier Ecosystem Hindering Service Standardization

- 4.3.4 Data-Security Concerns in Smart Building Systems

- 4.4 Value Chain Analysis

- 4.5 PESTEL Analysis

- 4.6 Regulatory and Legislative Framework for Market Entrants

- 4.7 Impact of Macroeconomic Indicators on FM Demand

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Services

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment and Funding Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Services

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard FM Services

- 5.1.2 Soft Services

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft FM Services

- 5.1.1 Hard Services

- 5.2 By Offering Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.2.2.1 Single FM

- 5.2.2.2 Bundled FM

- 5.2.2.3 Integrated FM

- 5.3 By End-user Industry

- 5.3.1 Commercial (IT and Telecom, Retail and Warehouses, etc.)

- 5.3.2 Hospitality (Hotels, Eateries, Large-scale Restaurants)

- 5.3.3 Institutional and Public Infrastructure (Govt, Education, Transportation)

- 5.3.4 Healthcare (Public and Private Facilities)

- 5.3.5 Industrial and Process (Manufacturing, Energy, Mining)

- 5.3.6 Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Partnerships

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ISS UK

- 6.4.2 Mitie Group PLC

- 6.4.3 Serco Group PLC

- 6.4.4 Kier Group PLC

- 6.4.5 G4S Facilities Management UK Limited

- 6.4.6 Sodexo Facilities Management Services

- 6.4.7 Compass Group

- 6.4.8 Equans

- 6.4.9 VINCI Facilities Limited

- 6.4.10 Aramark Facilities Services

- 6.4.11 Andron Facilities Management

- 6.4.12 CSM Facilities Management Group

- 6.4.13 Orton Group

- 6.4.14 Global Facilities.

- 6.4.15 BGIS

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Technology-led Integrated FM (IoT, BMS, AI-based Predictive Maintenance)

- 7.3 ESG-compliant FM Solutions Demand

- 7.4 Future Service-Model Shifts (Outcome-based Contracts)