PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851850

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851850

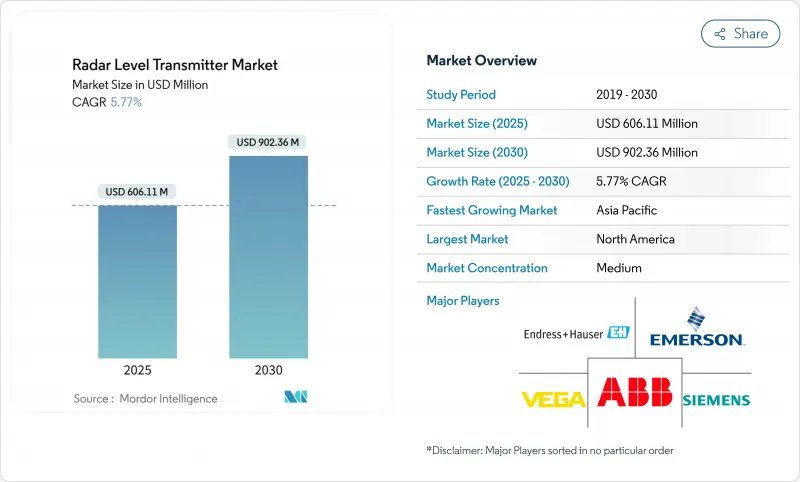

Radar Level Transmitter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The radar level transmitter market is valued at USD 606.11 million in 2025 and is forecast to reach USD 902.36 million by 2030, advancing at a 5.77% CAGR.

Demand is anchored in industrial automation programs that require precise level monitoring to meet stricter environmental and safety mandates. Technology migration from ultrasonic to 80 GHz radar in European oil terminals, growing desalination capital spending across the Gulf states, and retrofit activity in aging North-American water utilities are pivotal growth vectors. Manufacturers are also benefiting from coal-to-chemicals projects in China, where complex interface measurements favor guided-wave radar, and from a steady move toward wireless, Industrial-Internet-ready sensors that support predictive maintenance. Competitive differentiation hinges on antenna miniaturization, advanced signal processing for foam or low-dielectric media, and service ecosystems that shorten commissioning times.

Global Radar Level Transmitter Market Trends and Insights

80 GHz radar replacing ultrasonic sensors in EU oil-terminal overfill protection

European regulations mandate advanced overfill protection, prompting operators to replace ultrasonic gauges with 80 GHz radar. Narrow beam angles concentrate microwave energy, delivering reliable measurements even through vapors and temperature swings, while compact antenna designs simplify retrofits in tanks fitted with floating roofs. Coupled with maintenance-free operation, the technology ensures compliance and lowers lifecycle cost.

Desalination CAPEX boom in GCC boosting radar installations

Saudi Arabia, the UAE, and Kuwait collectively account for half of global desalination capacity. New multi-stage flash and reverse-osmosis plants demand non-contact radar that withstands corrosive, high-salinity brines. Integration with digital control systems improves energy efficiency and water recovery, embedding radar as a standard specification in regional EPC contracts.

Signal loss in foam-intense reactors

Thick foam layers attenuate microwaves, causing spurious echoes that disrupt level control in ethoxylation or fermentation vessels. Enhanced signal processing and hybrid radar-capacitance probes mitigate, but physics still limits radar penetration in extreme foaming.

Other drivers and restraints analyzed in the detailed report include:

- China coal-to-chemicals interface measurement demand

- Retrofit Wave of IIoT-Ready Instruments in Ageing US Water Plants

- Shortage of certified radar technicians in ASEAN

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Non-contact sensors captured 65% of 2024 revenue, reflecting preference for maintenance-free operation in corrosive or high-temperature duties. The sub-segment will expand at 6.8% CAGR, reinforced by frequency-modulated continuous-wave (FMCW) platforms that sharpen signal-to-noise ratios. Guided-wave radar retains a niche where interface detection or heavy foam is prevalent. Compact 80 GHz antennas now retrofit vessels once limited to ultrasonic probes, enlarging addressable demand for the radar level transmitter market.

Digital advances such as Bluetooth commissioning and in-sensor diagnostics simplify compliance audits, enhancing the radar level transmitter industry's value proposition. Suppliers position self-monitoring features as a hedge against workforce shortages, elevating radar to a core node in enterprise asset-performance platforms.

K-band (24-26 GHz) still held 38% of 2024 shipments, appreciated for cost-effectiveness and broad approvals. Yet W-band (76-81 GHz and 120 GHz) sensors show 7.4% CAGR due to sub-3° beam angles that ignore agitator blades and narrow nozzles, delivering reliable readings in 40-m columns or slender brew kettles. Certification agencies in the United States, EU, and China cleared W-band for process use, driving scale economies that are eroding historic price premiums. As component costs fall, W-band penetration will remake competitive positioning in the radar level transmitter market.

The Radar Level Transmitter Market Report is Segmented by Technology (Contact System, Non-Contact System), Frequency Range (C and X Band, K Band, W Band), Application (Liquids/Interfaces, Solids), End-User Industry (Oil and Gas, Chemicals, Water, Power Generation, Pharmaceuticals and Biotechnology, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 32% revenue share stems from mature oil, chemical, and food industries, coupled with federal grants that incentivize digital upgrades in water infrastructure. Utilities leverage cloud-connected radar to cut field visits, while craft brewers adopt hygienic models that withstand aggressive clean-in-place cycles.

Asia-Pacific is the growth engine at 7.5% CAGR, led by Chinese coal-to-chemicals plants and Indian smart-city wastewater projects. Australian miners specify foam-tolerant 80 GHz units for tailings management, and Southeast Asian palm-oil refineries demand guided-wave models that handle sticky media.

Europe maintains steady momentum, driven by process optimization in Germany's chemical parks and methane-emission rules that mandate tighter tank-gauging accuracy across the continent. Scandinavian utilities procure low-power radar sensors suited to cold-climate reservoirs, emphasizing sustainability and reduced servicing trips.

The Middle East's desalination boom anchors long-term demand, whereas Latin America's copper and lithium expansions support solids-focused radar deployments. Africa's cement and beverage sectors adopt cost-optimized 24 GHz units as electrification spreads.

- Emerson Electric Co.

- Siemens AG

- Endress+Hauser Group

- ABB Ltd.

- Honeywell International Inc.

- VEGA Grieshaber KG

- KROHNE Messtechnik

- Yokogawa Electric Corp.

- AMETEK Inc.

- Magnetrol International (AMETEK)

- Schneider Electric SE

- Pepperl+Fuchs SE

- Automation Products Group Inc.

- Nivelco Process Control Corp.

- Matsushima Measure Tech Co. Ltd.

- Hawk Measurement Systems

- Bindicator (Venture Measurement)

- Drexelbrook (Ametek)

- FEEJOY Technology

- SOR Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 80 GHz Radar Replacing Ultrasonic Sensors in EU Oil-Terminal Overfill Protection

- 4.2.2 Desalination CAPEX Boom in GCC Boosting Radar Installations

- 4.2.3 China Coal-to-Chemicals Interface Measurement Demand

- 4.2.4 Retrofit Wave of IIoT-Ready Instruments in Ageing US Water Plants

- 4.2.5 Hygienic Non-Contact Radar Adoption by North-American Craft Breweries

- 4.2.6 Foam-Tolerant Radar for Tailings Dams in Australian Mining

- 4.3 Market Restraints

- 4.3.1 Signal Loss in Foam-Intense Reactors

- 4.3.2 Shortage of Certified Radar Technicians in ASEAN

- 4.3.3 High Up-Front Cost vs Ultrasonic on OEM Skids

- 4.3.4 Low-Dielectric Powders Causing Accuracy Concerns

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Contact System (Guided Wave Radar)

- 5.1.2 Non-Contact System (Free-Space Radar)

- 5.1.2.1 FMCW Radar

- 5.1.2.2 Pulsed Radar

- 5.2 By Frequency Range

- 5.2.1 C and X Band (6-12 GHz)

- 5.2.2 K Band (24-26 GHz)

- 5.2.3 W Band (76-81 and 120 GHz)

- 5.3 By Application

- 5.3.1 Liquids, Slurries and Interfaces

- 5.3.2 Solids (Bulk Powders and Granulates)

- 5.4 By End-user Industry

- 5.4.1 Oil and Gas

- 5.4.2 Chemicals and Petrochemicals

- 5.4.3 Water and Wastewater

- 5.4.4 Food and Beverages

- 5.4.5 Power Generation

- 5.4.6 Pharmaceuticals and Biotechnology

- 5.4.7 Metals and Mining

- 5.4.8 Marine and Shipbuilding

- 5.4.9 Other Industries (Pulp and Paper, Cement)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (MandA, Partnerships, New Products)

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Emerson Electric Co.

- 6.4.2 Siemens AG

- 6.4.3 Endress+Hauser Group

- 6.4.4 ABB Ltd.

- 6.4.5 Honeywell International Inc.

- 6.4.6 VEGA Grieshaber KG

- 6.4.7 KROHNE Messtechnik

- 6.4.8 Yokogawa Electric Corp.

- 6.4.9 AMETEK Inc.

- 6.4.10 Magnetrol International (AMETEK)

- 6.4.11 Schneider Electric SE

- 6.4.12 Pepperl+Fuchs SE

- 6.4.13 Automation Products Group Inc.

- 6.4.14 Nivelco Process Control Corp.

- 6.4.15 Matsushima Measure Tech Co. Ltd.

- 6.4.16 Hawk Measurement Systems

- 6.4.17 Bindicator (Venture Measurement)

- 6.4.18 Drexelbrook (Ametek)

- 6.4.19 FEEJOY Technology

- 6.4.20 SOR Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment