PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851865

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851865

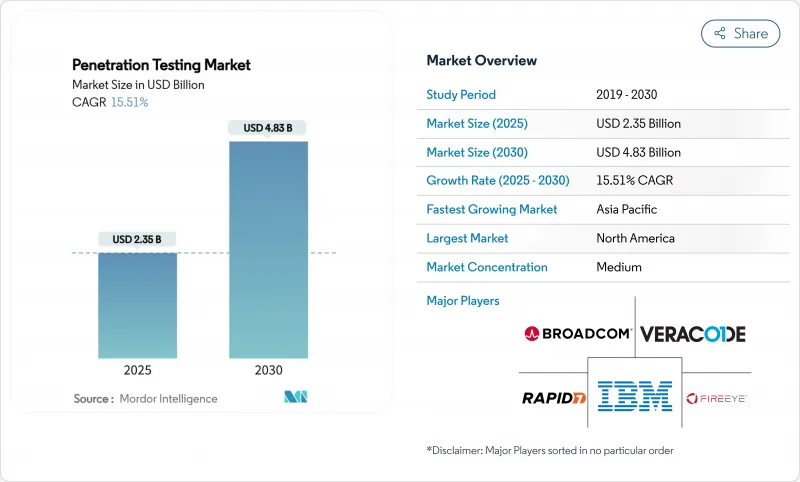

Penetration Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The penetration testing market was valued at USD 2.35 billion in 2025 and is forecast to reach USD 4.83 billion in 2030, advancing at a 15.51% CAGR over 2025-2030.

Growth is propelled by sharper cyber-attack tactics, tighter privacy statutes, and rising cyber-insurance prerequisites that make independent security validation a board-level priority. New mandates under HIPAA, PCI DSS 4.0, and the Digital Operational Resilience Act are expanding the addressable spend as organizations must prove continuous control efficacy to regulators. Investment is shifting toward AI-enabled, API-driven test automation that cuts cycle time and broadens access for resource-constrained teams. Cloud adoption, embedded DevSecOps practices, and aggressive digitalization across banking, healthcare, and manufacturing create fresh revenue pools for providers willing to bundle consulting, tooling, and managed services. The competitive field is responding through platform acquisitions, talent roll-ups, and venture funding aimed at scaling global delivery and shortening time-to-value.

Global Penetration Testing Market Trends and Insights

Government Mandates and Industry-Specific Regulations

Revised frameworks such as FedRAMP's 2024 guidance and forthcoming HIPAA updates now specify annual or even continuous penetration tests, obliging covered entities and cloud vendors to hard-wire offensive assessments into security programs. PCI DSS 4.0 alone introduces 63 new control statements that explicitly reference deeper, scenario-based testing for cardholder data environments. Financial entities in the EU face similar scrutiny under DORA, guaranteeing a multi-year tailwind for specialist service providers.

AI-Driven Automated Testing Platforms Lower Cost and Frequency

Machine-learning engines embedded in modern testing platforms detect exploitable paths with near-real-time accuracy, trimming manual effort and widening market reach to cash-strapped SMEs. Early adopters report cycle-time reductions of up to 70% and subscription entry points under USD 100 per month, converting one-off engagements into recurring revenue streams for vendors.

Lack of Awareness Among SMEs

Budget limits and staffing shortages continue to dampen penetration testing uptake among smaller firms despite evidence of rising breach exposure. Education campaigns, bundled insurance discounts, and lower-priced automated suites are gradually narrowing the gap, but the segment still lags larger enterprises on maturity metrics.

Other drivers and restraints analyzed in the detailed report include:

- DevSecOps Pipelines Require Continuous Pen-Testing Integration

- Cyber-Insurance Underwriting Now Demands Third-Party Tests

- Shortage and High Cost of Skilled Testers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Web application projects generated 36% penetration testing market share in 2024 as companies fortified e-commerce portals and SaaS workloads. Demand stays stable because every customer-facing service stack now includes browser-based interfaces needing recurring exploit validation. Mobile application testing, however, is scaling at a 19.23% CAGR, reflecting the migration of banking and retail interactions to Android and iOS channels.

Intensifying scrutiny from app-store gatekeepers and financial supervisors forces developers to integrate mobile-specific threat modeling, session management checks, and runtime protections. Cloud and API-centric architectures further enlarge the attack surface, pushing security teams toward unified platforms that scan web, mobile, and micro-services in a single engagement cadence.

On-premise programs retained 61% of 2024 revenues, a testament to data-residency mandates and comfort with in-house test orchestration. Yet cloud-based subscriptions are growing 20.27% annually, buoyed by the ability to spin up agents instantly and stream findings back into DevSecOps dashboards.

Providers are adding zero-trust connectors, anonymized data chambers, and regionally segregated workloads to reassure highly regulated buyers. Hybrid delivery-local test harnesses coupled with cloud analytics-emerges as the transitional state for firms balancing sovereignty with efficiency.

The Penetration Testing Market Report is Segmented by Testing Type (Network Penetration Testing, and More), Deployment Mode (On-Premise, and Cloud), Organization Size (Large Enterprises, and SMEs), Service Delivery Mode (In-House Testing Teams, and Third-Party Managed Services), End-User Industry (Government and Defense, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 39% of 2024 revenues, supported by federal directives such as FedRAMP test guidance for cloud vendors and IRS production-environment rules. Healthcare overhaul proposals alone could inject USD 4.6 billion in fresh security outlays once finalized. An advanced vendor ecosystem, mature cyber-insurance market, and venture funding concentration reinforce regional leadership.

Asia-Pacific is the fastest-growing arena, charting a 17.04% CAGR as insurers premium-price untested environments and governments formalize critical-infrastructure audit schedules. Japan's Cyber Colosseo training pipeline, China's push for self-reliant security stacks, and India's fintech surge combine to elevate test frequency requirements. Tier-2 economies in ASEAN are also commissioning managed services to plug local talent gaps.

Europe records steady expansion under GDPR and the Digital Operational Resilience Act, compelling banks and insurers to validate controls across cross-border entities. Incumbent telecom and manufacturing clusters add depth by commissioning industrial-control and 5G-network test scopes. Eastern European firms, confronted with supply-chain spillovers from nearby conflicts, are moving quickly toward continuous engagement models.

- IBM Corporation

- Rapid7, Inc.

- Synopsys, Inc.

- Checkmarx Ltd.

- Acunetix Ltd. (Invicti Security)

- Broadcom Inc. (Symantec Corporation)

- FireEye Inc.

- Veracode, Inc.

- Qualys, Inc.

- Tenable Holdings, Inc.

- Palo Alto Networks, Inc. (Unit 42)

- Offensive Security, LLC

- Core Security (Fortra)

- Pentera Security Ltd.

- HackerOne, Inc.

- Trustwave Holdings, Inc.

- IOActive, Inc.

- NCC Group plc

- Cofense Inc.

- Bishop Fox, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising cybersecurity risks across sectors

- 4.2.2 Increasing demand for security assessments and compliance audits

- 4.2.3 Government mandates and industry-specific regulations

- 4.2.4 AI-driven automated testing platforms lower cost and frequency

- 4.2.5 DevSecOps pipelines require continuous pen-testing integration

- 4.2.6 Cyber-insurance underwriting now demands third-party pen tests

- 4.3 Market Restraints

- 4.3.1 Lack of awareness among SMEs

- 4.3.2 Shortage and high cost of skilled testers

- 4.3.3 Tool-sprawl and false-positive fatigue reduce ROI

- 4.3.4 Legal/liability concerns over active exploitation in some nations

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Assessment of Macro Economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Testing Type

- 5.1.1 Network Penetration Testing

- 5.1.2 Web Application Penetration Testing

- 5.1.3 Mobile Application Penetration Testing

- 5.1.4 Social Engineering Penetration Testing

- 5.1.5 Wireless Network Penetration Testing

- 5.1.6 Cloud Penetration Testing

- 5.1.7 Other Types

- 5.2 By Deployment Model

- 5.2.1 On-premise

- 5.2.2 Cloud-based

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By Service Delivery Mode

- 5.4.1 In-house Testing Teams

- 5.4.2 Third-party Managed Services

- 5.5 By End-user Industry

- 5.5.1 Government and Defense

- 5.5.2 Banking, Financial Services and Insurance (BFSI)

- 5.5.3 IT and Telecom

- 5.5.4 Healthcare and Life Sciences

- 5.5.5 Retail and E-Commerce

- 5.5.6 Manufacturing

- 5.5.7 Energy and Utilities

- 5.5.8 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 GCC

- 5.6.5.1.2 Turkey

- 5.6.5.1.3 Israel

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Funding

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Rapid7, Inc.

- 6.4.3 Synopsys, Inc.

- 6.4.4 Checkmarx Ltd.

- 6.4.5 Acunetix Ltd. (Invicti Security)

- 6.4.6 Broadcom Inc. (Symantec Corporation)

- 6.4.7 FireEye Inc.

- 6.4.8 Veracode, Inc.

- 6.4.9 Qualys, Inc.

- 6.4.10 Tenable Holdings, Inc.

- 6.4.11 Palo Alto Networks, Inc. (Unit 42)

- 6.4.12 Offensive Security, LLC

- 6.4.13 Core Security (Fortra)

- 6.4.14 Pentera Security Ltd.

- 6.4.15 HackerOne, Inc.

- 6.4.16 Trustwave Holdings, Inc.

- 6.4.17 IOActive, Inc.

- 6.4.18 NCC Group plc

- 6.4.19 Cofense Inc.

- 6.4.20 Bishop Fox, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment