PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910645

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910645

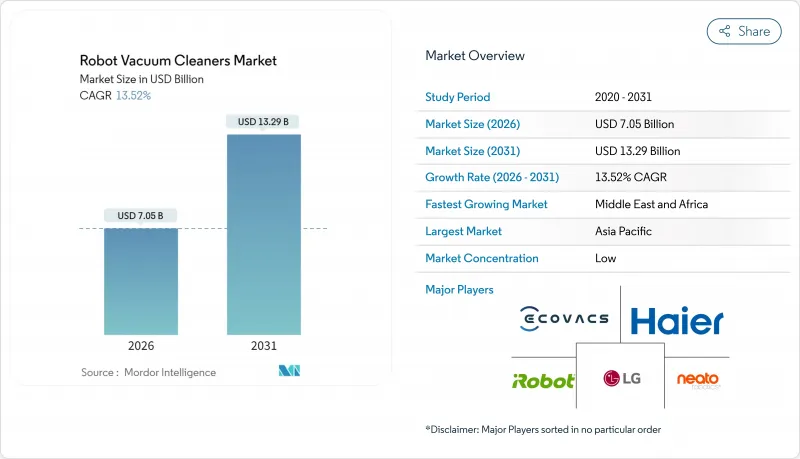

Robot Vacuum Cleaners - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Robotic vacuum cleaners market size in 2026 is estimated at USD 7.05 billion, growing from 2025 value of USD 6.21 billion with 2031 projections showing USD 13.29 billion, growing at 13.52% CAGR over 2026-2031.

Rising smart-home penetration, falling sensor and battery costs, and demographic shifts toward automated domestic care are the key forces behind this trajectory. Asia Pacific remains the pivotal growth engine as digitization programs spur infrastructure that supports always-connected appliances, while policy incentives in Japan and South Korea strengthen uptake in elderly-care settings. Component price deflation lets manufacturers embed LiDAR, AI navigation, and self-emptying docks in mid-range models, widening the consumer base. Competitive intensity is reshaped by Chinese vendors that leverage scale and rapid iteration to bring premium functionality to mainstream price tiers. Hospitality operators facing higher labor costs add an institutional demand layer that accelerates adoption across commercial real estate.

Global Robot Vacuum Cleaners Market Trends and Insights

Surging Adoption of Smart-Home Ecosystems in Asia

Voice-assistant compatibility is now a baseline requirement, and regional adoption rates exceed 10% in advanced economies. Brands localize features such as remote security monitoring and AI-driven room mapping to meet hygiene and safety preferences. Samsung and LG models tuned for domestic use illustrate how local incumbents defend share against Chinese challengers while aligning with national elderly-care programs.

Rapid Price Declines in Li-ion and Sensor Components

Volume manufacturing of LiDAR modules, cameras, and control ICs lowers production costs, pushing retail prices from USD 2,000-5,000 in 2024 toward USD 500-1,500 by 2030. Chinese vendors translate vertical integration into aggressive pricing, while incumbents respond by bundling premium navigation and self-cleaning docks in mid-tier lines. Lower barriers enhance penetration among first-time buyers and fuel upgrade cycles among existing owners.

Low Penetration of High-Suction Models in Deep-Pile Carpet Regions

Deep-pile carpets demand higher airflow and specialized brushes that raise cost and power consumption. Premium units rated at 20,000 Pa address the performance gap but remain unaffordable for price-sensitive households. Traditional uprights persist in these markets, limiting robotic uptake until high-performance features scale down in cost.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Hybrid Vacuum-Mop Models in Europe

- Hospitality Sector's Pivot to Autonomous Cleaning in Middle-East Luxury Hotels

- Battery-Safety Recalls Impacting Brand Trust in EU

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Floor vacuum units held a 78.35% share in 2025, anchoring the robotic vacuum cleaners market through proven efficacy across common floor types. Hybrid 2-in-1 systems, however, are advancing at a 16.6% CAGR as consumers seek single devices that vacuum and mop. ECOVACS' DEEBOT T30, with tangle-free rollers and heated mop pads, exemplifies the design philosophy that merges convenience with deeper cleaning.

Hybrid penetration improves especially in Europe where mixed wood-tile layouts prevail. Innovative models with edge-to-edge brush reach and auto-wash stations position the robotic vacuum cleaners market as a gateway to wider smart-home automation. Such versatility attracts upgrade buyers eager for devices that handle multiple chores without manual intervention.

Residential buyers still represent 90.25% of the robotic vacuum cleaners market size in 2025 due to mass-market pricing and app-based controls that cater to busy households. Commercial hospitality is the fastest-rising customer set, growing 14.95% annually as hotels mitigate labor shortages with 24/7 autonomous floor care. Units purpose-built for corridor geometry and larger debris hoppers underscore this shift.

Office and retail facilities gradually follow, deploying fleets managed from cloud dashboards that optimize routing and maintenance. The resulting data insights on traffic patterns and cleaning intensity evolve robots from single-function tools into integrated facility-management assets, deepening their value proposition.

Robotic Vacuum Cleaner Market Report is Segmented by Product Type (Floor Vacuum, Pool Vacuum, and More), End-User (Residential, Commercial), Battery Type (Lithium-Ion, Nickel-Metal Hydride), Connectivity (Smart-Connected, Non-Connected), Price Range (Below USD 200, and More), Distribution Channel (Online Marketplaces, Brand E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific anchored 40.70% of global demand in 2025, leveraging domestic manufacturing ecosystems that compress lead times and costs. Chinese producers refine designs at home before exporting, while South Korean incumbents differentiate on AI features tailored to safety-conscious users. Government grants for elder-care robots translate into sustained volume, embedding robots into daily routines.

The Middle East is the fastest-growing region at 18.3% CAGR through 2031 as luxury hotels operationalize 24/7 cleaning to offset staffing gaps. Dust-laden climates elevate demand for high-capacity filtration, and premium property owners adopt robotic fleets both for performance and brand differentiation.

North America and Europe exhibit high household awareness yet confront distinct regulatory dynamics. EU battery and AI legislation heightens compliance costs but reinforces consumer trust in brands that meet stringent safety thresholds. In Latin America, tariffs of 20-60% on imported appliances incentivize regional assembly strategies that could shift value-chain investment over the forecast window.

- iRobot Corporation

- Ecovacs Robotics Co. Ltd

- Roborock Technology Co. Ltd

- SharkNinja Operating LLC

- Dyson Ltd

- LG Electronics Inc.

- Samsung Electronics Co. Ltd

- Electrolux AB

- Panasonic Corporation

- Haier Group Corporation

- Cecotec Innovaciones SL

- Neato Robotics Inc.

- ILIFE Innovation Ltd

- Anker Innovations (Eufy)

- Vorwerk SE and Co. KG (Kobold)

- Miele and Cie KG

- Bissell Homecare Inc.

- HOBOT Technology Inc.

- Proscenic Technology Co. Ltd

- Hitachi Ltd

- Haeir Group Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Adoption of Smart-Home Ecosystems in Asia

- 4.2.2 Rapid Price Declines in Li-ion and Sensor Components

- 4.2.3 Growing Demand for Hybrid Vacuum-Mop Models in Europe

- 4.2.4 Hospitality Sector's Pivot to Autonomous Cleaning in Middle-East Luxury Hotels

- 4.2.5 Government Incentives for Elderly-Care Tech in Japan and South Korea

- 4.3 Market Restraints

- 4.3.1 Low Penetration of High-Suction Models in Deep-Pile Carpet Regions (US Midwest)

- 4.3.2 Battery-Safety Recalls Impacting Brand Trust in EU

- 4.3.3 High Import Tariffs on Smart Appliances in South America

- 4.3.4 Inter-brand Software Interoperability Gaps Limiting Ecosystem Stickiness

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment and Funding Landscape

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Floor Vacuum

- 5.1.2 Pool Vacuum

- 5.1.3 Window Cleaning Robot

- 5.1.4 Hybrid 2-in-1 Vacuum-Mop

- 5.2 By End-User

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.3 By Battery Type

- 5.3.1 Lithium-ion

- 5.3.2 Nickel-Metal Hydride

- 5.4 By Connectivity

- 5.4.1 Smart-Connected (Wi-Fi / Voice-Assist)

- 5.4.2 Non-Connected

- 5.5 By Price Range

- 5.5.1 Below USD 200

- 5.5.2 USD 200 - 499

- 5.5.3 USD 500 and Above

- 5.6 By Distribution Channel

- 5.6.1 Online Marketplaces

- 5.6.2 Brand E-commerce

- 5.6.3 Specialty Stores

- 5.6.4 Mass Retailers and Hypermarkets

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Nordics

- 5.7.4 Middle East and Africa

- 5.7.4.1 Saudi Arabia

- 5.7.4.2 United Arab Emirates

- 5.7.4.3 South Africa

- 5.7.4.4 Rest of Middle East and Africa

- 5.7.5 Asia-Pacific

- 5.7.5.1 China

- 5.7.5.2 Japan

- 5.7.5.3 South Korea

- 5.7.5.4 Rest of Asia-Pacific

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 iRobot Corporation

- 6.4.2 Ecovacs Robotics Co. Ltd

- 6.4.3 Roborock Technology Co. Ltd

- 6.4.4 SharkNinja Operating LLC

- 6.4.5 Dyson Ltd

- 6.4.6 LG Electronics Inc.

- 6.4.7 Samsung Electronics Co. Ltd

- 6.4.8 Electrolux AB

- 6.4.9 Panasonic Corporation

- 6.4.10 Haier Group Corporation

- 6.4.11 Cecotec Innovaciones SL

- 6.4.12 Neato Robotics Inc.

- 6.4.13 ILIFE Innovation Ltd

- 6.4.14 Anker Innovations (Eufy)

- 6.4.15 Vorwerk SE and Co. KG (Kobold)

- 6.4.16 Miele and Cie KG

- 6.4.17 Bissell Homecare Inc.

- 6.4.18 HOBOT Technology Inc.

- 6.4.19 Proscenic Technology Co. Ltd

- 6.4.20 Hitachi Ltd

- 6.4.21 Haeir Group Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment