PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851884

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851884

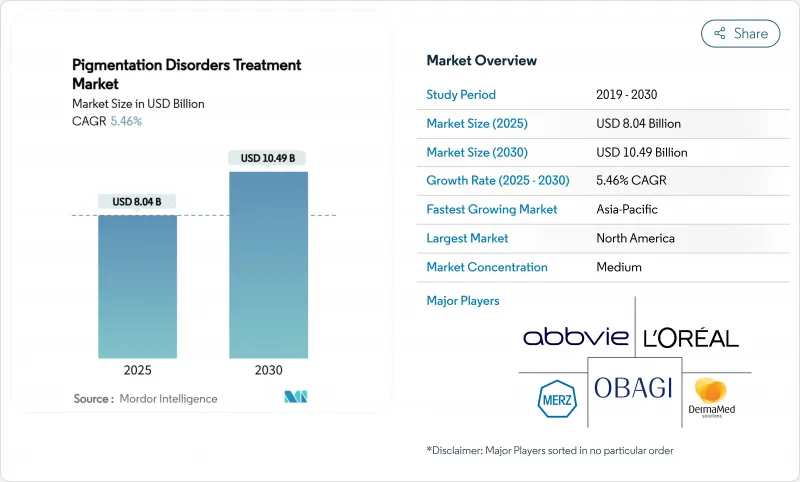

Pigmentation Disorders Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The pigmentation disorders treatment market size stands at USD 8.04 billion in 2025 and is forecast to reach USD 10.49 billion by 2030, advancing at a 5.46% CAGR over the period.

Sustained growth is powered by rising disease prevalence, regulatory momentum behind topical and oral JAK inhibitors, increasing dermatology spending, and AI-driven diagnostic accuracy improvements. Pharmaceutical pipelines are focusing on immune-modulating pathways, while device makers refine laser safety profiles for darker skin tones. Convergence between medical dermatology and aesthetic care is widening the addressable base, and stronger social-media influence in Asia is accelerating patient awareness and therapeutic demand. Strategic acquisitions and portfolio diversification underscore a market moving toward precision medicine and omni-channel delivery models.

Global Pigmentation Disorders Treatment Market Trends and Insights

Rise in Prevalence of Pigmentation Disorders

Global cases are climbing due to demographic changes, urban pollution, and greater diagnostic vigilance. Vitiligo affects 28.5 million people worldwide, generating significant psychosocial burden among patients with darker skin tones who experience higher contrast between affected and unaffected areas. Post-inflammatory hyperpigmentation is increasingly common after acne, with complete clearance seldom achieved even after treatment.Melasma incidence remains high in sunny climates and among women of reproductive age, a trend amplified by UV exposure shifts related to climate change. These epidemiological patterns enlarge the patient pool seeking both preventive and therapeutic solutions across regions.

Growing Expenditure on Dermatological & Aesthetic Procedures

Spending on dermatology services is rising as consumers prioritize skin health and appearance. Procedures once deemed purely cosmetic now attract reimbursement when therapeutic benefit is demonstrated, encouraging clinics to integrate lasers, peels, and combination regimens. Medical spas broaden service menus, while hospital outpatient departments adopt advanced devices to meet demand. Availability of professional-grade home-use IPL units at roughly USD 1,200 is widening access, stimulating the pigmentation disorders treatment market.

High Out-of-Pocket Cost of Cosmetic Procedures

Many insurers classify pigmentation procedures as elective, leaving patients to shoulder costs that range from several hundred to several thousand dollars per session. Affordability issues delay treatment initiation and can lead to incomplete therapy cycles that blunt outcomes. The barrier is acute in emerging markets where disposable income lags demand for advanced aesthetic care, restraining the pigmentation disorders treatment industry's immediate uptake despite clear clinical need.

Other drivers and restraints analyzed in the detailed report include:

- R&D Pipeline Success of Topical JAK Inhibitors

- AI-Enabled Diagnostic Imaging Improving Treatment Outcomes

- Limited Reimbursement Coverage for Pigment Disorders

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vitiligo accounted for 33.56% of 2024 revenue, securing the largest share of the pigmentation disorders treatment market. The segment is growing at an 8.34% CAGR, reflecting breakthrough approvals such as topical ruxolitinib and phase 3 trials of oral JAK candidates. The pigmentation disorders treatment market size for vitiligo is anticipated to climb steadily to 2030 as regulatory agencies worldwide review similar formulations. Melasma maintains significant demand within high-UV regions, while post-inflammatory hyperpigmentation remains prevalent among acne patients with skin of color. Albinism, though numerically smaller, sustains consistent therapeutic needs for photoprotection and ocular support. Completion of Clinuvel's afamelanotide phase III trial may introduce systemic therapy that complements existing topical or phototherapy regimens.

Continued epidemiological surveillance shows pigmentary disorders intersect with psychosocial wellness, motivating health systems to assess quality-of-life indices in resource allocation. AI-driven diagnosis facilitates earlier vitiligo identification, enabling timely JAK inhibitor initiation before lesion expansion. Meanwhile, clinical researchers pursue biomarkers that forecast repigmentation likelihood, aiming to stratify patients and maximize therapeutic utility.

Laser and energy platforms captured 37.36% of 2024 revenue, retaining primacy through proven versatility across disorders. Still, biologics and JAK inhibitors are the fastest-growing class at 9.03% CAGR, heralding a precision-medicine era. The pigmentation disorders treatment market size for biologics is projected to widen as oral inhibitors secure wider indications and reimbursement frameworks adapt. Conventional topical depigmenting agents persist as foundational therapy due to ease of use and affordability. Chemical peels and dermabrasion support combination strategies that blend cosmetic refinement with clinical clearance.

Industry advances emphasize wavelength optimization and integrated cooling to mitigate PIH. Professional societies report that 1726 nm laser platforms enhance safety and permit uniform application across all Fitzpatrick skin types. Device makers also release multifunction consoles tailored to treat vascular lesions, acne, and pigmentation within one suite, raising capital-efficiency for clinics.

The Pigmentation Disorders Treatment Market Report is Segmented by Type of Disorder (Albinism, Vitiligo, and More), Treatment Type (Topical Agents, Dermabrasion, and More), Product Category (Pharmaceuticals, Energy-Based Devices and More), End User (Dermatology Clinics, Hospital Out-Patient Departments and More), and Geography (North America, Europe and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained the leading 37.13% share of the pigmentation disorders treatment market in 2024, aided by advanced insurance coverage for novel agents and broad clinician familiarity with laser protocols. Favorable reimbursement for ruxolitinib cream and ongoing phase 3 trials for oral inhibitors underpin demand momentum. High awareness among skin-of-color communities also propels service uptake, though coverage disparities persist.

Europe follows with stable growth as national health systems integrate targeted therapies alongside established topical standards. The region's stringent device regulations encourage safety-focused innovation, reinforcing clinician trust in energy platforms. Public-funded phototherapy services remain widely accessible, creating balanced modality usage.

Asia-Pacific is the fastest-growing region at a 7.83% CAGR. Rising disposable income, strong social-media beauty influence, and deep cultural emphasis on even skin tone are catalyzing procedure volume in China, Japan, South Korea, and India. The pigmentation disorders treatment market size in Asia is set to close the gap with North America as e-commerce and medical-tourism channels proliferate. Regulatory harmonization across ASEAN countries may further streamline cross-border device distribution.

Latin America and the Middle East & Africa collectively represent an emergent frontier. Urbanization, improving dermatology infrastructure, and local manufacturing of cosmeceuticals seed steady uptake, though economic volatility and insurance gaps temper near-term scale. Government-led public-health programs to address albinism and vitiligo stigma may indirectly support therapy adoption.

- Abbvie

- L'Oreal Group

- Galderma

- Pfizer

- Incyte

- Pierre Fabre

- Candela Medical

- Merz Pharma

- Bayer

- Obagi Cosmeceuticals

- Sun Pharmaceuticals Industries

- SkinCeuticals

- Clinuvel Pharmaceuticals

- Fosun Pharma

- Cynosure

- Vital Esthetique

- DermaMed Solutions

- Epionce

- InMode (Invasix)

- Candela Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise In Prevalence Of Pigmentation Disorders

- 4.2.2 Growing Expenditure On Dermatological & Aesthetic Procedures

- 4.2.3 R&D Pipeline Success Of Topical JAK-Inhibitors

- 4.2.4 Social-Media-Driven Demand For Even-Tone Skin In Emerging Asia

- 4.2.5 AI-Enabled Diagnostic Imaging Improving Treatment Outcomes

- 4.2.6 Pharma-Aesthetic Cross-Over Business Models Unlocking Revenue

- 4.3 Market Restraints

- 4.3.1 High Out-Of-Pocket Cost Of Cosmetic Procedures

- 4.3.2 Limited Reimbursement Coverage For Pigment Disorders

- 4.3.3 Laser-Induced PIH Risk In Darker Skin Types

- 4.3.4 Supply-Chain Dependence On Chinese Hydroquinone Feedstocks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Type of Disorder

- 5.1.1 Albinism

- 5.1.2 Vitiligo

- 5.1.3 Melasma

- 5.1.4 Post-Inflammatory Hyperpigmentation (PIH)

- 5.1.5 Other Disorders

- 5.2 By Treatment Type

- 5.2.1 Topical Agents

- 5.2.2 Dermabrasion

- 5.2.3 Chemical Peels

- 5.2.4 Laser / Energy-based Therapies

- 5.2.5 Phototherapy

- 5.2.6 Emerging Biologics & JAK-Inhibitors

- 5.3 By Product Category

- 5.3.1 Pharmaceuticals

- 5.3.2 Energy-based Devices

- 5.3.3 Cosmeceuticals & Adjunctive Skin-care

- 5.4 By End User

- 5.4.1 Dermatology Clinics

- 5.4.2 Hospital Out-patient Departments

- 5.4.3 Medical Spas & Aesthetic Centers

- 5.4.4 Home-use / e-commerce Customers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 AbbVie

- 6.3.2 L'Oreal Group

- 6.3.3 Galderma

- 6.3.4 Pfizer

- 6.3.5 Incyte

- 6.3.6 Pierre Fabre

- 6.3.7 Candela Medical

- 6.3.8 Merz Pharma

- 6.3.9 Bayer AG

- 6.3.10 Obagi Cosmeceuticals

- 6.3.11 Sun Pharmaceutical Industries

- 6.3.12 SkinCeuticals

- 6.3.13 Clinuvel Pharmaceuticals

- 6.3.14 Fosun Pharma

- 6.3.15 Cynosure

- 6.3.16 Vital Esthetique

- 6.3.17 DermaMed Solutions

- 6.3.18 Epionce

- 6.3.19 InMode (Invasix)

- 6.3.20 Syneron Candela

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment