PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851896

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851896

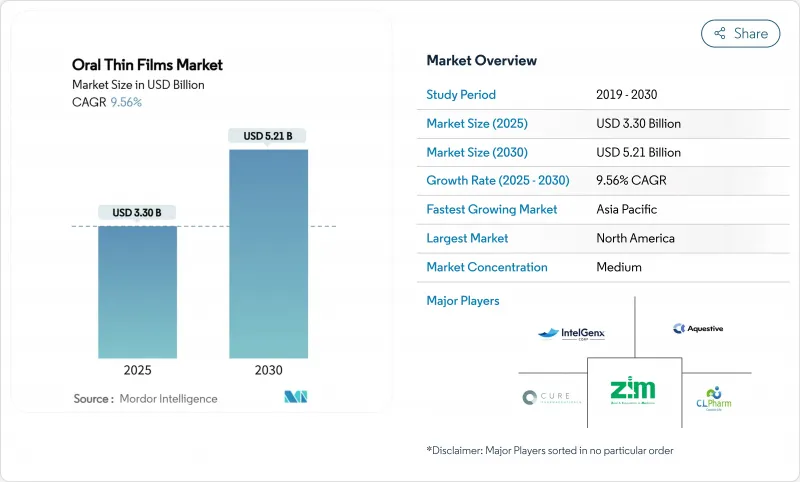

Oral Thin Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The oral thin films market size stands at USD 3.30 billion in 2025 and is forecast to reach USD 5.21 billion by 2030, reflecting a 9.56% CAGR over the period.

Demand accelerates as pharmaceutical developers prioritize patient-centric formats that bypass swallowing difficulties, avoid first-pass hepatic metabolism, and deliver rapid therapeutic onset. Population aging, higher chronic disease prevalence, and the need for pediatric-friendly medicines all reinforce a structural shift toward thin-film delivery. Technology improvements in polymer science, moisture barrier coatings, and continuous manufacturing add further momentum by lowering unit costs and widening the range of compatible active pharmaceutical ingredients. Competitive intensity grows as both branded innovators and generic manufacturers employ 505(b)(2) reformulation pathways to repurpose existing molecules, expanding the oral thin films market into indications once dominated by tablets and capsules.

Global Oral Thin Films Market Trends and Insights

Rising Prevalence of Chronic Diseases

Chronic non-communicable illnesses heighten the clinical urgency for dosage forms that improve adherence in patients with swallowing difficulties. Dysphagia affects 25% of adults older than 50 and up to 50% of nursing-home residents, and those patients experience longer inpatient stays and higher treatment costs. Sublingual buprenorphine films have become the preferred formulation in opioid use disorder programs because they reduce diversion risk and simplify directly observed therapy, reinforcing the oral thin films market expansion in addiction care. Clinicians also favor film products in hypertension and diabetes, where daily dosing regimens require steady compliance. Together, these disease trends supply a consistent patient base that shields the oral thin films market from economic slowdowns.

Growing Preference for Patient-Friendly Drug Delivery

An evidence base linking palatability and adherence now guides formulation design in pediatric and geriatric pharmacotherapy. A systematic review of 225 pediatric studies confirmed taste as a top barrier to completion of antibiotic and anticonvulsant regimens. Dissolvable films overcome this barrier by embedding flavor-masking excipients, leading to higher completion rates in head-to-head trials against liquids. Regulators also recognize the value proposition: FDA clearance of the dissolvable oral contraceptive Femlyv in July 2024 highlighted benefits in user convenience and dose accuracy. As prescribers increasingly factor ease of use into therapy selection, the oral thin films market captures prescriptions that once defaulted to tablets.

Limited Active Pharmaceutical Ingredient Loading Capacity

Thin films typically accommodate no more than 30% drug by weight before mechanical integrity fails, capping single-strip payloads around 30 mg in commercial practice. High-dosage therapies such as non-steroidal anti-inflammatory drugs must resort to multiple-strip administration schedules, negating some convenience benefits. Research into multilayer designs shows promise yet still confronts dissolution-time trade-offs. Until material science pushes that ceiling higher, the oral thin films market will focus on potent actives where lower milligram doses suffice.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Geriatric and Pediatric Populations

- Accelerated 505(b)(2) Reformulation Strategies

- High Regulatory and Quality Assurance Barriers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sublingual films accounted for 55.34% of oral thin films market share in 2024, reflecting entrenched physician familiarity in opioid addiction therapy and emergency seizure management. The format ensures rapid transmucosal uptake, delivering therapeutic plasma concentrations within minutes. Competitive pipelines remain active, with at least six new sublingual candidates in late-stage studies targeting anaphylaxis, hypotension, and migraine.

Buccal films, forecast to advance at an 11.45% CAGR, harness mucoadhesive polymers that prolong residence time against the cheek and slow payload release. This kinetic profile attracts hormone-replacement and chronic pain developers seeking once-daily dosing. 3-D printing further individualizes buccal thickness and drug load, enabling dose-titration without new stability studies. Over the outlook period, investors expect smaller yet faster-growing buccal lines to chip away at the dominant but maturing sublingual base.

Opioid dependence retained 39.65% of the oral thin films market size in 2024 and gains policy support under expanded medication-assisted treatment mandates in North America. Mandatory insurance coverage guarantees high prescription volumes, and thin-film packaging deters diversion through unit-dose blisters.

Migraine programs achieve a 12.21% CAGR, stimulated by RizaFilm's 2023 US approval that set a regulatory precedent for future triptan films. The format addresses patients who experience nausea and risk vomiting tablets during acute attacks. As additional molecules such as lasmiditan migrate to film, neurologists foresee wider adoption. Nausea-and-vomiting as well as schizophrenia segments also benefit, but their combined growth trails migraine's surge.

The Oral Thin Films Market Report is Segmented by Product (Sublingual Films, Buccal Films, and More), Disease Indication (Opioid Dependence, and More), Distribution Channel (Hospital Pharmacies, and More), Technology (Solvent-Casting, Hot-Melt Extrusion, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 41.67% of oral thin films market share in 2024. Robust reimbursement, clinician education, and clear FDA guidance accelerate uptake across pain, addiction, and pediatric allergy care. The regional pipeline includes eight NDA submissions under review as of July 2025, indicating sustained product flow. Retail pricing remains premium in the United States, underpinned by patent protection and limited generic competition.

Asia-Pacific is forecast to expand at 10.45% CAGR through 2030, propelled by contract manufacturing clusters in India and regulatory alignment efforts in the ASEAN Pharmaceutical Harmonization Scheme. Chinese producers invest in solvent-casting capacity, seeking WHO prequalification for export-oriented buprenorphine films. Rising middle-class incomes heighten acceptance of patient-friendly dosage forms, while domestic e-pharmacy platforms solve rural access gaps. Favorable cost structures position the region as both a supply base and a fast-growing demand center within the global oral thin films market.

Europe maintains steady volume under single-payer systems that scrutinize cost per quality-adjusted life-year. The European Medicines Agency's December 2024 approval of buprenorphine Neuraxpharm film underscores regulatory continuity despite Brexit. Country-level price controls spur reference-pricing erosion but also promote generics. In response, innovators pivot toward 3-D printed personalized therapies to secure differentiation. Tele-pharmacy directives embedded in the EU Pharmaceutical Strategy support cross-border mail order, likely nudging the online share upward over time.

- Aquestive Therapeutics

- Intelgenx

- LTS Lohmann Therapie-Systeme

- Viatris

- NAL Pharma

- ZIM Laboratories Ltd.

- Sunovion Pharmaceuticals

- CURE Pharmaceutical

- C.L. Pharm

- Indivior

- BioDelivery Sciences International

- Rapid Dose Therapeutics

- AdhexPharma

- Catalent

- Tapemark

- IBSA Group

- Dr.Thins

- DK Livkon Healthcare

- NutraStrips

- Pharmedica

- Nova Thin Film Pharmaceuticals

- Orcosa

- Labtec GmbH

- Aavishkar Oral Strips

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Chronic Diseases

- 4.2.2 Growing Preference for Patient-Friendly Drug Delivery

- 4.2.3 Increasing Geriatric and Pediatric Populations

- 4.2.4 Accelerated 505(B)(2) Reformulation Strategies

- 4.2.5 Expanding Cannabis and Nutraceutical Applications

- 4.2.6 Technological Advancements in Polymeric Film Engineering

- 4.3 Market Restraints

- 4.3.1 Limited Active Pharmaceutical Ingredient Loading Capacity

- 4.3.2 High Regulatory and Quality Assurance Barriers

- 4.3.3 Pricing Pressure from Generic Competition

- 4.3.4 Insufficient Good Manufacturing Practice Infrastructure

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat Of New Entrants

- 4.5.2 Bargaining Power Of Buyers

- 4.5.3 Bargaining Power Of Suppliers

- 4.5.4 Threat Of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Patent Landscape

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Sublingual Films

- 5.1.2 Buccal Films

- 5.1.3 Orodispersible Films

- 5.1.4 Fast-Dissolving Oral Films

- 5.2 By Disease Indication

- 5.2.1 Opioid Dependence

- 5.2.2 Nausea And Vomiting

- 5.2.3 Schizophrenia

- 5.2.4 Migraine

- 5.2.5 Pain Management

- 5.2.6 Others

- 5.3 By Distribution Channel

- 5.3.1 Hospital Pharmacies

- 5.3.2 Retail Pharmacies

- 5.3.3 Online Pharmacies

- 5.3.4 Other Distribution Channel

- 5.4 By Technology (Manufacturing Method)

- 5.4.1 Solvent-Casting

- 5.4.2 Hot-Melt Extrusion

- 5.4.3 3-D Printing

- 5.4.4 Other Technologies

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials As Available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Aquestive Therapeutics Inc.

- 6.3.2 IntelGenx Corp.

- 6.3.3 LTS Lohmann Therapie-Systeme AG

- 6.3.4 Viatris

- 6.3.5 NAL Pharma

- 6.3.6 ZIM Laboratories Ltd.

- 6.3.7 Sunovion Pharmaceuticals Inc.

- 6.3.8 CURE Pharmaceutical

- 6.3.9 C.L. Pharm

- 6.3.10 Indivior PLC

- 6.3.11 BioDelivery Sciences International

- 6.3.12 Rapid Dose Therapeutics

- 6.3.13 AdhexPharma

- 6.3.14 Catalent Inc.

- 6.3.15 Tapemark

- 6.3.16 IBSA Group

- 6.3.17 Dr.Thins

- 6.3.18 DK Livkon Healthcare

- 6.3.19 NutraStrips

- 6.3.20 Pharmedica

- 6.3.21 Nova Thin Film Pharmaceuticals

- 6.3.22 Orcosa

- 6.3.23 Labtec GmbH

- 6.3.24 Aavishkar Oral Strips

7 Market Opportunities & Future Outlook