PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851921

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851921

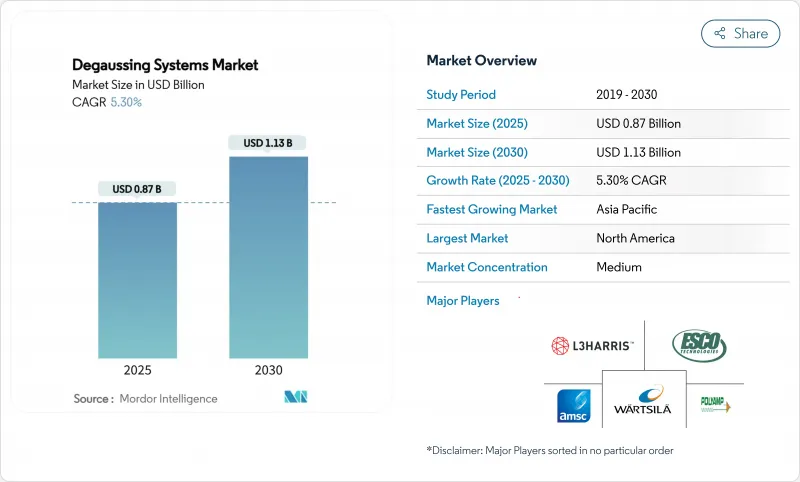

Degaussing Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The degaussing systems market size is estimated at USD 0.87 billion in 2025 and is forecasted to reach USD 1.13 billion by 2030, advancing at a 5.3% CAGR.

Rising naval expenditure, the growing sophistication of magnetic-influence sea mines, and the steady pace of fleet-life-extension programs underpin this expansion. North American destroyer and cruiser upgrades, European mine-hunter procurement, and expanding Asia-Pacific submarine fleets ensure a broad customer base for electromagnetic signature control. High-temperature superconducting (HTS) coils and software-defined control units foster technology refresh cycles, while artificial-intelligence (AI) algorithms push performance thresholds by moderating coil currents in real time. Retrofit demand governs contract activity because navies view signature management as a cost-effective path to stretching ship life without new-build outlays. Supply-chain pressure around HTS tape and rare-earth magnetic sensors tempers short-term growth, yet tier-one vendors with vertically integrated component lines mitigate most disruption.

Global Degaussing Systems Market Trends and Insights

Rising Naval Modernization Budgets Accelerating Investment in Degaussing Systems

Steady growth in defense allocations keeps multi-year ship-upgrade pipelines active. The US Navy's destroyer life-extension package earmarks signature-management retrofits as core electronic-warfare enhancements. Italy's mine-hunter program embeds low-magneto-acoustic technologies as a baseline fit. Similar procurement blueprints in the Philippines and Canada cement a long runway for the degaussing systems market.

Increased Deployment of Magnetic-Influence Sea Mines Driving Demand for Magnetic Signature Control

Modern mines combine magnetic, acoustic, and pressure sensors, elevating precise field suppression requirements. The validation of India's multi-influence ground mine exemplifies the rising lethality that naval planners must counter. Historical loss figures reveal that mines remain the most cost-effective anti-surface weapon, anchoring the need for robust degaussing across blue-water and littoral vessels.

Elevated Capital Expenditure and Long-Term Maintenance Costs Limit Broader Adoption

The substantial upfront investment and ongoing operational expenses associated with advanced degaussing systems create adoption barriers, particularly for smaller naval forces with constrained budgets. Comprehensive degaussing installations can represent 2-5% of total vessel construction costs, and HTS-based packages command premiums that exceed copper-coil alternatives by 40-60%. Specialized lifecycle support-including cryogenic cooling plants, helium logistics, and certified technicians-adds USD 2-4 million over a 10-year maintenance horizon for a mid-sized combatant. These financial realities often force navies to confine full-spectrum signature management to aircraft carriers, submarines, and frontline destroyers while accepting residual magnetic footprints on lower-priority hulls. Consequently, market penetration among emerging maritime nations lags because capital charges crowd out other combat-system upgrades.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Retrofit Initiatives Targeting Older Surface Vessels for Degaussing Upgrades

- Emergence of High-Temperature Superconducting Coil Technology Enabling Compact and Efficient Systems

- Supply-Chain Vulnerabilities for HTS Tape and Rare-Earth-Based Magnetic Sensors Hinder Production Scalability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The segment totals underline how covert platforms anchor spending. The submarines category accounted for 29.65% of degaussing systems market revenue in 2024, while mine counter-measure ships will expand fastest at 7.89% CAGR. This performance differential mirrors the pronounced threat from influence mines and the strategic premium on under-ice and littoral concealment. Submarine programmes in Australia, India, and South Korea integrate full-hull coil sets at the design stage, contrasting with surface ships where retrofitting is the norm. Mine-hunter hulls already built with low-ferrite composites still add distributed micro-loops to crush residual magnetism. Destroyers and frigates maintain sizeable demand because mid-life upgrades coincide with radar and sonar refresh cycles, creating a multiplier effect for degaussing work scopes.

Navies weigh vessel-specific risk exposure when allocating budgets. Submarines face continuous passive detection risk and thus justify high-spec proprietary materials. Conversely, corvettes adopt modular architectures that spread costs using standardized coil modules rated for regional magnetic conditions. The nuanced mix obliges suppliers to field configurable systems ranging from 30-meter unmanned craft to 100,000-ton carriers without rewriting control code.

Continuous degaussing systems cornered 60.90% of 2024 revenue, highlighting their status as a baseline fit. Though degaussing remains core, deperming has re-emerged because modern steels retain higher remanence after repeated polar transits. A 6.12% CAGR through 2030 underscores how navies view periodic demagnetization as vital insurance before deployment into mined chokepoints. Contemporary pierside deperming cages employ pulsed direct current techniques capable of 95.5% flux-density reduction in half the legacy processing time. Additionally, portable deperming mats allow frigates to reset signatures during patrols without returning to home dock, raising operational readiness and underpinning a positive outlook for the deperming slice of the degaussing systems market.

Although a smaller niche, ranging facilities close the feedback loop by providing empirical magnetic-field data. Software analytics extrapolate these readings into coil-current setpoints, demonstrating that even lower-revenue segments create pull-through for higher-margin digital services.

The Degaussing Systems Market Report is Segmented by Vessel Type (Aircraft Carriers, Destroyers, Frigates, Corvettes, Submarines, and More), Solution (Degaussing, Deperming, and Ranging), Component (Control Units, Power Amplifiers, Coils and Cabling, and More), Installation Type (New-Build Installation and Retrofit), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 34.17% of 2024 revenue. The US Navy's destroyer and cruiser service-life-extension contracts alone sustain a multi-billion-dollar pipeline that favors domestically produced coils, magnetometers, and control units. Canada's Kingston-class degaussing refits and allied Foreign Military Sales (FMS) cases further reinforce the region's standing. With three qualified HTS testbeds, North American yards host the most advanced superconducting deployment programmes worldwide.

Asia-Pacific will post the highest 8.80% CAGR through 2030. Rising defense budgets and contested sea lanes propel demand. Japan extends HTS trials to its Mogami-class frigates, while Australia's AUKUS submarine endeavour integrates magnetic-signature management standards that exceed legacy benchmarks. India's mine programme, coupled with Southeast Asian littoral fleet expansion, accelerates the adoption of micro-degaussing solutions for unmanned platforms. Chinese shipyards embed AI-driven field-tuning software across new Type 054B builds, setting regional technology pace and prompting peers to keep up.

Europe remains pivotal, galvanized by NATO's Baltic and High North posture. Italy's mine-hunter initiative and France's FDI frigate series incorporate deperming and ranging combinations that drive systems-of-systems procurement. The United Kingdom's Type 31 programme specifies digital-twin-validated coil layouts as standard, underscoring regional commitment to magnetic hygiene. Parallel investments in polar research icebreakers introduce civil maritime niches for degaussing vendors, diversifying revenue streams beyond combatants.

- L3Harris Technologies Inc.

- Wartsila Corporation

- Polyamp AB

- Larsen & Toubro Limited

- Exail SAS

- IFEN S.p.A.

- American Superconductor Corporation (AMSC)

- Dayatech Merin Sdn Bhd

- DA Group

- Ultra Electronics Holdings Ltd.

- Babcock International Group

- Thales Group

- ESCO Technologies inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising naval modernization budgets accelerating investment in degaussing systems

- 4.2.2 Increased deployment of magnetic-influence sea mines driving demand for magnetic signature control

- 4.2.3 Expansion of retrofit initiatives targeting older surface vessels for degaussing upgrades

- 4.2.4 Emergence of high-temperature superconducting (HTS) coil technology enabling compact and efficient systems

- 4.2.5 Integration of AI-powered adaptive algorithms for real-time signature management

- 4.2.6 Growing requirement for systems in stealthy unmanned surface and underwater vehicles

- 4.3 Market Restraints

- 4.3.1 Elevated capital expenditure and long-term maintenance costs limit broader adoption

- 4.3.2 Extended acquisition timelines due to complex defense procurement procedures

- 4.3.3 Resource reallocation toward emerging railgun and directed-energy weapon systems reduces funding availability

- 4.3.4 Supply-chain vulnerabilities for HTS tape and rare-earth-based magnetic sensors hinder production scalability

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Vessel Type

- 5.1.1 Aircraft Carriers

- 5.1.2 Destroyers

- 5.1.3 Frigates

- 5.1.4 Corvettes

- 5.1.5 Submarines

- 5.1.6 Mine Countermeasure Vessels

- 5.1.7 Other Vessel Types

- 5.2 By Solution

- 5.2.1 Degaussing

- 5.2.2 Deperming

- 5.2.3 Ranging

- 5.3 By Component

- 5.3.1 Control Units (DCU)

- 5.3.2 Power Amplifiers

- 5.3.3 Coils and Cabling

- 5.3.4 Magnetometers and Sensors

- 5.3.5 Software and Analytics

- 5.4 By Installation Type

- 5.4.1 New-Build Installation

- 5.4.2 Retrofit

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Rest of Europe

- 5.5.3 South America

- 5.5.3.1 Brazil

- 5.5.3.2 Rest of South America

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 L3Harris Technologies Inc.

- 6.4.2 Wartsila Corporation

- 6.4.3 Polyamp AB

- 6.4.4 Larsen & Toubro Limited

- 6.4.5 Exail SAS

- 6.4.6 IFEN S.p.A.

- 6.4.7 American Superconductor Corporation (AMSC)

- 6.4.8 Dayatech Merin Sdn Bhd

- 6.4.9 DA Group

- 6.4.10 Ultra Electronics Holdings Ltd.

- 6.4.11 Babcock International Group

- 6.4.12 Thales Group

- 6.4.13 ESCO Technologies inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment