PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851923

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851923

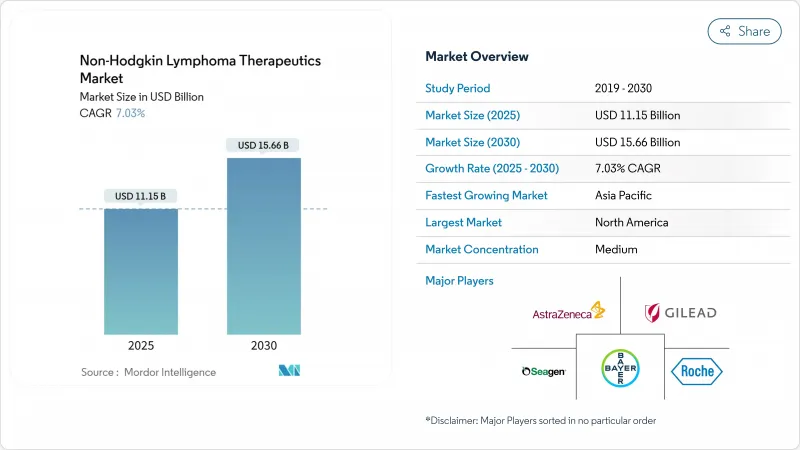

Non-Hodgkin Lymphoma Therapeutics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Non-Hodgkin Lymphoma Therapeutics Market size is estimated at USD 11.15 billion in 2025, and is expected to reach USD 15.66 billion by 2030, at a CAGR of 7.03% during the forecast period (2025-2030).

Growth reflects a decisive shift away from single-agent chemotherapy toward precision immunotherapies, especially chimeric antigen receptor T-cell (CAR-T) products and bispecific antibodies that produce durable remissions in heavily pre-treated patients. North America sustains leadership on the back of robust expedited-approval programs, early reimbursement adoption, and a mature network of certified cell-therapy centers. Meanwhile, Asia-Pacific registers the fastest uptake as domestic manufacturers scale automated cell-processing lines and governments expand oncology coverage. Therapy-line dynamics underscore unmet need: first-line regimens retain dominance, yet third-line and refractory populations spur the bulk of incremental revenue as physicians exhaust conventional options. Competitive intensity rises as large pharma invests in closed, modular CAR-T production platforms that compress vein-to-vein intervals, directly improving progression-free survival outcomes. Regulatory harmonization between U.S. and EU agencies continues to streamline dossier requirements, accelerating global launches of next-generation constructs.

Global Non-Hodgkin Lymphoma Therapeutics Market Trends and Insights

Growing Burden of Non-Hodgkin Lymphoma Drives Market Expansion

Annual U.S. diagnoses of diffuse large B-cell lymphoma now exceed 18,000 and continue to rise with population aging and improved detection capabilities. Relapse remains frequent, as 40% of patients fail to achieve durable remission after standard R-CHOP. Each subsequent therapy line raises failure risk, reaching 80% by the fifth attempt. Expanding incidence increases hospitalizations, infusion-center demand, and overall pharmaceutical spending, directly lifting Non-Hodgkin lymphoma therapeutics market revenue. Epidemiologic momentum is especially strong in middle-income economies where diagnostic imaging and immunohistochemistry capacity are scaling. Rising case volumes generate larger trial-ready patient pools that speed enrollment for innovative agents.

Innovative Drug Technologies Transform Treatment Paradigms

CAR-T constructs such as axicabtagene ciloleucel deliver 89% one-year progression-free survival in consolidation settings, far exceeding historical benchmarks. Subcutaneous bispecifics like epcoritamab achieve 38.9% complete responses in third-line large B-cell lymphoma versus 9.4% for chemo-immunotherapy. Automated stirred-tank bioreactors now reach cell densities above 5 X 10^6 cells/ml within seven days, cutting production time and contamination risk. Artificial-intelligence tools integrate genomic, biomarker, and outcomes data to guide sequencing, elevating response durability and reducing overtreatment. These advances strengthen clinical value propositions and reinforce payer willingness to reimburse premium list prices.

High Therapeutic Costs Limit Market Penetration

Median U.S. acquisition prices for single-dose CAR-T products exceed USD 400,000, and supportive-care costs lift total episode spending above USD 500,000 in many centers. Budget-impact models show that treating every eligible third-line patient would raise national oncology drug outlays by 3-4% annually, pressuring public and private payers. While value-based contracts temper financial exposure, their uptake remains patchy outside the United States. Emerging economies face steeper hurdles as limited specialized facilities and out-of-pocket payment structures restrict access, curbing the Non-Hodgkin lymphoma therapeutics market's global reach. Price sensitivity also influences formulary placements for bispecific antibodies and antibody-drug conjugates, decelerating uptake despite clinical benefit.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Expedited Pathways Accelerate Market Access

- Real-World Evidence Expansion Strengthens Reimbursement Decisions

- Safety Concerns and Adverse Effects Constrain Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Radiation therapy retained 47.23% share of the Non-Hodgkin lymphoma therapeutics market in 2024 owing to its established role in curative intent protocols and broad equipment availability. Yet chemotherapy posts the fastest 7.97% CAGR through 2030 as dose-dense regimens and novel maintenance schedules raise tolerability and extend use into older cohorts. The immunotherapy subset remains smaller but accelerates at 8.9% CAGR, supported by CAR-T and bispecific launches that address refractory disease gaps. A comparative real-world study reported 89% one-year progression-free survival for post-transplant CAR-T consolidation versus 54% under historical salvage, reinforcing clinical preference.

Broader adoption of closed, automated manufacturing has compressed production cycles from 22 days to 12 days, lowering facility overhead and making on-demand therapy more feasible. Bispecific antibodies deliver outpatient subcutaneous dosing, reducing chair-time and enabling administration in community clinics, which widens patient access. These advantages increase the immunotherapy contribution to overall revenue, steadily eroding chemotherapy dependence. Still, radiation remains entrenched for localized early-stage presentations, underlining a multimodal future in which novel biologics are layered onto foundational modalities.

The Non-Hodgkin Lymphoma Therapeutics Market Report is Segmented by Therapy Type (Chemotherapy, Radiation Therapy, Targeted Therapy, Immunotherapy, Other Therapies), Cell Type (B-Cell Lymphomas, T-Cell Lymphomas), Treatment Line (First-Line, Second-Line, Third-Line & Refractory), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 45.45% of 2024 revenue, as widespread payer coverage and 105 certified cell-therapy centers under the U.S. FACT accreditation program enable rapid uptake. The region's non-Hodgkin lymphoma therapeutics market share is expected to remain stable through 2030 despite price headwinds, as new indications offset unit-cost pressure. Regional real-world data networks such as CIBMTR feed continuous safety updates that refine protocols and sustain clinician confidence.

Europe follows with a mature yet slower-growing base where health-technology assessments shape adoption. While EMA approval lags FDA by roughly three quarters, outcome-based reimbursement pilots in Germany and Spain are unlocking incremental access. National programs invest in domestic cell-manufacturing hubs, reducing cross-border logistical delays and aligning with sustainability targets. The Non-Hodgkin lymphoma therapeutics market size linked to key EU5 countries is anticipated to rise in the coming years, primarily from bispecific uptake that requires no leukapheresis.

Asia-Pacific registers the most vigorous 8.87% CAGR as China's expedited local regulatory pathways and Medicare-style reimbursement pilot dramatically expand patient access. More than 20 Chinese manufacturers operate commercial CAR-T facilities, and point-of-care production models shorten turnaround to seven days in top oncology hospitals. Japan's Pharmaceutical and Medical Device Agency supports conditional approvals with post-marketing surveillance, accelerating earlier patient availability. These initiatives combine with rising middle-class insurance penetration to elevate overall regional demand. Latin America and the Middle East & Africa remain nascent but improving as regional centers of excellence emerge in Brazil, Saudi Arabia, and South Africa. Cross-border patient flow, collaborative training programs, and technology-transfer partnerships gradually enhance localized treatment capacity, broadening the Non-Hodgkin lymphoma therapeutics market footprint beyond traditional high-income geographies.

- Roche

- Novartis

- Gilead Sciences Inc. / Kite Pharma

- Bristol-Myers Squibb

- Seagen

- Takeda Pharmaceuticals

- AstraZeneca

- Janssen Biotech / Johnson & Johnson

- BeiGene Ltd.

- Genmab

- Regeneron Pharmaceuticals

- ADC Therapeutics

- Incyte Corp.

- Eli Lilly and Company

- Bayer

- Amgen

- Abbvie

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Burden of Non-Hodgkin Lymphoma (NHL)

- 4.2.2 Demand For Innovative Drugs & Novel Technologies

- 4.2.3 Favourable Regulatory Approvals & Expedited Pathways

- 4.2.4 Expansion of Real-World Evidence Datasets Boosting Reimbursement

- 4.2.5 Precision-Diagnostic Biomarkers Driving Earlier-Line Adoption

- 4.2.6 Shift Toward Personalized Medicine

- 4.3 Market Restraints

- 4.3.1 High Cost of Novel NHL Therapies

- 4.3.2 Adverse Effects & Safety Concerns (E.G., CRS, Neuro-Toxicity)

- 4.3.3 Autologous Cell-Therapy Manufacturing Bottlenecks

- 4.3.4 Stringent Regulations and Guidelines Regarding the Treatments

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Pipeline Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value - USD)

- 5.1 By Therapy Type

- 5.1.1 Chemotherapy

- 5.1.2 Radiation Therapy

- 5.1.3 Targeted Therapy

- 5.1.4 Immunotherapy (incl. CAR-T, Bispecifics)

- 5.1.5 Other Therapies

- 5.2 By Cell Type

- 5.2.1 B-cell Lymphomas

- 5.2.2 T-cell Lymphomas

- 5.3 By Treatment Line

- 5.3.1 First-line

- 5.3.2 Second-line

- 5.3.3 Third-line & Refractory

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 F. Hoffmann-La Roche Ltd.

- 6.3.2 Novartis AG

- 6.3.3 Gilead Sciences Inc. / Kite Pharma

- 6.3.4 Bristol Myers Squibb Co.

- 6.3.5 Seagen Inc.

- 6.3.6 Takeda Pharmaceutical Co. Ltd.

- 6.3.7 AstraZeneca PLC

- 6.3.8 Janssen Biotech / Johnson & Johnson

- 6.3.9 BeiGene Ltd.

- 6.3.10 Genmab A/S

- 6.3.11 Regeneron Pharmaceuticals

- 6.3.12 ADC Therapeutics SA

- 6.3.13 Incyte Corp.

- 6.3.14 Eli Lilly & Co.

- 6.3.15 Bayer AG

- 6.3.16 Amgen Inc.

- 6.3.17 AbbVie Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment