PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851933

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851933

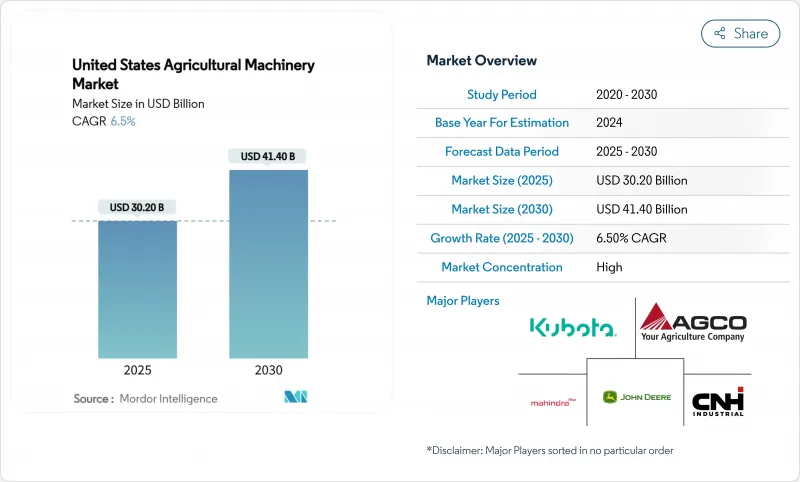

United States Agricultural Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The United States agricultural machinery market size is valued at USD 30.2 billion in 2025 and is projected to grow at a CAGR of 6.5%, reaching USD 41.4 billion by 2030.

Federal incentives for climate-smart practices, precision technology retrofits, and electrification investments help counterbalance cyclical market fluctuations. Equipment owners focus on upgrading capabilities to reduce operational costs and achieve sustainability goals, increasing demand for telematics, predictive maintenance, and autonomous-ready systems. Dealer consolidation improves after-sales service networks, while leasing and subscription options help mitigate the impact of higher interest rates. The irrigation segments demonstrate higher growth rates in the United States agricultural machinery market, driven by increasing water scarcity and stricter emissions regulations.

United States Agricultural Machinery Market Trends and Insights

Widespread Adoption of Precision-Ag Retro-Fit Kits

Retro-fit solutions enable farmers to extend their existing fleet's lifespan while reducing fertilizer and pesticide usage by up to 30% through data-driven improvements. The investment of USD 50,000 per tractor for retrofitting is significantly lower than the USD 400,000 required for new autonomous-ready equipment, typically resulting in a return on investment within three years. Mid-scale row-crop farms increasingly adopt these solutions to maintain cost competitiveness without increasing debt. Equipment dealers benefit from additional service revenue through installation and calibration of retrofit kits, which strengthens customer relationships and improves profitability. The growing adoption of modular upgrades extends equipment replacement cycles, causing Original Equipment Manufacturers (OEMs) to shift their focus from unit sales to software and integration services.

Electrification Road-Maps by Major Original Equipment Manufacturers

Deere & Company plans to launch its first all-electric, autonomous-capable tractor in 2026 and has invested in Kreisel Electric for battery supply. AGCO introduced the Fendt e100 Vario to pilot fleets in 2024, supported by a 60% increase in research and development spending focused on electric powertrains. Current battery density limits electric tractors to under-120-horsepower applications, which align with the requirements of fruit, vegetable, and dairy farms. The Natural Resources Conservation Service (NRCS) offers cost-share programs that can cover over 50% of purchase costs, reducing financial barriers for small farms. While manufacturers expect future battery technology improvements to enable higher-horsepower applications, current progress has encouraged component suppliers to expand United States battery and inverter production.

Dealer Technician Shortage

The equipment service industry faces a significant labor shortage. The consolidation of service locations has reduced the number of physical stores, increasing response times during critical planting and harvest periods. Modern precision equipment requires specialized diagnostic capabilities that exceed the skills available in rural labor markets, compelling Original Equipment Manufacturers (OEMs) to expand remote support services and implement modular component replacement systems. These labor constraints have led farmers to restrict their purchases of agricultural machinery.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of Telematics-Based Predictive Maintenance

- Climate-Smart Grant Incentives

- Lengthy Environmental Protection Agency Tier 5 Emission Compliance Lead-Times

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tractors maintain a 51% share of the United States agricultural machinery market in 2024, demonstrating their essential role in tillage, seeding, and material handling. The segment's revenue growth stems from high-horsepower models, while compact tractors increasingly incorporate electric drivetrains for specialty farming applications. Irrigation equipment, though a smaller segment, is projected to achieve the highest growth rate at 9.4% CAGR through 2030. Modern irrigation systems, including center pivots, drip lines, and sensor-controlled valves, integrate real-time soil moisture data, reducing water consumption by up to 25%. This growth aligns with Western state groundwater regulations and federal WaterSMART program incentives.

In plowing and cultivating systems, manufacturers incorporate variable-depth tillage technology to reduce soil disruption, maintaining steady growth despite increasing no-till farming practices. Advanced seeding and planting equipment enable precise single-kernel placement, improving emergence rates and supporting precise nutrient application. While harvesting machinery demand correlates with row-crop prices, new combines featuring predictive ground-speed automation improve fuel efficiency and throughput, driving replacement demand. Farmers increasingly opt to upgrade existing equipment with autonomous guidance and variable-rate controllers instead of purchasing new machinery, resulting in parts and digital service revenue exceeding equipment sales. Across equipment categories, sensor systems and ISOBUS-compatible controllers establish brand-independent ecosystems, reducing manufacturer lock-in and requiring traditional manufacturers to provide open APIs to maintain tractor market position.

The United States Agricultural Machinery Market Report is Segmented by Product Type (Tractors, Plowing and Cultivating Machinery, and More), and by Farm Size (Less Than 500 Acres, 500-2, 000 Acres, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Deere & Company

- CNH Industrial NV

- AGCO Corporation

- Kubota Corporation

- Mahindra & Mahindra Ltd.

- CLAAS KGaA mbH

- KUHN SAS

- Same Deutz-Fahr S.P.A.

- Kinze Manufacturing

- Horsch, LLC

- Ploeger Oxbo Group B.V.

- Argo Tractors S.p.A.

- Netafim Limited (An Orbia Business)

- Valmont Industries, Inc.

- Yanmar Holdings Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Widespread Adoption of Precision-Ag Retro-Fit Kits

- 4.2.2 Electrification Road-Maps by Major Original Equipment Manufacturers

- 4.2.3 Rising Adoption of Telematics-Based Predictive Maintenance

- 4.2.4 Climate-Smart Grant Incentives

- 4.2.5 Surge in Bespoke Equipment Leasing Models

- 4.2.6 Venture-Backed Robotics Start-Ups Targeting Speciality Crops

- 4.3 Market Restraints

- 4.3.1 Dealer Technician Shortage

- 4.3.2 Patchy Rural 5G Coverage for Connected Machinery

- 4.3.3 Volatile Commodity-Price Swings Curbing Farm Capital Expenditure

- 4.3.4 Lengthy Environmental Protection Agency Tier 5 Emission Compliance Lead-times

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Tractors

- 5.1.2 Plowing and Cultivating Machinery

- 5.1.2.1 Plows

- 5.1.2.2 Harrows

- 5.1.2.3 Cultivators and Tillers

- 5.1.2.4 Other Plowing and Cultivating Machinery

- 5.1.3 Planting Machinery

- 5.1.3.1 Seed Drills

- 5.1.3.2 Planters

- 5.1.3.3 Spreaders

- 5.1.3.4 Other Planting Machinery

- 5.1.4 Harvesting Machinery

- 5.1.4.1 Combine Harvesters

- 5.1.4.2 Forage Harvesters

- 5.1.4.3 Other Harvesting Machinery

- 5.1.5 Haying and Forage Machinery

- 5.1.5.1 Mowers

- 5.1.5.2 Balers

- 5.1.5.3 Other Haying and Forage Machinery

- 5.1.6 Irrigation Machinery

- 5.1.6.1 Sprinkler Irrigation

- 5.1.6.2 Drip Irrigation

- 5.1.6.3 Other Irrigation Machinery

- 5.1.7 Other Agricultural Machinery

- 5.2 By Farm Size

- 5.2.1 Less Than 500 acres

- 5.2.2 500-2,000 acres

- 5.2.3 More Than 2,000 acres

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 CNH Industrial NV

- 6.4.3 AGCO Corporation

- 6.4.4 Kubota Corporation

- 6.4.5 Mahindra & Mahindra Ltd.

- 6.4.6 CLAAS KGaA mbH

- 6.4.7 KUHN SAS

- 6.4.8 Same Deutz-Fahr S.P.A.

- 6.4.9 Kinze Manufacturing

- 6.4.10 Horsch, LLC

- 6.4.11 Ploeger Oxbo Group B.V.

- 6.4.12 Argo Tractors S.p.A.

- 6.4.13 Netafim Limited (An Orbia Business)

- 6.4.14 Valmont Industries, Inc.

- 6.4.15 Yanmar Holdings Co., Ltd.

7 Market Opportunities and Future Outlook