PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851955

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851955

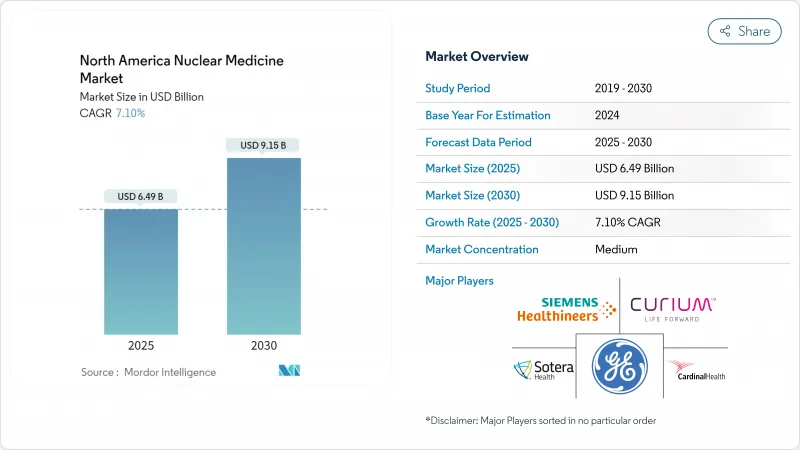

North America Nuclear Medicine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The North America nuclear medicine market stands at USD 8.02 billion in 2025 and is forecast to reach USD 13.65 billion by 2030, translating to an 11.23% CAGR.

This expansion underscores the segment's pivotal role in precision diagnostics and targeted therapy across oncology, cardiology, and neurology. Sustained investment in radiotheranostics, broader clinical indications, and supportive reimbursement policies continue to lift procedure volumes despite macro-economic pressures. Supply chain localization, particularly for molybdenum-99 and actinium-225, further reduces procurement risk and strengthens value-chain resilience. Intensifying competition among incumbents and new entrants accelerates innovation while patent litigation shapes strategic positioning.

North America Nuclear Medicine Market Trends and Insights

Rising burden of cancer & CVD

Cancer incidence continues to climb across North America, with cardiovascular disease remaining the leading cause of mortality, sustaining demand for accurate diagnostic and therapeutic nuclear medicine procedures. Demographic aging amplifies this need as prostate, breast, and lung cancer prevalence rises sharply beyond age 60. Pediatric indications now grow following FDA approval of lutetium Lu 177 dotatate for patients aged 12 and above, opening new addressable populations. While traditional SPECT cardiac volumes ebb, PET myocardial perfusion imaging gains favor for its higher specificity. The convergence of oncology and cardiology applications enables providers to streamline care pathways and cross-sell services, anchoring multi-specialty revenue streams.

Hybrid imaging (SPECT/CT, PET/CT) adoption surge

North American healthcare systems increasingly adopt these technologies, with cardiac PET imaging gaining significant traction among US cardiologists as demonstrated by expanding clinical adoption and improved reimbursement frameworks under Centers for Medicare & Medicaid Services reforms in 2025 that provide separate payment pathways for advanced diagnostic radiopharmaceuticals. GE HealthCare's Flyrcado tracer, with a 109-minute half-life, broadens stress testing feasibility and attracts outpatient cardiology centers. Detector advances such as cadmium zinc telluride improve resolution while trimming radiation dose, addressing clinician and patient safety. Artificial intelligence algorithms automate lesion quantification, reducing interpretation variability and accelerating report turnaround.

Short half-life logistics bottlenecks

Many diagnostic isotopes decay within hours, demanding just-in-time distribution. Fluorine-18's 6-hour half-life restricts shipment zones to roughly 200 miles. In 2024, unexpected European reactor downtime created 50-100% shortages in technetium-99m across multiple U.S. states, delaying elective scans. Cold-chain compliance adds cost, and rural sites often cannot meet delivery windows, limiting service availability. Longer-lived copper-64 offers partial relief, though widespread clinical adoption hinges on additional infrastructure and trial data.

Other drivers and restraints analyzed in the detailed report include:

- Domestic Mo-99 supply build-out (NorthStar, etc.)

- High CAPEX & regulatory hurdles for cyclotrons

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Diagnostic radiopharmaceuticals retained 72.70% share of the North America nuclear medicine market in 2024, supported by entrenched reimbursement and entrenched clinician familiarity. Therapeutic agents, however, are growing much faster at an 11.45% CAGR as radioligands like lutetium-177 PSMA address advanced metastatic disease with favorable safety profiles. The North America nuclear medicine market size for therapeutics is set to surpass USD 4.6 billion by 2030, reflecting accelerating adoption among oncologists. SPECT remains dominant in routine bone scans, while PET's superior resolution wins neurology and oncology referrals. Artificial intelligence-driven dosimetry improves treatment precision, reinforcing payer confidence in premium reimbursement tiers.

A reinforcing loop exists between diagnostic and therapeutic revenues: positive imaging experiences facilitate patient enrollment in companion therapeutics. Novartis's Pluvicto reached USD 1 billion in U.S. sales during the first nine months of 2024, validating commercial appetite for high-value radiotheranostics. CMS payment reform in 2025 created a separate APC for diagnostic tracers above USD 630, improving hospital margins and encouraging inventory expansion. The North America nuclear medicine industry now positions therapeutic innovation as a primary differentiator among manufacturers that once concentrated on diagnostic agents.

Oncology represented 41.45% of the North America nuclear medicine market in 2024, reflecting its central role in tumor staging and therapy monitoring. The North America nuclear medicine market size for oncology applications is forecast to cross USD 5.6 billion in 2030 at an 11.2% CAGR. Neurology is the fastest-growing application, expanding 11.78% annually as amyloid and tau PET increase Alzheimer's diagnostic accuracy. CMS travel policy updates in 2025 lowered out-of-pocket costs for Medicare beneficiaries, further encouraging scan uptake.

Neuroimaging demand spurs supply chain adjustments for fluorine-18 tracers like Neuraceq, recently added through Lantheus's USD 750 million acquisition of Life Molecular Imaging. Advanced AI algorithms shorten interpretation time from 12 minutes to 4 minutes per scan, addressing neuroradiologist shortages. Cardiology maintains relevance through PET perfusion imaging, which grew 6% year-over-year in 2024 despite SPECT declines. Endocrinology remains steady, with thyroid uptake studies and iodine-131 therapy stable across major U.S. academic centers.

The North America Nuclear Medicine Market Report is Segmented by Product Type (Diagnostic Radiopharmaceuticals, Therapeutic Radiopharmaceuticals), Application (Oncology, Cardiology, Neurology, and More), Radioisotope (Tc-99m, F-18, I-131, Lu-177, Y-90, Ga-68, Ac-225, Others), End User (Hospitals, Diagnostic Imaging Centers, and More), and Geography (US, Canada, Mexico). Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- GE HealthCare Technologies Inc.

- Siemens Healthineers

- Cardinal Health

- Curium Pharma

- Bracco Imaging S.p.A.

- Bayer AG (Radiology Division)

- Novartis

- Lantheus

- Jubilant Pharma Ltd (Jubilant Radiopharma)

- Eckert & Ziegler AG

- Nordion (Sotera Health Co.)

- Telix Pharmaceuticals Ltd.

- NorthStar Medical Radioisotopes LLC

- Isotopia Molecular Imaging Ltd.

- BWX Technologies Inc. (BWXT Medical)

- IsoRay

- Ion Beam Applications SA

- SOFIE Biosciences Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising burden of cancer & CVD

- 4.2.2 Hybrid imaging (SPECT/CT, PET/CT) adoption surge

- 4.2.3 Domestic Mo-99 supply build-out (NorthStar, etc.)

- 4.2.4 FDA fast-tracks novel radiotheranostics

- 4.2.5 Alpha-emitter pipeline (Ac-225, Pb-212) expansion

- 4.2.6 AI-enabled dose-reduction & workflow gains

- 4.3 Market Restraints

- 4.3.1 Short half-life logistics bottlenecks

- 4.3.2 High CAPEX & regulatory hurdles for cyclotrons

- 4.3.3 Mo-99 HEU-to-LEU transition delays

- 4.3.4 Radiopharmacist talent shortage vs USP <825>

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Diagnostic Radiopharmaceuticals

- 5.1.1.1 SPECT

- 5.1.1.2 PET

- 5.1.1.3 Others

- 5.1.2 Therapeutic Radiopharmaceuticals

- 5.1.2.1 Targeted Beta Therapy

- 5.1.2.2 Targeted Alpha Therapy

- 5.1.2.3 Brachytherapy

- 5.1.1 Diagnostic Radiopharmaceuticals

- 5.2 By Application

- 5.2.1 Oncology

- 5.2.2 Cardiology

- 5.2.3 Neurology

- 5.2.4 Endocrinology

- 5.2.5 Other Applications

- 5.3 By Radioisotope

- 5.3.1 Technetium-99m

- 5.3.2 Fluorine-18

- 5.3.3 Iodine-131

- 5.3.4 Lutetium-177

- 5.3.5 Yttrium-90

- 5.3.6 Gallium-68

- 5.3.7 Actinium-225

- 5.3.8 Others

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Diagnostic Imaging Centers

- 5.4.3 Academic & Research Institutes

- 5.4.4 Pharmaceutical Companies

- 5.5 North America

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 GE HealthCare Technologies Inc.

- 6.3.2 Siemens Healthineers AG

- 6.3.3 Cardinal Health Inc.

- 6.3.4 Curium Pharma

- 6.3.5 Bracco Imaging S.p.A.

- 6.3.6 Bayer AG (Radiology Division)

- 6.3.7 Novartis AG (Advanced Accelerator Applications)

- 6.3.8 Lantheus Holdings Inc.

- 6.3.9 Jubilant Pharma Ltd (Jubilant Radiopharma)

- 6.3.10 Eckert & Ziegler AG

- 6.3.11 Nordion (Sotera Health Co.)

- 6.3.12 Telix Pharmaceuticals Ltd.

- 6.3.13 NorthStar Medical Radioisotopes LLC

- 6.3.14 Isotopia Molecular Imaging Ltd.

- 6.3.15 BWX Technologies Inc. (BWXT Medical)

- 6.3.16 Isoray Inc.

- 6.3.17 Ion Beam Applications SA

- 6.3.18 SOFIE Biosciences Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment