PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852001

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852001

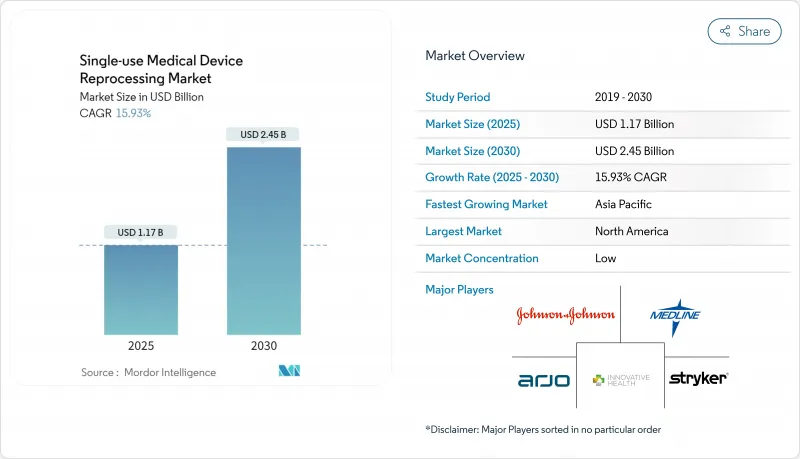

Single-use Medical Device Reprocessing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The single-use medical device reprocessing market is valued at USD 1.17 billion in 2025 and is forecast to expand to USD 2.45 billion in 2030 at a 15.93% CAGR, underscoring robust demand for proven cost-containment and sustainability solutions in global healthcare systems .

Regulatory clarity from the U.S. FDA's May 2024 guidance on remanufacturing and growing acceptance of vaporized hydrogen peroxide sterilization have reduced compliance uncertainty and broadened the universe of devices considered safe for reprocessing. Hospital procurement teams view reprocessing as a line-item lever for margin preservation amid inflation and reimbursement headwinds, especially after documented savings of USD 451 million in 2024 across 17 countries. Sustainability mandates, Scope-3 carbon accounting and antitrust enforcement against restrictive OEM contracts are accelerating device-level adoption, while AI-enabled traceability platforms and automated sterilizers reinforce patient-safety confidence .

Global Single-use Medical Device Reprocessing Market Trends and Insights

Cost-containment Pressure on Hospitals

Shrinking operating margins have moved reprocessing from optional to essential in hospital supply-chain playbooks, often delivering 40-60% device-level savings versus OEM list prices . Medicare payment reforms and private-payer contracting heightened visibility of disposable device spend, prompting the Veterans Health Administration to revisit its own reprocessing restrictions in 2025 . Chief financial officers increasingly embed reprocessing ROIs in annual capital-allocation models, translating to systematic adoption across multi-hospital networks . The scale of savings is now material to bond-rating agencies evaluating nonprofit health-system liquidity, reinforcing management commitment . As inflation persists, financial stewardship is expected to underpin at least one-third of new account conversions through 2027 .

Regulatory Approvals & Clearances for Reprocessed SUDs

The FDA's 2024 remanufacturing guidance clarified boundaries between servicing and reprocessing, reducing legal ambiguity for third-party operators . Vaporized hydrogen peroxide earned recognition as an established sterilization modality, diversifying validated methods beyond ethylene oxide . Japan embedded single-use device re-manufacturing into its QMS ordinance with staggered compliance deadlines through 2024, setting a template for other APAC regulators . The FDA's 2025 approvals of VARIPULSE and Sphere-9 catheter systems, each containing reusable components, signaled growing confidence in mixed-use platforms . These milestones collectively expand the single-use medical device reprocessing market addressable base beyond cardiology into complex electrophysiology segments .

OEM Lobbying & Restrictive Labeling Practices

Johnson & Johnson's 2025 antitrust loss, accompanied by a USD 442 million penalty, underscores systemic OEM resistance to reprocessing adoption . Manufacturers continue to leverage "single-use" labels to sow legal uncertainty, particularly in emerging markets with nascent regulatory oversight . Trade associations funded by OEMs lobby against expanded device-eligibility lists, delaying clinical uptake in high-volume categories like laparoscopic instruments . Even where antitrust scrutiny curbs overt contract restrictions, soft barriers such as staff-training withdrawal can still impede provider confidence . The resulting legal environment is expected to shave nearly three percentage points off projected CAGR in the near term .

Other drivers and restraints analyzed in the detailed report include:

- Sustainability & Waste-reduction Mandates

- ESG Reporting Tying Scope-3 Emissions to Procurement

- EU MDR Article 17 Cross-border Fragmentation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The cardiovascular catheter category delivered 37.56% of single-use medical device reprocessing market size in 2024, sustained by well-documented clinical equivalency studies and standardized sterilization workflows . Electrophysiology catheters are pacing the field with a 16.09% CAGR, catalyzed by FDA approvals for VARIPULSE and Sphere-9 systems that incorporate reusable components . Laparoscopic instruments benefit from robotic-surgery scale, yet complex geometries demand automated cleaning tunnels available chiefly at large commercial reprocessors . Gastroenterology device growth hinges on sterilization breakthroughs like ULTRA GI hydrogen-peroxide gas-plasma cycles, which mitigate past infection risks . Orthopedic external-fixation hardware remains niche due to patient-custom configurations and extended wear times, while general-surgery tools provide steady volume but face pricing commoditization pressures .

Technological advances, notably AI-based device-tracking tags and cloud analytics, now allow product-level performance benchmarking across reuse cycles, fostering surgeon trust in reprocessed alternatives . Enhanced inspection optics and non-destructive integrity testing continue to elevate quality assurance, helping cardiovascular and laparoscopic devices maintain near-parity with new OEM units in failure rates . As category life-cycle emissions enter formal ESG scorecards, providers prioritize high-volume disposable categories such as catheters for earliest conversion, reinforcing leadership of cardiovascular subsegments in the single-use medical device reprocessing market .

Third-party operators accounted for 84.45% of single-use medical device reprocessing market share in 2024, reflecting scale advantages in sterilization, validation and logistics . The sector's 16.37% CAGR through 2030 is fueled by payer and regulator preference for ISO-certified specialist facilities over resource-strained in-house units . Consolidation continues, exemplified by Medline's 2024 acquisition of Ecolab's surgical solutions business, integrating reprocessing into a full-line distribution model that simplifies provider procurement.

Hospitals evaluating internal programs confront capital outlays for sterilizers, traceability software and quality testing that exceed USD 5 million per site, tipping cost-benefit calculations toward outsourcing . Regulatory amendments harmonizing FDA QSR with ISO 13485 in 2026 are expected to heighten documentation burdens, disadvantaging smaller in-house units lacking dedicated regulatory teams . As commercial partners adopt AI vision-inspection and robotic packing lines, throughput efficiencies generate 5-8-point margin advantages, widening the gap versus hospital-run operations. Accordingly, most top-100 U.S. IDNs now operate hybrid models where only very low-volume instruments remain on-site, while high-volume cath-lab and EP devices ship to third-party plants weekly.

The Single-Use Medical Device Reprocessing Market Report is Segmented by Product Type (Cardiovascular Catheters, Electrophysiology Catheters, and More), Service Provider (Third-party/Commercial Reprocessors, In-house/Hospital Reprocessing Units), Application (Cardiology, and More), End User (Hospitals & Surgical Centers, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 43.53% of 2024 revenue, underpinned by FDA guidance certainty, antitrust enforcement and well-developed third-party networks . The U.S. market also benefits from hospital sustainability charters that align reprocessing with ESG key-performance indicators . Canada's public-funded health system adopts reprocessing to offset budget caps, while Mexico's medical-device cluster in Baja California offers near-shore sterilization capacity expansion for cross-border providers .

Asia-Pacific is on track to record a 17.25% CAGR to 2030, led by Japan's QMS rule harmonization and China's hospital-modernization programs, which target 70% device-reuse certification in tier-1 cities by 2028 . India's Ayushman Bharat scheme expands insurance coverage, compelling public hospitals to stretch fixed budgets, thereby elevating reprocessing in procurement tenders starting 2026 . South Korea and Australia, both early electron-beam sterilization adopters, pilot AI-tracked catheter reuse to meet national zero-waste targets by 2035 .

Europe's outlook is tempered by Article 17 fragmentation that introduces divergent reprocessing rules among member states, inflating compliance costs by up to 25% for cross-border operators . Germany's potential CE-reprocessing ban could remove USD 90 million in annual revenue if enacted in 2026, although Denmark and the Netherlands have issued guidance enabling reprocessing under strict quality-management oversight . The United Kingdom, outside EU frameworks, formally targets elimination of avoidable single-use medical goods by 2045, positioning reprocessing as a central compliance mechanism . France's health ministry launched a limited pilot in 2024 to evaluate duodenoscope reprocessing economics, possibly informing national policy in 2027 .

- Stryker

- SterilMed (Johnson & Johnson)

- Medline ReNewal

- Innovative Health

- Northeast Scientific

- Vanguard

- Cardinal Health

- ReNu Medical

- Hygia Health Services

- Midwest Reprocessing Center

- Centurion Medical Products

- Arjo

- Sterimed Inc.

- Vascular Solutions

- Suretek Medical

- Medtronic (Cath Lab Reprocessing)

- Becton Dickinson (Tray Return Programs)

- Siemens Healthineers (Eco-Cycle Services)

- Koninklijke Philips

- Restore Medical Solutions

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cost-containment pressure on hospitals

- 4.2.2 Regulatory approvals & clearances for reprocessed SUDs

- 4.2.3 Sustainability & waste-reduction mandates

- 4.2.4 ESG reporting tying Scope-3 emissions to procurement

- 4.2.5 Antitrust rulings curbing OEM restrictive contracts

- 4.2.6 Supply-chain resilience post-pandemic PPE shortages

- 4.3 Market Restraints

- 4.3.1 OEM lobbying & restrictive labelling practices

- 4.3.2 Device design limits to multiple re-use cycles

- 4.3.3 EU MDR Article 17 cross-border fragmentation

- 4.3.4 AI-enabled traceability exposing reprocessing failures

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type (Value, USD)

- 5.1.1 Cardiovascular Catheters

- 5.1.2 Electrophysiology Catheters

- 5.1.3 Laparoscopic Instruments

- 5.1.4 Gastroenterology Devices

- 5.1.5 Orthopedic External Fixation Devices

- 5.1.6 General Surgery Instruments

- 5.2 By Service Provider (Value, USD)

- 5.2.1 Third-party /Commercial Reprocessors

- 5.2.2 In-house /Hospital Reprocessing Units

- 5.3 By Application (Value, USD)

- 5.3.1 Cardiology

- 5.3.2 Gastroenterology

- 5.3.3 Orthopedics

- 5.3.4 Urology

- 5.3.5 General Surgery

- 5.4 By End User (Value, USD)

- 5.4.1 Hospitals & Surgical Centers

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Specialty Clinics & Cath Labs

- 5.4.4 Academic & Research Institutes

- 5.5 By Geography (Value, USD)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Stryker

- 6.3.2 SterilMed (Johnson & Johnson)

- 6.3.3 Medline ReNewal

- 6.3.4 Innovative Health

- 6.3.5 Northeast Scientific

- 6.3.6 Vanguard AG

- 6.3.7 Cardinal Health

- 6.3.8 ReNu Medical

- 6.3.9 Hygia Health Services

- 6.3.10 Midwest Reprocessing Center

- 6.3.11 Centurion Medical Products

- 6.3.12 Arjo

- 6.3.13 Sterimed Inc.

- 6.3.14 Vascular Solutions

- 6.3.15 Suretek Medical

- 6.3.16 Medtronic (Cath Lab Reprocessing)

- 6.3.17 Becton Dickinson (Tray Return Programs)

- 6.3.18 Siemens Healthineers (Eco-Cycle Services)

- 6.3.19 Philips

- 6.3.20 Restore Medical Solutions

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment