PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035064

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035064

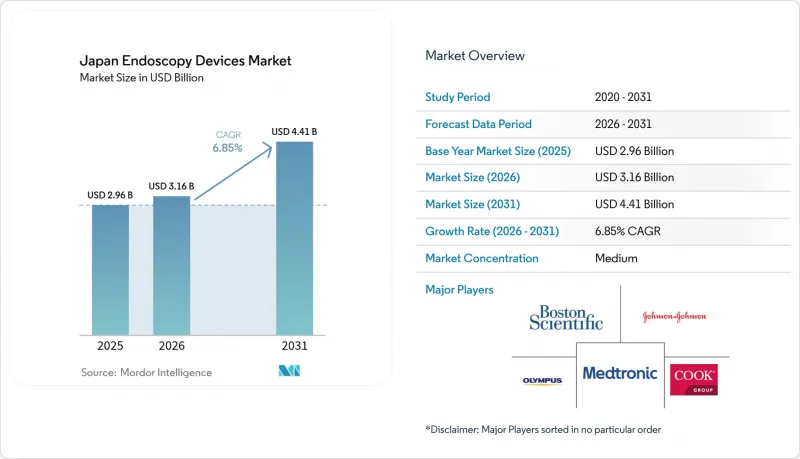

Japan Endoscopy Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Japan endoscopy devices market size was valued at USD 2.96 billion in 2025 and estimated to grow from USD 3.16 billion in 2026 to reach USD 4.41 billion by 2031, at a CAGR of 6.85% during the forecast period (2026-2031).

Japan's universal health insurance, a rapidly aging population, and rising demand for minimally invasive care together fuel sustained procedure growth. Robot-assisted platforms, AI-guided visualization, and 4K/8K imaging upgrades keep capital expenditure high while enabling earlier lesion detection and more precise therapeutic intervention. Ambulatory surgical centers (ASCs) are scaling quickly as cost-efficient hubs, shifting routine diagnostic work away from hospitals and stimulating demand for compact, high-throughput systems. Domestic champions Olympus, Fujifilm, and Hoya (Pentax) currently dominate, yet foreign entrants leverage AI modules and single-use accessories to gain share, intensifying competitive technology cycles. Forward-looking providers view advanced endoscopy suites as revenue generators rather than cost centers as reimbursement codes for AI-enhanced procedures outpace standard tariffs.

Japan Endoscopy Devices Market Trends and Insights

Universal Healthcare Coverage Driving Advanced Endoscopy Adoption

Japan's 2024 revision of National Health Insurance introduced enhanced reimbursement codes for AI-assisted procedures, boosting hospital revenue by up to 30% compared with conventional scopes. Facilities consequently accelerate equipment upgrades to maintain tariff eligibility. Academic hospitals moved first, but regional centers now follow as capital budgets align with higher billings. The policy favors early detection, thereby pushing demand for CADe-enabled colonoscopy that lifts adenoma detection rates and reduces repeat visits. Vendors respond by bundling analytics software with new towers to streamline purchasing decisions. Over the medium term, reimbursement alignment is expected to standardize AI-guided visualization across most prefectures.

Government-Led Cancer Screening Mandates Elevating Procedure Volumes

Biennial gastric and colorectal screenings for citizens older than 50 became compulsory in 2024, driving a 23% jump in total endoscopic procedures that year and a further 18% rise expected in 2025. The mandates particularly boost endoscopic resection volumes, with gastric ESD cases already climbing to 57% of tumor resections. Provincial clinics expand capacity to meet quotas, prompting bulk procurement of visualization towers and high-definition scopes. The government links subsidy allocation to throughput metrics, incentivizing real-time data reporting via the Japan Endoscopy Database. Over the long term, the screening policy anchors a stable procedure pipeline that underpins the Japan endoscopy devices market.

Capital Costs and Price Controls Creating Investment Barriers

A high-definition system with advanced imaging costs JPY 30-45 million (USD 200,000-300,000). Biennial NHI revisions trim standard-procedure tariffs by 4.2%, stretching payback periods, especially for clinics with limited volume. Subsidies favor new technology, yet smaller providers struggle to raise upfront capital, widening the digital gap. Group purchasing and manufacturer leasing schemes partially mitigate hurdles, but medium-term impact on market CAGR remains negative.

Other drivers and restraints analyzed in the detailed report include:

- Ambulatory Surgical Centers Expansion Transforming Care Delivery

- AI Integration Revolutionizing Diagnostic Capabilities

- Workforce Shortages Limiting Procedural Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Robot-assisted systems represent the fastest-growing category, expanding at a 14.1% CAGR on a small base, while flexible scopes hold the largest revenue share at 53.40% in 2025, underpinning the Japan endoscopy devices market size for visualization hardware. The Hinotori system's expanded 2024 approval illustrates clinical momentum and vendor commitment. Advanced articulation and tremor reduction support complex ESD and NOTES procedures. Meanwhile, 4K/8K towers spur replacement demand among hospitals aiming to meet AI-module image-quality minima. Accessories enjoy steady pull-through, sustaining margin even as tower pricing faces NHI pressure. Digital Twin integration promises pre-operative simulation that could shorten procedure time and support outcome auditing.

Robot systems command premium pricing, yet leasing models target ASCs eager for differentiation. Capsule devices gain urban traction due to patient preference for non-invasive GI screening, though reimbursement coverage remains limited. Over the forecast, continual optical upgrades, robotics, and connected-care analytics keep this segment central to the Japan endoscopy devices market.

Gastroenterology contributes 60.35% of revenue, sustained by government screening that locks in high colonoscopy and ESD volumes. Urology, the fastest-advancing application, is growing at 11.7% CAGR as single-port robots enable scar-minimizing nephrectomies and prostatectomies. Orthopedics maintains a steady arthroscopy pipeline, while cardiology leverages intracardiac imaging for ablation guidance. ENT and gynecology climb modestly on the back of specialty scopes and the Dexter robot's laparoscopic hysterectomy feasibility.

The Japan endoscopy devices market share for gastroenterology is expected to remain dominant through 2031, but incremental revenue will increasingly stem from urology and crossover applications. Vendors thus prioritize modular platforms capable of multi-disciplinary use to maximize return on capital.

The Japan Endoscopy Devices Market Report is Segmented by Device Type (Endoscopes, Endoscopic Operative Devices, Visualization Equipment, and Accessories & Consumables), Application (Gastroenterology, Orthopedic Surgery, Cardiology, Urology, and More), Procedure Type (Diagnostic Endoscopy and Therapeutic Endoscopy), End User (Hospitals, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Olympus Corp.

- Fujifilm Holdings Corp.

- Hoya Corp. (Pentax Medical)

- Johnson & Johnson (Ethicon Endo-Surgery)

- Boston Scientific

- Medtronic

- Cook Group

- KARL STORZ SE

- Conmed

- Richard Wolf

- Machida Endoscope

- Aohua Endoscopy Co., Ltd.

- Taewoong Medical

- SonoScape Medical Corp.

- Smiths Group

- Stryker

- Intuitive Surgical

- Nipro Endo Inc.

- Arthrex

- Cantel Medical (Jazz ALPHA)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Universal healthcare coverage and favorable reimbursement for advanced endoscopic procedures

- 4.2.2 Government-led gastric & colorectal cancer screening mandates elevating procedure volumes

- 4.2.3 Expansion of ambulatory surgical centers boosting demand for high-throughput endoscopy systems

- 4.2.4 Integration of AI-enabled CADe/CADx modules driving upgrade cycles of visualization platforms

- 4.2.5 Rising prevalence of lifestyle-linked GI disorders increasing therapeutic endoscopy adoption

- 4.3 Market Restraints

- 4.3.1 High upfront capital cost and NHI price controls limiting equipment ROI

- 4.3.2 Shortage of certified endoscopists and nursing staff constraining procedural capacity

- 4.3.3 Environmental and cost concerns over single-use scopes temper adoption rates

- 4.4 Regulatory Outlook

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device Type

- 5.1.1 Endoscopes

- 5.1.1.1 Rigid Endoscope

- 5.1.1.2 Flexible Endoscope

- 5.1.1.3 Capsule Endoscope

- 5.1.1.4 Robot-assisted Endoscope

- 5.1.2 Endoscopic Operative Devices

- 5.1.3 Visualization Equipment

- 5.1.3.1 Endoscopic Camera

- 5.1.3.2 SD Visualization System

- 5.1.3.3 HD Visualization System

- 5.1.3.4 4K/8K UHD Visualization System

- 5.1.4 Accessories & Consumables

- 5.1.1 Endoscopes

- 5.2 By Application

- 5.2.1 Gastroenterology

- 5.2.2 Orthopedic Surgery

- 5.2.3 Cardiology

- 5.2.4 ENT Surgery

- 5.2.5 Gynecology

- 5.2.6 Urology

- 5.3 By Procedure Type

- 5.3.1 Diagnostic Endoscopy

- 5.3.2 Therapeutic Endoscopy

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers (ASCs)

- 5.4.3 Specialty Clinics

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Olympus Corp.

- 6.3.2 Fujifilm Holdings Corp.

- 6.3.3 Hoya Corp. (Pentax Medical)

- 6.3.4 Johnson & Johnson (Ethicon Endo-Surgery)

- 6.3.5 Boston Scientific Corp.

- 6.3.6 Medtronic plc

- 6.3.7 Cook Group Inc.

- 6.3.8 KARL STORZ SE

- 6.3.9 Conmed Corp.

- 6.3.10 Richard Wolf GmbH

- 6.3.11 Machida Endoscope Co., Ltd.

- 6.3.12 Aohua Endoscopy Co., Ltd.

- 6.3.13 Taewoong Medical Co., Ltd.

- 6.3.14 SonoScape Medical Corp.

- 6.3.15 Smith & Nephew plc

- 6.3.16 Stryker Corp.

- 6.3.17 Intuitive Surgical Inc.

- 6.3.18 Nipro Endo Inc.

- 6.3.19 Arthrex Inc.

- 6.3.20 Cantel Medical (Jazz ALPHA)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment