PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852013

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852013

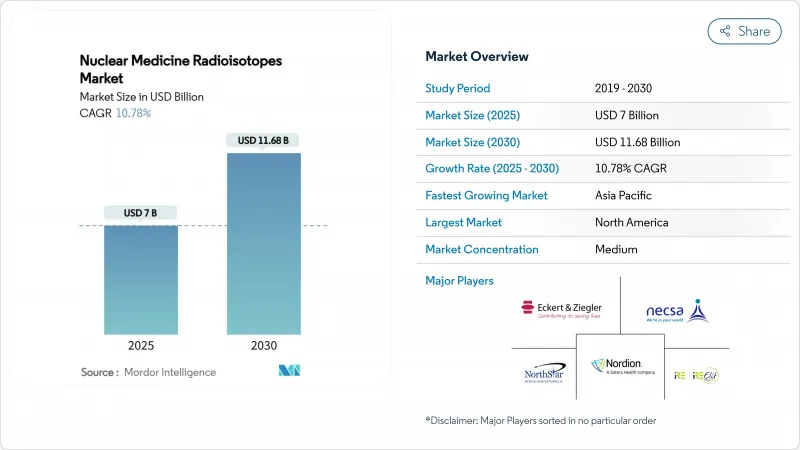

Nuclear Medicine Radioisotopes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The nuclear medicine radioisotopes market size reached USD 7 billion in 2025 and is forecast to climb to USD 11.68 billion by 2030, reflecting a 10.78% CAGR.

Growth momentum flows from rising cancer prevalence, expanding cardiology imaging volumes, and supply-chain shifts toward low-enriched-uranium (LEU) and cyclotron-based production. Diagnostic radioisotopes retain an 86.70% revenue lead as technetium-99m, fluorine-18, and gallium-68 anchor routine SPECT and PET imaging. Therapeutic isotopes, led by lutetium-177 and breakthrough alpha emitters such as actinium-225 and lead-212, accelerate on the back of regulatory fast-tracking and compelling clinical data. Cardiovascular adoption of flurpiridaz F-18 boosts PET penetration, while oncology theranostics capture investment and clinical enthusiasm. Regionally, North America commands 42.23% revenue on the strength of advanced healthcare infrastructure and a supportive regulatory climate; Asia-Pacific, however, exhibits the highest growth potential thanks to aggressive cyclotron roll-outs and expanding patient access.

Global Nuclear Medicine Radioisotopes Market Trends and Insights

Rising Prevalence of Cancer Requiring Theranostic Isotopes

Global oncology caseloads are projected to surge 60% by 2030, intensifying demand for isotopes that enable image-guided, targeted therapy. Lutetium-177 PSMA therapy posts 49.5% objective responses in metastatic prostate cancer and maintains favorable safety profiles compared with chemotherapy. The U.S. Food and Drug Administration designated 212Pb-DOTAMTATE as a breakthrough for gastroenteropancreatic neuroendocrine tumors following 62.5% response rates, underscoring alpha-emitter momentum.

Growing Adoption of SPECT & PET Imaging in Cardiology

Cardiology remains the largest application by volume as aging demographics elevate myocardial perfusion imaging needs. The clearance of flurpiridaz F-18 removes technetium-99m dependency while providing superior PET image quality and workflow benefits. Cyclotron-based 18F production, now supplying 95% of PET tracers, supports daily throughput increases and supply resilience.

Regulatory Fast-Tracking of Alpha Emitters for Targeted Therapy

Breakthrough and priority-review pathways in the U.S. and Europe compress time-to-market for alpha-emitting radiopharmaceuticals. Harmonized European Medicines Agency guidelines and evolving Asian frameworks improve cross-border development efficiency.

Other drivers and restraints analyzed in the detailed report include:

- Informed Patients, Evolving Markets: The Awareness Effect

- Supply-Chain Shift to LEU-Based Mo-99 Mitigating Shortages

- Short Half-Life Logistics & Waste Challenges

- Aging Reactor Fleet Limiting Isotope Output

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Diagnostic isotopes held an 86.70% nuclear medicine radioisotopes market share in 2024, underpinned by technetium-99m's ubiquity. Fluorine-18 and gallium-68 support PET's rapid expansion, particularly in oncology staging and cardiology perfusion studies. Therapeutic radioisotopes record the swiftest 11.45% CAGR as oncologists embrace lutetium-177 and alpha emitters for resistant cancers. The nuclear medicine radioisotopes market size for therapeutic agents is forecast to double between 2025 and 2030. Clinical data for yttrium-90 microspheres in hepatocellular carcinoma and iodine-131 in differentiated thyroid cancer reinforce radiopharmaceutical acceptance.

Advancing alpha-emitter pipelines lift long-term growth prospects. Actinium-225 generates high-linear-energy-transfer cytotoxicity with minimal collateral tissue damage, though production remains capacity-limited. Lead-212 generator breakthroughs promise broader accessibility and cost reduction. Regulatory bodies require stringent manufacturing controls, elevating investment needs but safeguarding patient safety.

Cardiology represented 31.45% revenue in 2024 on the back of entrenched SPECT protocols and emerging PET workflows. PET myocardial perfusion delivers higher diagnostic accuracy, shortened protocols, and superior attenuation correction, factors fueling conversion. Oncology, however, is projected to overtake cardiology mid-decade on an 11.78% CAGR as theranostics proliferate. The nuclear medicine radioisotopes market size for oncology indications is projected to reach USD 6.1 billion by 2030. PSMA-targeted imaging and therapy in prostate cancer and somatostatin receptor applications in neuroendocrine tumors showcase outcome improvements and quality-of-life gains.

Neurology and thyroid applications preserve niche demand. PET amyloid imaging expands slowly alongside disease-modifying Alzheimer's drugs, whereas iodine-123 and iodine-131 retain relevance in thyroid diagnostics and ablation therapy respectively.

The Nuclear Medicine Radioisotopes Market Report is Segmented by Type (Diagnostic Radioisotopes [Technetium-99m, Fluorine-18, and More], Therapeutic Radioisotopes [Iodine-131, Lutetium-177, and More]), Application (Oncology, Cardiology, and More), Source (Reactor-Produced Isotopes, and More), End-User (Hospitals, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 42.23% of 2024 revenue, anchored by roughly USD 2.43 billion U.S. demand and an ecosystem of cyclotrons, reactors, and radiopharmacies. Domestic LEU Mo-99 facilities under construction aim to eliminate reliance on aging foreign reactors and shield the region from supply disruptions. Canada, historically a major exporter via the Chalk River reactor, now invests in small modular reactor research and cyclotron upgrades to retain competitiveness. Mexico broadens nuclear medicine accessibility through public-private partnerships and cross-border isotope logistics.

Europe captured 28.15% share with Belgium, the Netherlands, France, and Germany serving as continental production hubs. France's Orano Med lead-212 plant targets 10,000 annual doses by 2025, positioning Europe at the forefront of alpha-emitter commercialization. Germany's dense network of 42 medical cyclotrons supplies regional PET needs, while the United Kingdom's Project Arthur seeks domestic Mo-99 coverage by 2030 to insulate health services from shortages.

Asia-Pacific posts the fastest 12.04% CAGR, led by rapid cyclotron deployment in China and India. China's 1,200 nuclear medicine departments handled 3.9 million procedures in 2024, with government plans to double capacity by 2035. India's 300-plus centers leverage Bhabha Atomic Research Centre support for reactor and cyclotron isotope production. South Korea's move to domestically produce actinium-225 and Australia's USD 392.2 million 2033 market projection illustrate widening regional opportunity circles. Japan partners with SHINE Technologies to secure lutetium-177 supply, ensuring continuity for prostate cancer therapy.

Latin America and the Middle East & Africa remain nascent but demonstrate consistent infrastructure investments. Brazil upgrades cyclotron installations in Sao Paulo, while Saudi Arabia funds theranostic centers under Vision 2030 health strategies.

- Curium Pharma

- Cardinal Health

- GE Healthcare

- Siemens Healthineers (PETNET)

- Lantheus Holdings

- Advanced Accelerator Applications (AAA)

- Eckert & Ziegler Radiopharma

- Nordion

- Jubilant Radiopharma

- IBA Radiopharma Solutions

- SHINE Technologies

- NorthStar Medical Radioisotopes

- BWXT Medical

- Isotopia Molecular Imaging

- ITM Isotope Technologies Munich

- Telix Pharmaceuticals

- Cyclotek

- NTP Radioisotopes

- Nusano

- Orano Med

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising prevalence of cancer requiring theranostic isotopes

- 4.2.2 Growing adoption of SPECT & PET imaging in cardiology

- 4.2.3 Supply-chain shift to LEU-based Mo-99 mitigating shortages

- 4.2.4 Regulatory fast-tracking of alpha-emitters for targeted therapy

- 4.2.5 Expansion of cyclotron networks in emerging economies

- 4.2.6 Rise of theranostic isotope pairings (Ga-68/Lu-177, etc.)

- 4.3 Market Restraints

- 4.3.1 Short half-life logistics & waste challenges

- 4.3.2 Aging reactor fleet limiting isotope output

- 4.3.3 High CAPEX of cyclotrons in developing regions

- 4.3.4 Escalating radiation-safety compliance costs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type (Value)

- 5.1.1 Diagnostic Radioisotopes

- 5.1.1.1 Technetium-99m (Tc-99m)

- 5.1.1.2 Fluorine-18 (F-18)

- 5.1.1.3 Iodine-123 (I-123)

- 5.1.1.4 Others

- 5.1.2 Therapeutic Radioisotopes

- 5.1.2.1 Iodine-131

- 5.1.2.2 Lutetium-177

- 5.1.2.3 Yttrium-90

- 5.1.2.4 Others

- 5.1.1 Diagnostic Radioisotopes

- 5.2 By Application (Value)

- 5.2.1 Oncology

- 5.2.2 Cardiology

- 5.2.3 Neurology

- 5.2.4 Thyroid Disorders

- 5.2.5 Others

- 5.3 By Source (Value)

- 5.3.1 Reactor-produced Isotopes

- 5.3.2 Cyclotron-produced Isotopes

- 5.3.3 Generator-produced Isotopes

- 5.4 By End-user (Value)

- 5.4.1 Hospitals

- 5.4.2 Diagnostic Imaging Centers

- 5.4.3 Academic & Research Institutes

- 5.4.4 Pharmaceutical & Biotechnology Companies

- 5.5 By Geography (Value)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Curium

- 6.3.2 Cardinal Health

- 6.3.3 GE HealthCare

- 6.3.4 Siemens Healthineers (PETNET)

- 6.3.5 Lantheus Holdings

- 6.3.6 Advanced Accelerator Applications (AAA)

- 6.3.7 Eckert & Ziegler Radiopharma

- 6.3.8 Nordion

- 6.3.9 Jubilant Radiopharma

- 6.3.10 IBA Radiopharma Solutions

- 6.3.11 SHINE Technologies

- 6.3.12 NorthStar Medical Radioisotopes

- 6.3.13 BWXT Medical

- 6.3.14 Isotopia Molecular Imaging

- 6.3.15 ITM Isotope Technologies Munich

- 6.3.16 Telix Pharmaceuticals

- 6.3.17 Cyclotek

- 6.3.18 NTP Radioisotopes

- 6.3.19 Nusano

- 6.3.20 Orano Med

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment