PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852015

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852015

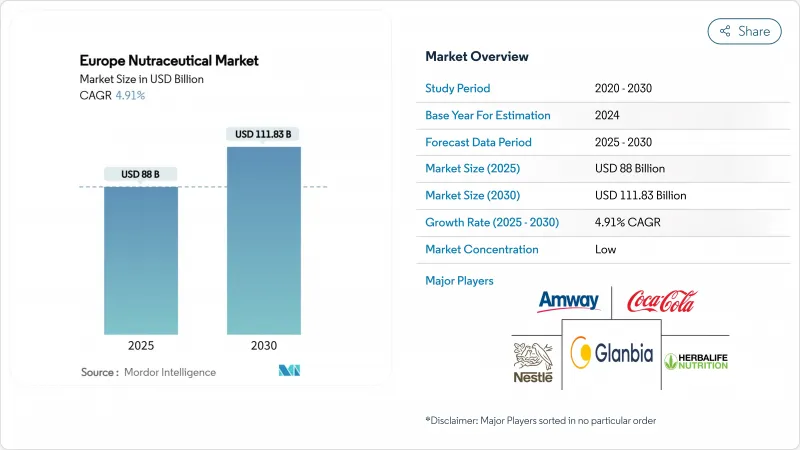

Europe Nutraceutical - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The European nutraceutical market is valued at USD 88 billion in 2025 and is expected to grow to USD 111.83 billion by 2030, with a CAGR of 4.91% during the forecast period.

This growth is driven by increasing spending on preventive healthcare, supportive policies for functional nutrition. Rising obesity rates and the related economic costs are pushing the market toward evidence-based solutions to delay the onset of chronic diseases. Among product types, functional foods held the largest market share, while dietary supplements are expected to grow the fastest. In terms of source, plant-based ingredients generated the highest revenue in 2024, while microbial-based alternatives are expected to grow rapidly. In terms of distribution channels, supermarkets/hypermarkets accounted for the largest market share, but online retail stores are projected to grow significantly. In terms of geography, Germany led the market, while the United Kingdom is expected to record the highest CAGR by 2030. The market remains fragmented, with agile companies using direct-to-consumer models to target specific health needs, while established food and pharmaceutical companies such as Glanbia PLC, Amway Corp., and others expand their clinical-claim portfolios to maintain their market position.

Europe Nutraceutical Market Trends and Insights

Aging population boosting functional intake

Europe's aging population is increasing the demand for nutraceuticals that support cognitive health, bone strength, and heart health. As of January 2024, Europe's overall population was estimated at 449.3 million, with over 21.6% aged 65 and older, according to the European Union. With 1 in 6 Europeans dying from noncommunicable diseases before the age of 70, as per PubMed Central, as of May 2025, policymakers are encouraging preventive nutrition through subsidies to lower long-term healthcare costs. This has led to a rise in products like omega-3 supplements for cholesterol control and collagen peptides for joint health, aimed at seniors focused on staying active as they age. Recent product launches in Europe have introduced advanced formulations that combine these functional ingredients to address the specific needs of older adults. Companies focusing on senior health in their product development benefit from supportive policies, such as VAT reductions on medically targeted supplements and faster European Food Safety Authority (EFSA) approvals for health claims related to aging.

Rising consumer focus on preventive health and wellness nutrition

The European nutraceutical market is growing as more people focus on preventive health and wellness. This shift has increased demand for products that help prevent chronic diseases and support overall health. Consumers are looking for supplements and functional foods that boost immunity, improve digestion, increase energy, and promote well-being. According to the World Health Organization, by 2025, 8.9 million more people in Germany are expected to experience better health, reflecting a broader trend of health awareness across Europe. At Vitafoods Europe 2024, a leading industry event, companies showcased innovative products to meet these needs. For example, Evonik launched AvailOm(R), an omega-3 powder with Boswellia extract for joint health, and IN VIVO BIOTICS(TM), a synbiotic solution to enhance gut health and immunity. These developments highlight the market's focus on creating effective and convenient nutraceutical products that align with the growing interest in preventive health.

Stringent European Food Safety Authority (EFSA) health-claim validation processes

The strict health-claim approval process by the European Food Safety Authority (EFSA) creates significant hurdles for the European nutraceutical market. Companies must undergo a lengthy approval process, often taking 3 to 5 years, which includes conducting expensive clinical trials to validate health claims. The updated European Regulation 2015/2283, effective from 2025, has introduced stricter rules, requiring detailed documentation of production processes. This has further extended approval timelines and increased the complexity of bringing new products to market. As a result, larger multinational companies with dedicated regulatory teams are better positioned to navigate these challenges. While the market continues to grow, the pace of innovation has slowed. Each time the European Food Safety Authority (EFSA) introduces new rules or updates existing ones, it creates uncertainty for product developers, making it harder for companies to plan and launch new products.

Other drivers and restraints analyzed in the detailed report include:

- Obesity and weight-management concerns

- Rising demand for clean-label and natural products

- High product development and compliance costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Functional Foods lead the European nutraceutical market in 2024, holding a 36.70% share. The popularity of fortified cereals, probiotic dairy drinks, and protein-enriched bakery products drives this dominance. These items benefit from strong visibility in supermarkets, reduced sugar content, and high consumer loyalty. Fiber-fortified breakfast items and slow-digesting proteins remain household staples, while confectionery brands include plant sterols and omega-3s to cater to healthier snacking trends. Lactose-free specialty dairy drinks with probiotics further strengthen their position by addressing digestive health needs across all age groups.

Dietary Supplements are expected to grow the fastest, with a 6.78% CAGR through 2030, significantly contributing to the European nutraceutical market size during the forecast period. This growth is fueled by precise dosing, tele-nutrition services, and condition-specific products like enzyme blends for digestion or botanicals for menopause relief. Personalized daily sachets improve adherence and customer retention, while clean-label sports-nutrition capsules attract a broader audience beyond athletes. As e-pharmacy regulations tighten in the region, brands offering clinically backed products in convenient formats are well-positioned to gain market share in both physical and online stores.

The Europe Nutraceutical Market is Segmented by Product Type (Functional Foods, Functional Beverages, and More), Source (Plant Based, Animal Based, and More), Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, and More), and Geography (United Kingdom, Germany, France, Italy, Spain, Netherlands, Sweden, Poland, Switzerland, Russia, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Nestle S.A.

- Danone S.A.

- Vitabiotics Ltd.

- Bayer AG

- Glanbia PLC

- NTP Biotech

- Amway Corp.

- The Coca-Cola Company

- Red Bull GmbH

- General Mills Inc.

- DSM-Firmenich

- Archer-Daniels-Midland Company

- Gruppo Farmaimpresa SRL

- Biofarma Group

- BASF SE

- Abbott Laboratories

- Lonza Group

- Rain Nutrience Ltd.

- G&G Vitamins

- Herbalife Nutrition Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising consumer focus on preventive health and wellness nutrition

- 4.2.2 Ageing population boosting functional intake

- 4.2.3 Rising demand for clean-label and natural products

- 4.2.4 High sports and fitness participation rates

- 4.2.5 Obesity and weight management concerns

- 4.2.6 Integration with public health programs

- 4.3 Market Restraints

- 4.3.1 Stringent European Food Safety Authority (EFSA) health-claim validation processes

- 4.3.2 High product development and compliance costs

- 4.3.3 Consumer backlash against ultra-processed 'health' foods

- 4.3.4 Counterfeit and low-quality products online

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Functional Foods

- 5.1.1.1 Breakfast Cereals

- 5.1.1.2 Bakery and Confectionery

- 5.1.1.3 Snacks

- 5.1.1.4 Dairy Products

- 5.1.1.5 Other Functional Foods

- 5.1.2 Functional Beverages

- 5.1.2.1 Energy Drinks

- 5.1.2.2 Sports Drinks

- 5.1.2.3 Fortified Juices

- 5.1.2.4 Other Functional Beverages

- 5.1.3 Dietary Supplements

- 5.1.3.1 Vitamins and Minerals

- 5.1.3.2 Botanicals

- 5.1.3.3 Enzymes

- 5.1.3.4 Omega

- 5.1.3.5 Other Dietary Supplements

- 5.1.1 Functional Foods

- 5.2 By Source

- 5.2.1 Plant Based

- 5.2.2 Animal Based

- 5.2.3 Microbial Based

- 5.2.4 Others

- 5.3 By Distribution Channel

- 5.3.1 Supermarkets / Hypermarkets

- 5.3.2 Convenience Stores

- 5.3.3 Pharmacies and Drug Stores

- 5.3.4 Online Retail Stores

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Netherlands

- 5.4.7 Sweden

- 5.4.8 Poland

- 5.4.9 Switzerland

- 5.4.10 Russia

- 5.4.11 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Nestle S.A.

- 6.4.2 Danone S.A.

- 6.4.3 Vitabiotics Ltd.

- 6.4.4 Bayer AG

- 6.4.5 Glanbia PLC

- 6.4.6 NTP Biotech

- 6.4.7 Amway Corp.

- 6.4.8 The Coca-Cola Company

- 6.4.9 Red Bull GmbH

- 6.4.10 General Mills Inc.

- 6.4.11 DSM-Firmenich

- 6.4.12 Archer-Daniels-Midland Company

- 6.4.13 Gruppo Farmaimpresa SRL

- 6.4.14 Biofarma Group

- 6.4.15 BASF SE

- 6.4.16 Abbott Laboratories

- 6.4.17 Lonza Group

- 6.4.18 Rain Nutrience Ltd.

- 6.4.19 G&G Vitamins

- 6.4.20 Herbalife Nutrition Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK