PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910464

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910464

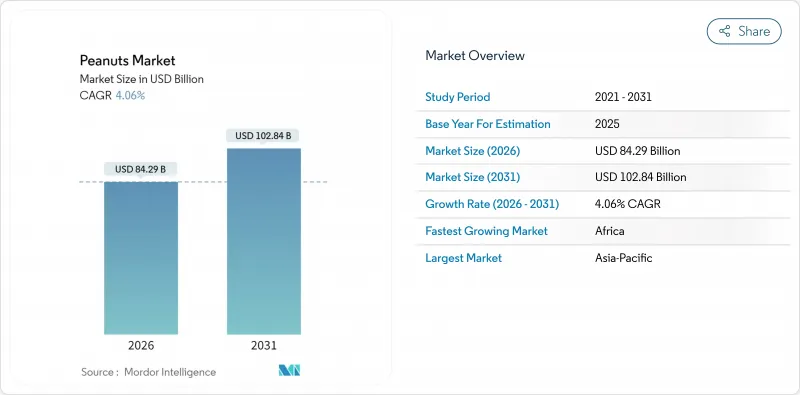

Peanuts - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The peanut market was valued at USD 81 billion in 2025 and estimated to grow from USD 84.29 billion in 2026 to reach USD 102.84 billion by 2031, at a CAGR of 4.06% during the forecast period (2026-2031).

This stable expansion reflects resilient supply chains, innovations in processing, and the steady pivot toward plant-based proteins that position the peanut market for continued growth. Large-scale processing upgrades, blockchain-enabled traceability, and shell-upcycling projects are broadening end-use applications while helping producers defend margins against climate-driven cost pressures. Asia-Pacific maintains the strongest demand pull, South Africa delivers the sharpest regional acceleration, and sustained U.S. yield improvements anchor global export capacity. Competitive intensity remains moderate because no single supplier dominates every geography, enabling both multinationals and mid-tier processors to differentiate through sustainability credentials, flavor innovation, and specialty ingredients.

Global Peanuts Market Trends and Insights

Rising Demand for Plant-Based Proteins

Peanut flour delivers 35-55% protein plus 15% dietary fiber, giving manufacturers a clean-label ingredient suited for gluten-free foods and fortified beverages. Institutional research indicates feed formulations could absorb 700,000 metric tons annually, adding USD 437 million to producer sales while enriching eggs with unsaturated fats and beta-carotene. As flexitarian diets expand across Western economies, manufacturers are integrating peanut proteins into cereals, meal-replacement shakes, and sports nutrition lines, reinforcing a steady demand base for the peanut market.

Growth of Peanut-Based Snacking Formats

Retail sales of snack nuts hit USD 5.2 billion in 2024, even as volumes slipped 2.9%, signaling clear consumer willingness to pay premiums for flavor innovations and sustainable sourcing. Flavored peanuts, nutrition-rich trail mixes, and single-serve packs line convenience stores, positioning the peanut market to capture on-the-go spending despite inflationary pressure. KP Snacks' acquisition of Whole Earth underlines the push to revitalize the stalled nut-butter category, maintaining 43% household penetration in the United Kingdom. Similar portfolio moves are anticipated across continental Europe, where premium spreads and coated nut innovations are climbing shelf space.

Climate-Induced Yield Volatility

Modeling projects 20% yield losses for peanuts by 2100 under high-emission scenarios, with drought-prone belts in the U.S. Southeast already costing USD 50 million annually. Genomics-assisted breeding delivers drought-tolerant lines, yet commercialization windows stretch beyond immediate needs, keeping supply tight during prolonged heatwaves. Senegalese trials reveal CO2-fertilization could raise yields 19% in specific microclimates, highlighting heterogeneity that complicates global sourcing strategies. The development of high-throughput phenotyping methods is accelerating the breeding of stress-tolerant cultivars, though commercialization requires substantial investment and regulatory approval processes.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Peanut Processing Capacity

- Clean-Label Shift Boosting Peanut Flour Uptake

- Food-Safety Recalls (Aflatoxin)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Peanut Market Report is Segmented by Geography (North America, Europe, Asia-Pacific, South America, and More). The Report Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Export Analysis (Value and Volume), Import Analysis (Value and Volume), and Price Trend Analysis. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Geography Analysis

Asia-Pacific commands 52.18% of the peanut market share in 2025 on an annual production of 19,000 thousand metric tons, anchored by China at 36% global output. India's 7,100 thousand metric tons crop secures second place while urbanizing Southeast Asia scales snack-nut demand. Consumption growth inside China tightens export surpluses, occasionally firming global prices, while equipment modernization spreads unevenly across producer nations.

Africa and the Middle East deliver mixed patterns. Africa registers the fastest regional rise at 6.35% CAGR to 2031, aided by disease-resistant cultivars and new irrigation schemes. Turkey and Saudi Arabia grow import demand, though foreign-exchange swings and political tension can disrupt shipping timelines. The implementation of deforestation-free rules will reward certified suppliers, potentially redirecting flows away from low-compliance origins. Germany and France favor peanut butter and confectionery usage, while the United Kingdom sustains premium snack selections despite static volumes.

The United States exports a stable 25% of crop volume to Mexico, Canada, Europe, China, and Japan. Georgia's 53% share of national production offers shipping engagement but heightens regional weather risk. Canada and Mexico supplement supply while expanding roasted and confectionery categories. South America shows the fastest multi-country expansion, led by Argentina's dominance in raw-nut exports and Brazil's projected record crop of 832,300 metric tons, up 40.6%. Cordoba's cluster model integrates growers with crushers and port logistics, enhancing competitive landed costs. Chile remains a primary regional buyer, whereas Brazil bolsters domestic processing to serve snack and confectionery segments.

- Market Overview

- Market Drivers

- Market Restraints

- Regulatory Landscape

- Technological Outlook

- Value/Supply-Chain Analysis

- PESTEL Analysis

- List of Stakeholders

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for plant-based proteins

- 4.2.2 Growth of peanut-based snacking formats

- 4.2.3 Expansion of peanut processing capacity

- 4.2.4 Clean-label shift boosting peanut flour uptake

- 4.2.5 Blockchain-enabled origin tracing raising export premiums

- 4.2.6 Upcycling peanut shells into bioplastics

- 4.3 Market Restraints

- 4.3.1 Climate-induced yield volatility

- 4.3.2 Food-safety recalls (aflatoxin)

- 4.3.3 EU deforestation-free import rules tightening

- 4.3.4 Emerging allergy-labeling mandates in developing markets

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Value/Supply-Chain Analysis

- 4.7 PESTEL Analysis

5 Market Size and Growth Forecasts

- 5.1 By Geography (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis)

- 5.1.1 North America

- 5.1.1.1 United States

- 5.1.1.2 Canada

- 5.1.1.3 Mexico

- 5.1.2 South America

- 5.1.2.1 Brazil

- 5.1.2.2 Argentina

- 5.1.2.3 Chile

- 5.1.3 Europe

- 5.1.3.1 Germany

- 5.1.3.2 France

- 5.1.3.3 Italy

- 5.1.3.4 United Kingdom

- 5.1.4 Asia-Pacific

- 5.1.4.1 China

- 5.1.4.2 India

- 5.1.4.3 Japan

- 5.1.4.4 Australia

- 5.1.5 Middle East

- 5.1.5.1 Turkey

- 5.1.5.2 Saudi Arabia

- 5.1.6 Africa

- 5.1.6.1 South Africa

- 5.1.6.2 Kenya

- 5.1.6.3 Egypt

- 5.1.1 North America

6 Competitive Landscape

- 6.1 List of Stakeholders

- 6.1.1 Olam Group

- 6.1.2 Cargill, Incorporated

- 6.1.3 ADM

- 6.1.4 Wilmar International Limited

- 6.1.5 Birdsong Peanuts

- 6.1.6 Shree Padm Agri Brokers

- 6.1.7 Qingdao Changshou Food Co., Ltd.

- 6.1.8 Shandong Jinfeng Group

- 6.1.9 The Kraft Heinz Company

- 6.1.10 Hormel Foods Corporation

7 Market Opportunities and Future Outlook