PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852063

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852063

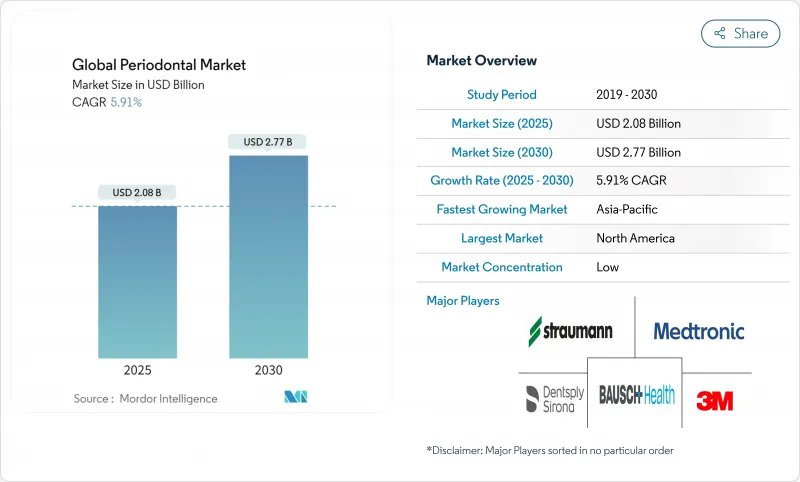

Global Periodontal - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The periodontal treatment market size stands at USD 2.08 billion in 2025 and is forecast to reach USD 2.77 billion by 2030, expanding at a 5.91% CAGR.

Advancing regenerative devices, rising dental-insurance penetration, and a pronounced shift toward minimally invasive care are accelerating demand. An aging global population-with severe periodontitis cases projected to climb from 1 billion in 2021 to 1.56 billion by 2050-anchors long-term procedure volumes. The periodontal treatment market is also benefitting from cosmetic dentistry's social-media-driven boom, stronger links between oral and systemic health in reimbursement policy, and continuous product launches that shorten chair time. Conversely, high treatment costs in emerging economies and shortages of specialized clinicians in rural areas restrain growth momentum.

Global Periodontal Market Trends and Insights

Rising prevalence of periodontal diseases among ageing populations

Rapid population ageing is elevating disease burden: nearly 70% of adults over 65 in high-income economies exhibit some periodontitis, while senescent cells intensify inflammation that standard debridement alone cannot resolve. Healthcare systems are integrating periodontal screening into chronic-disease programmes, reinforcing a solid demand pipeline that sustains the periodontal treatment market over the long term.

Growing demand for cosmetic & aesthetic dentistry

Video-conferencing culture and social-media visibility have recalibrated patient expectations toward seamless function and facial harmony. Digital scanners and chairside 3-D printing enable clinicians to merge regenerative periodontal surgery with smile-design workflows, drawing younger cohorts into the periodotal treatment market. Insurers now reimburse aesthetic-linked periodontal procedures when systemic health benefits are documented, further widening the addressable base.

High treatment cost & limited reimbursement in emerging markets

In India only 5% of the population can afford advanced oral care; 80% have never visited a dentist, demonstrating a vast access gap. Import dependence inflates equipment prices, and private payment models dominate. Although local manufacturers are scaling, the affordability barrier continues to slow periodontal treatment market uptake across South and Southeast Asia.

Other drivers and restraints analyzed in the detailed report include:

- Technological shift toward minimally-invasive laser & regenerative therapies

- Expanding dental-insurance coverage in high-income economies

- Shortage of specialised periodontists in semi-urban & rural areas

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Equipment contributed 55.72% to the periodontal treatment market in 2024 as power-driven scalers, lasers, and CBCT imaging became standard for comprehensive care. Ongoing upgrades in piezoelectric systems and the rising penetration of diode lasers keep average selling prices resilient. Consumables, though smaller, are the fastest advancing slice at a 6.25% CAGR, propelled by regenerative membranes and nano-hydroxyapatite grafts that clinicians reorder frequently. The periodontal treatment market size for regenerative graft materials is set to expand steadily, supported by clinical proof of faster osseointegration.

The medication sub-segment is pivoting toward locally delivered antimicrobials, enabling sustained drug concentrations in periodontal pockets without systemic exposure. Together, these dynamics reinforce the periodontal treatment market trajectory as practices invest in both capital equipment and recurring consumables to stay competitive.

Gingivitis retained 46.98% share of the periodontal treatment market size in 2024 because routine prophylaxis addresses a broad patient base. Public-health campaigns and employer-sponsored dental wellness have increased early detection, keeping this segment sizeable. Aggressive periodontitis, although smaller, is set to post a 6.64% CAGR to 2030 as improved genetic and biomarker diagnostics allow clinicians to intervene earlier in rapid-destructive cases.

Chronic periodontitis continues to climb with longevity, while necrotizing and medication-related conditions create specialized niches that stimulate innovation in immunomodulatory adjuncts. These multiple disease pathways make the periodontal treatment market a diversified field that rewards flexible product portfolios.

The Periodontal Treatment Market Report is Segmented by Product (Equipment, Consumables, Medication), Disease (Gingivitis, Chronic Periodontitis, Aggressive Periodontitis, Other Diseases), Treatment (Non-Surgical Treatment, Surgical Treatment), End User (Hospitals, Dental Clinics, Academic & Research Institutes), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 42.23% of 2024 turnover as Medicaid expansions and private-insurance upgrades broadened adult periodontal benefits. Yet provider shortages outside major metros limit penetration speed, prompting mobile clinics and teledentistry pilots. The periodontal treatment market remains robust across Canada, where federal coverage launched in 2024 underwrites comprehensive periodontal services.

Asia-Pacific is the primary growth engine at 7.94% CAGR through 2030. China's implant boom and digitally enabled peri-implant maintenance propel equipment upgrades, while domestic manufacturing-exemplified by Laxmi Dental's graft production-shrinks import costs for India. Medical-tourism flows to Thailand and South Korea further swell the periodontal treatment market, supported by governmental health-check subsidies that bundle periodontal screening into inbound packages.

Europe benefits from universal insurance and stringent device regulations that safeguard clinical standards. Germany and Switzerland pioneer biomaterial development, with Geistlich's collagen membranes gaining traction for difficult defects. Southern European economies experience faster growth as EU recovery funds modernize clinics. Latin America and the Middle East show steady demand, especially in urban centers where premium cosmetic dentistry resonates with aspirational consumers, although currency volatility tempers the periodontal treatment market's potential in the near term.

- Dentsply Sirona

- Envista Holdings (Nobel Biocare, KaVo Kerr)

- Straumann Group

- 3M

- Henry Schein

- BIOLASE Inc.

- J. Morita Corp.

- Zimmer Biomet

- Geistlich Pharma

- BEGO GmbH

- A-dec

- NSK Nakanishi

- Ultradent Products

- Keystone Dental Group

- Millennium Dental Technologies

- Brasseler USA

- Parkell

- DentalEZ

- AMD Lasers

- Botiss Biomaterials

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising prevalence of periodontal diseases among ageing populations

- 4.2.2 Growing demand for cosmetic & aesthetic dentistry

- 4.2.3 Technological shift toward minimally-invasive laser & regenerative therapies

- 4.2.4 Expanding dental-insurance coverage in high-income economies

- 4.2.5 Home-use photodynamic devices improving patient compliance

- 4.2.6 AI-driven risk-analytics inside DSOs enabling preventive outreach

- 4.3 Market Restraints

- 4.3.1 High treatment cost & limited reimbursement in emerging markets

- 4.3.2 Shortage of specialised periodontists in semi-urban & rural areas

- 4.3.3 Post-COVID clinic focus on higher-margin restorative work

- 4.3.4 Regulatory uncertainty for nano-biomaterials

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product (Value, USD million)

- 5.1.1 Equipment

- 5.1.1.1 Power-Driven Scalers & Ultrasonic Units

- 5.1.1.2 Dental Lasers

- 5.1.1.3 CBCT & Imaging Systems

- 5.1.2 Consumables

- 5.1.2.1 Sutures & Hemostats

- 5.1.2.2 Barrier Membranes

- 5.1.2.3 Regenerative Bone-Graft Substitutes

- 5.1.3 Medication

- 5.1.3.1 Topical Antibiotics & Antimicrobials

- 5.1.3.2 Systemic Antibiotics

- 5.1.1 Equipment

- 5.2 By Disease (Value, USD million)

- 5.2.1 Gingivitis

- 5.2.1.1 Acute Gingivitis

- 5.2.1.2 Recurrent Gingivitis

- 5.2.1.3 Chronic Gingivitis

- 5.2.2 Chronic Periodontitis

- 5.2.3 Aggressive Periodontitis

- 5.2.4 Other Diseases

- 5.2.1 Gingivitis

- 5.3 By Treatment (Value, USD million)

- 5.3.1 Non-Surgical Treatment

- 5.3.1.1 Scaling

- 5.3.1.2 Root Planing

- 5.3.1.3 Medication Therapy

- 5.3.1.3.1 Topical Therapy

- 5.3.1.3.2 Systemic Therapy

- 5.3.2 Surgical Treatment

- 5.3.2.1 Flap Surgery / Pocket-Reduction Therapy

- 5.3.2.2 Soft-Tissue Graft

- 5.3.2.3 Bone Grafting

- 5.3.2.4 Guided Tissue Regeneration

- 5.3.2.5 Other Surgical Treatments

- 5.3.1 Non-Surgical Treatment

- 5.4 By End User (Value, USD million)

- 5.4.1 Hospitals

- 5.4.2 Dental Clinics

- 5.4.3 Academic & Research Institutes

- 5.5 By Geography (Value, USD million)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Dentsply Sirona

- 6.3.2 Envista Holdings (Nobel Biocare, KaVo Kerr)

- 6.3.3 Straumann Group

- 6.3.4 3M Company

- 6.3.5 Henry Schein Inc.

- 6.3.6 BIOLASE Inc.

- 6.3.7 J. Morita Corp.

- 6.3.8 Zimmer Biomet

- 6.3.9 Geistlich Pharma

- 6.3.10 BEGO GmbH

- 6.3.11 A-dec Inc.

- 6.3.12 NSK Nakanishi

- 6.3.13 Ultradent Products

- 6.3.14 Keystone Dental Group

- 6.3.15 Millennium Dental Technologies

- 6.3.16 Brasseler USA

- 6.3.17 Parkell Inc.

- 6.3.18 DentalEZ Inc.

- 6.3.19 AMD Lasers

- 6.3.20 Botiss Biomaterials

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment