PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852077

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852077

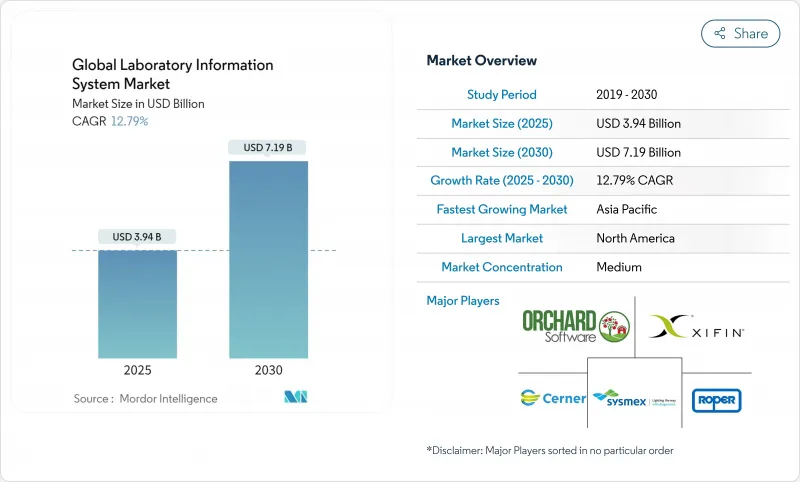

Global Laboratory Information System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The laboratory information system market is valued at USD 3.19 billion in 2025 and is forecast to climb to USD 7.19 billion by 2030, advancing at a 12.79% CAGR.

Growth rests on larger test volumes generated by aging populations, fast-maturing cloud architectures that cut capital barriers, and tightening interoperability mandates that pull laboratories into broader clinical data networks. Software remains the anchor purchase, yet demand leans toward expert services that shorten time-to-value, while AI modules move from pilot to production in result validation, inventory control, and predictive maintenance. Laboratories also recalibrate deployment strategies: most large institutions still run on-premise systems, but small and midsize facilities pivot to software-as-a-service models that open enterprise-grade features without server investments. Geographic momentum shifts as Asia-Pacific adds new digital health budgets and leapfrogs legacy constraints, even while North America guards its lead through rigorous compliance rules and early AI adoption. Escalating cyberattacks underscore the need for zero-trust security layers that strengthen vendor selection criteria, and a wave of mergers-from diagnostics giants to cloud-native entrants-signals a race for scale, talent, and regulatory depth.

Global Laboratory Information System Market Trends and Insights

Rising Global Diagnostic Testing Volumes Driven by Aging Populations

World health systems process soaring test counts as the 65-plus demographic accelerates, lifting chronic disease panels and routine screenings. In the United States alone, laboratories handled more than 14 billion tests in 2024, and demographic projections indicate sustained expansion. Manual workflows cannot keep pace, so laboratories deploy modern LIS modules that automate specimen labeling, tracking, and multilayer result verification. AI engines now flag hemolysis or clot interference within seconds, releasing technologists for complex review. Rural clinics in China that adopted health kiosk networks saw patient visits jump 37.85% and medical revenue climb 54.03%, illustrating the multiplier effect once digital processes anchor community care .

Rapid Scale-up of Biobank Networks

Precision-medicine projects demand longitudinal biospecimen libraries, pushing biobank consortia to invest in configurable LIS platforms. These systems track consent, lineage, and chain-of-custody across distributed freezers while integrating with sequencing pipelines. Guy's and St Thomas' BioResource deployed Matrix Gemini to automate 500,000-plus samples and reclaimed 20% storage space through optimized location mapping. Vendors respond with biobank-ready modules that map sample derivatives, enforce ISO 20387 compliance, and export query-ready data to translational research teams.

High Total Cost of Ownership

Comprehensive LIS deployments frequently overrun initial budgets once data migration, validation, and user training surface. Full-scale projects can cross USD 60,000 in software fees and stretch 6-9 months, while annual licensing spans USD 3,000 to USD 250,000 depending on seats and modules. Smaller labs lacking internal IT teams bear integration consulting expenses that double headline price tags. New U.S. FDA rules for laboratory-developed tests from May 2025 introduce additional documentation and quality-system layers that inflate implementation timelines.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Uptake of Cloud/SaaS LIS That Lower Capital Outlays

- AI-Powered Workflow Automation Modules

- Strengthening Regulatory Mandates for Interoperability

- Escalating Cybersecurity & HIPAA/GDPR Liabilities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software maintained a 65.15% stake of the laboratory information system market in 2024, anchored by core modules that orchestrate specimen intake, analyzer interfaces, and compliance documentation. Implementation teams, however, observe that successful rollouts hinge on workflow redesign, driving services revenue to a 13.14% CAGR. The laboratory information system market size associated with integrated support bundles is projected to widen as labs outsource validation and post-go-live optimization. SaaS code bases speed version upgrades, yet they also spur demand for training contracts that upskill staff on quarterly releases. Vendors differentiate through consulting depth, interoperability mapping, and regulatory audit readiness, converting one-time license deals into recurring service pipelines.

Second, smaller facilities with lean headcount lean on managed services for server monitoring, patching, and cybersecurity hardening. Premium support tiers bundle 24/7 help desks and rapid interface tailoring as payer rules evolve, creating annuity revenue streams that offset cyclical license spending. With the FDA's 2025 LDT rule intensifying documentation duties, laboratories look for partners that supply pre-built SOP templates and e-signature workflows, ensuring continuous compliance while internal teams remain focused on quality control tasks.

On-premise deployments held 59.26% of the laboratory information system market share in 2024 as large hospitals safeguarded data sovereignty and leveraged sunk server investments. Yet cloud implementations record a 13.85% CAGR, signaling an inflection in buying patterns. The laboratory information system market size attributable to SaaS contracts is forecast to rise sharply as subscription models scale with test volumes rather than hardware cycles. Hybrid approaches emerge where sensitive personally identifiable information resides on-site, while analytics dashboards and long-term archives shift to vendor clouds.

Remote access needs borne out of pandemic restrictions tipped executive sentiment toward cloud reliability, and proof-of-concept pilots now demonstrate parity or superiority in uptime compared with on-premise clusters. SOC 2 Type II reports, HIPAA business-associate assurances, and regional data-residency zones address compliance teams' concerns. Over time, depreciation schedules and power-cost spikes further erode the economics of maintaining local data centers, accelerating the transition path for institutions planning next-generation smart-hospital blueprints.

The Report Covers Global Laboratory Information System Companies and It is Segmented by Component (Software and Service), Mode of Delivery (On-Premise, Cloud-Based, and Hybrid), Laboratory Type (Clinical Pathology Labs, Anatomic Pathology Labs, and More), End User (Hospital and Clinics and More), and Geography. The Market Provides the Value (in USD Million) for the Above Segments.

Geography Analysis

North America continued to dominate with 42.84% of the laboratory information system market share in 2024. The United States anchors this lead through strict CLIA oversight and robust payer incentives that reward digital quality metrics. Canada's single-payer initiatives inject funding into provincial lab modernizations, while Mexico's private-hospital chains adopt cloud platforms to bypass limited legacy IT staffing. The fallout from the 2024 Change Healthcare breach draws executive attention to cybersecurity hardening and vendor SOC 2 credentials. New FDA mandates for laboratory-developed tests, effective May 2025, push replacement cycles as older platforms lack the e-quality-management functions now required.

Asia-Pacific registers the fastest 14.38% CAGR, underwritten by government e-health roadmaps and expanding middle-class insurance coverage. India's National Digital Health Blueprint funnels investment into interoperable data platforms, and early pilots forecast a USD 25 billion digital-health economy by 2030. China's rural health kiosks prove that tele-pathology and remote result delivery can leapfrog brick-and-mortar constraints, driving cloud adoption among tier-3 county hospitals. South Korea's Samsung Medical Centre demonstrates smart-hospital orchestration where LIS, radiology, and pharmacy platforms align through FHIR exchanges, setting a regional benchmark copied by Singapore and Australia.

Europe shows steady though slower progression as GDPR dictates tight data-sovereignty controls that complicate extra-regional cloud hosting. Germany retains top regional share, while France accelerates oncology-focused sequencing labs benefiting from national genomics funding. The Middle East opens green-field hospital builds tied to Vision 2030 programs, embedding LIS from day one to meet Joint Commission accreditation. South America advances gradually; Brazil's private insurance market encourages lab consolidation, yet currency volatility and regulatory heterogeneity temper multicountry deployments. Across all regions, donor-funded public-health labs seek open-source or low-cost SaaS options that comply with WHO surveillance reporting, creating a secondary tier for value-oriented vendors.

- Clinisys (Roper)

- Oracle Health (Cerner Corporation)

- Epic Systems

- SCC Soft Computer, LLC

- Orchard Software

- Sysmex

- XIFIN

- CompuGroup Medical SE & Co. KGaA

- Cirdan Ltd.

- Dedalus Group S.p.A.

- Total Specific Solutions B.V

- Comp Pro Med, Inc

- Margy Tech Pvt. Ltd.

- Biosero

- Wavefront Software, Inc.

- LigoLab LLC

- Aspyra LLC

- LabWare, Inc.

- ClinLab, Inc.

- TELCOR, Inc.

- eLabNext B.V.

- CGM SCHUYLAB

- SoftTech Health LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Diagnostic Testing Volumes Driven By Aging Populations

- 4.2.2 Rapid Scale-Up Of Biobank Networks

- 4.2.3 Rapid Uptake Of Cloud/SaaS Lis That Lower Capital Outlays

- 4.2.4 AI-Powered Workflow Automation Modules

- 4.2.5 Strengthening Regulatory Mandates For Interoperability

- 4.2.6 Growth Of Cloud-Native LIS Start-Ups In Emerging Markets

- 4.3 Market Restraints

- 4.3.1 High Total Cost Of Ownership

- 4.3.2 Escalating Cybersecurity & HIPASS/GDPR Liabilities

- 4.3.3 Shortage Of LIS-Literate Lab Informaticians

- 4.3.4 Fragmented And Evolving Regulatory Requirements

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD Million)

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Stand-alone LIS

- 5.1.1.2 Integrated LIS / EHR-centric

- 5.1.1.3 SaaS LIS Platforms

- 5.1.2 Services

- 5.1.2.1 Implementation & Integration

- 5.1.2.2 Maintenance & Support

- 5.1.2.3 Training & Consulting

- 5.1.1 Software

- 5.2 By Mode of Delivery

- 5.2.1 On-premise

- 5.2.2 Cloud-based

- 5.2.3 Hybrid

- 5.3 By Laboratory Type

- 5.3.1 Clinical Pathology Labs

- 5.3.2 Anatomic Pathology Labs

- 5.3.3 Molecular Diagnostics Labs

- 5.3.4 Blood Banks & Biobanks

- 5.3.5 Other Specialized Labs

- 5.4 By End User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Laboratories

- 5.4.3 Academic & Research Institutes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Clinisys (Roper)

- 6.3.2 Oracle Health (Cerner Corporation)

- 6.3.3 Epic Systems Corporation

- 6.3.4 SCC Soft Computer, LLC

- 6.3.5 Orchard Software Corporation

- 6.3.6 Sysmex Corporation

- 6.3.7 XIFIN, Inc.

- 6.3.8 CompuGroup Medical SE & Co. KGaA

- 6.3.9 Cirdan Ltd.

- 6.3.10 Dedalus Group S.p.A.

- 6.3.11 Total Specific Solutions B.V

- 6.3.12 Comp Pro Med, Inc

- 6.3.13 Margy Tech Pvt. Ltd.

- 6.3.14 Biosero, Inc.

- 6.3.15 Wavefront Software, Inc.

- 6.3.16 LigoLab LLC

- 6.3.17 Aspyra LLC

- 6.3.18 LabWare, Inc.

- 6.3.19 ClinLab, Inc.

- 6.3.20 TELCOR, Inc.

- 6.3.21 eLabNext B.V.

- 6.3.22 CGM SCHUYLAB

- 6.3.23 SoftTech Health LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment