PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852081

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852081

Hyaluronic Acid Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

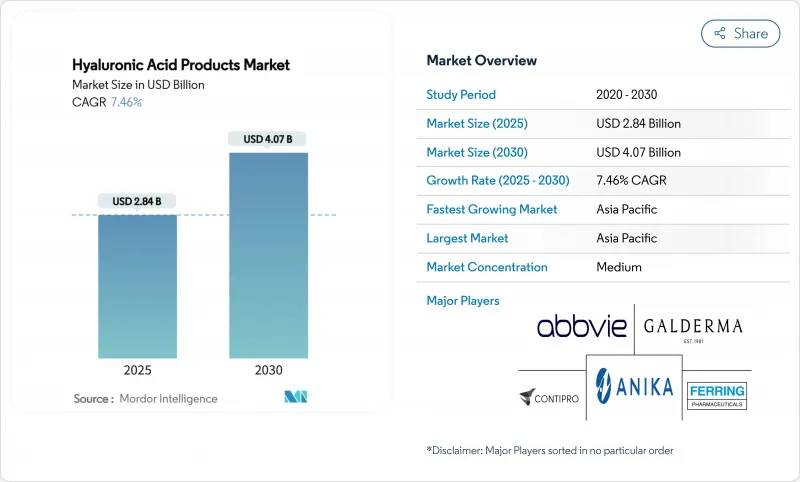

The hyaluronic acid products market size reached USD 2.84 billion in 2025 and is projected to attain USD 4.07 billion by 2030, translating to a 7.46% CAGR.

This upward trajectory is driven by the increasing integration of aesthetic medicine with therapeutic applications, a steady influx of regulatory approvals for advanced formulations, and a shift in production technologies favoring non-animal fermentation methods. Industry players are strategically aligning cosmetic and medical applications to diversify and expand their revenue streams. Simultaneously, healthcare professionals are increasingly adopting multi-molecular weight hyaluronic acid products, which are recognized for their enhanced ability to penetrate deeper skin layers and provide extended tissue retention. Strategic collaborations, such as L'Oreal's acquisition of a 10% stake in Galderma, highlight the intensifying competition among market participants to secure innovative assets and maintain a competitive edge. The Asia-Pacific region emerges as a key growth driver, leveraging its large-scale manufacturing capabilities and the rising demand from urban populations. Furthermore, regulatory authorities in the region have accelerated their review and approval processes, effectively reducing the time required for product commercialization and enabling faster market entry.

Global Hyaluronic Acid Products Market Trends and Insights

Rising demand for anti-aging solutions in skincare

Clinical studies have demonstrated that cross-linked hyaluronic acid injections effectively sustain fibroblast activation and collagen synthesis for up to a year, driving the market for scientifically validated anti-aging solutions. Shifting demographics are influencing demand trends, moving beyond traditional metrics of population aging. As of January 2024, the European Union reported a population of 449.3 million, with over 21.6% aged 65 and above. Key suppliers, such as DSM-Firmenich, have launched trinary molecular-weight product lines designed to target specific dermal depths, enabling premium pricing strategies. Growing consumer preference for minimally invasive treatments has led companies to invest in multi-weight serums that complement in-clinic injectable procedures. Radiofrequency-enhanced endogenous HA stimulation has achieved a 67.69% increase in natural HA levels within three months, positioning device-cosmetic hybrids as a lucrative growth opportunity. Furthermore, rising disposable incomes in emerging markets are driving demand for high-performance anti-aging solutions.

Growing use in aesthetic dermatology and cosmetic injections

The aesthetic dermatology market is transitioning toward precision medicine, emphasizing advanced molecular engineering and clinical applications of hyaluronic acid fillers. The hyaluronic acid products market is experiencing growth, driven by FDA approvals for temple hollowing fillers and RHA technologies that replicate natural facial movements. Product development now focuses on rheological properties, such as G-prime strength and cohesivity, to ensure long-lasting structural support. Galderma's Restylane SHAYPE exemplifies how next-generation gels meet these stringent performance criteria. Combination treatment protocols, with an 89% patient satisfaction rate, integrate multiple fillers in a single session to optimize aesthetic outcomes. These bundled services not only enhance practitioner revenue per visit but also increase product demand, accelerating market growth.

Allergic reactions and inflammation from consumption

A meta-analysis of 16 trials identified limited pain relief from intra-articular HA and highlighted systemic inflammatory markers, prompting healthcare providers to optimize patient selection strategies. FDA warnings regarding fillers contaminated with undisclosed diclofenac emphasized the critical need for enhanced supply chain oversight. In response, manufacturers like Contipro have invested in advanced endotoxin-removal filtration technologies to improve product purity. Additionally, personalized dosing algorithms are being developed to optimize efficacy and safety, supported by digital monitoring tools that track post-injection swelling and bruising. As surveillance systems evolve, real-world evidence will provide deeper insights into the actual incidence of adverse events, enabling data-driven evaluations of risk-benefit profiles to inform formulary decisions.

Other drivers and restraints analyzed in the detailed report include:

- Expansion in orthopedic applications

- Demand for non-animal and vegan sources of hyaluronic acid

- Regulatory challenges for oral HA supplements and claims

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2024, high-molecular products accounted for 46.44% of the hyaluronic acid market revenue, driven by their well-established applications in viscosupplementation and fillers. Meanwhile, ultra-low variants are gaining traction with an 8.45% CAGR, attributed to their superior dermal penetration and compatibility with nanoparticle carriers. Hybrid formulations, such as IBSA's NAHYCO-based complexes, combine high and low molecular weights to restore facial volume while maintaining effective spreadability. Crosslink chemistries now enable post-production weight adjustments, providing manufacturers with flexible tools to optimize viscosity and degradation rates. The competitive landscape is increasingly focused on patent portfolios that protect proprietary depolymerization and crosslinking technologies.

Emerging clinical data is shaping product selection strategies. Studies indicate that polymer concentration and crosslink type significantly influence injectability force, impacting physician preferences. Regulatory authorities are now requiring rheology data in technical submissions, adding complexity to compliance processes. Companies offering multi-weight kits empower practitioners to customize treatments on-site, improving inventory efficiency and reducing patient chair time. As low-weight products continue to penetrate drug delivery pipelines, molecular-weight segmentation is expected to converge across therapeutic and cosmetic applications, unlocking broader revenue opportunities.

The Global Hyaluronic Acid Market is Segmented by Molecular Weight (High Molecular Weight and Low Molecular Weight, Ultra Low Molecular Weight), Application (Dietary Supplements, Pharmaceutical Industry, and Cosmetics Industry); and by Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Geography Analysis

In 2024, the Asia-Pacific region accounted for 46.08% of global revenue and is projected to grow at a CAGR of 8.19% from 2025 to 2030. This growth is driven by cost-efficient fermentation capabilities and the rapid urban adoption of injectable aesthetics. China, serving as a manufacturing hub, leads in hyaluronic acid production for cosmetics. According to China Customs, the export value of personal care and cosmetic products from China reached USD 7.2 billion in 2024. Regional governments are supporting this growth through biotechnology incentives. For instance, South Korea increased its biomedical research and development funding by 15% for 2025, aiming to commercialize advanced HA derivatives. Bloomage Biotech exemplifies the region's shift from contract manufacturing to intellectual property-driven value creation, with over 520 patents and a supply network spanning more than 4,000 global brands. The competitive landscape is becoming more intense, as public disputes over labeling accuracy highlight stricter local regulatory oversight.

North America and Europe prioritize premium formulations supported by extensive clinical evidence. Regulatory changes, such as the FDA's drug reclassification proposal, create both challenges and opportunities for companies capable of managing lengthy trial processes. Products like Galderma's Restylane SHAYPE and AbbVie's JUVEDERM VOLUMA XC Temple demonstrate region-specific innovations designed to address unique anatomical needs. Strategic partnerships, such as the Galderma-L'Oreal collaboration, enable co-marketing and shared technological advancements. While compliance costs under Europe's Medical Devices Regulation pose barriers for smaller firms, those that remain in the market benefit from reduced competition.

Emerging regions, including South America and the Middle East and Africa, are experiencing double-digit growth in procedures, although infrastructure constraints limit immediate volume expansion. LG Chem's launch of VITARAN in Thailand reflects a broader trend of multinational companies adapting their portfolios to local markets. These firms are also establishing regional depots to reduce lead times and navigate tariff complexities. As regulatory frameworks in these regions mature, the market is expected to transition from heavy import reliance to selective local manufacturing partnerships, further diversifying the global hyaluronic acid products market.

- AbbVie Inc.

- Anika Therapeutics, Inc.

- Contipro a.s.

- Ferring B.V.

- Galderma S.A.

- Kewpie Corporation

- Lifecore Biomedical, Inc.

- Sanofi S.A.

- Seikagaku Corporation

- DSM-Firmenich AG

- Givaudan SA

- Fufeng Group Company Limited

- Bloomage Biotechnology Corporation Limited

- Stanford Chemicals

- Zimmer Biomet Holdings, Inc.

- HTL Biotechnology

- LG Group (LG Chem Life Sciences)

- Crown Laboratories, Inc. (Revance Therapeutics)

- Merz GmbH & Co. KGaA

- Baoding Faithful Industry

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for anti-aging solutions in skincare

- 4.2.2 Growing use in aesthetic dermatology and cosmetic injections

- 4.2.3 Expansion in orthopedic applications

- 4.2.4 Popularity in oral HA supplements for joint and skin health\

- 4.2.5 Demand for non-animal and vegan sources of hyaluronic acid

- 4.2.6 Adoption in advanced drug delivery systems

- 4.3 Market Restraints

- 4.3.1 Allergic reactions and inflammation from consumption

- 4.3.2 Regulatory challenges for oral HA supplements and claims

- 4.3.3 Storage sensitivity and risk of microbial contamination

- 4.3.4 Challenges in combining with certain active ingredients

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porters Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Molecular Weight

- 5.1.1 High Molecular Weight

- 5.1.2 Low Molecular Weight

- 5.1.3 Ultra Low Molecular Weight

- 5.2 By Application

- 5.2.1 Dietary Supplements

- 5.2.2 Pharmaceutical Industry

- 5.2.3 Cosmetics Industry

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 Italy

- 5.3.2.4 France

- 5.3.2.5 Spain

- 5.3.2.6 Poland

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 AbbVie Inc.

- 6.4.2 Anika Therapeutics, Inc.

- 6.4.3 Contipro a.s.

- 6.4.4 Ferring B.V.

- 6.4.5 Galderma S.A.

- 6.4.6 Kewpie Corporation

- 6.4.7 Lifecore Biomedical, Inc.

- 6.4.8 Sanofi S.A.

- 6.4.9 Seikagaku Corporation

- 6.4.10 DSM-Firmenich AG

- 6.4.11 Givaudan SA

- 6.4.12 Fufeng Group Company Limited

- 6.4.13 Bloomage Biotechnology Corporation Limited

- 6.4.14 Stanford Chemicals

- 6.4.15 Zimmer Biomet Holdings, Inc.

- 6.4.16 HTL Biotechnology

- 6.4.17 LG Group (LG Chem Life Sciences)

- 6.4.18 Crown Laboratories, Inc. (Revance Therapeutics)

- 6.4.19 Merz GmbH & Co. KGaA

- 6.4.20 Baoding Faithful Industry

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK