PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852119

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852119

India Ceramic Tiles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

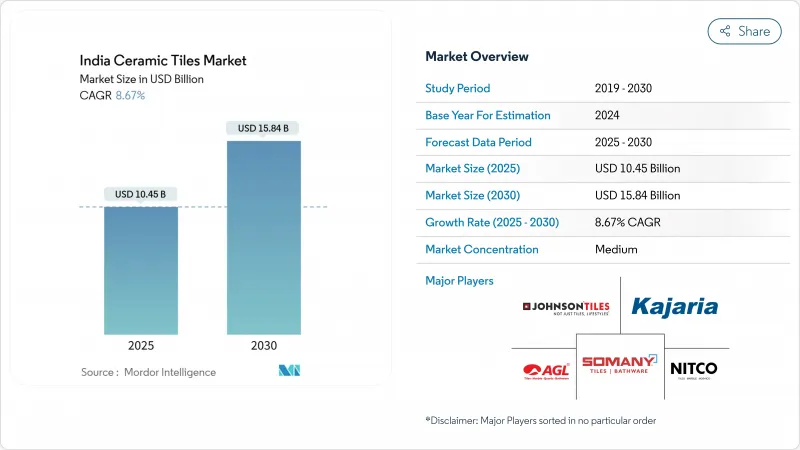

The India ceramic tiles market size stood at USD 10.45 billion in 2025 and is forecast to reach USD 15.84 billion by 2030, expanding at an 8.67% CAGR during 2025-2030.

Strong demand from affordable-housing schemes, smart-city programs and private real-estate investments is underpinning a steady sales trajectory as the nation urbanizes at scale. Continuous technology upgrades inside the Morbi production hub, wider natural-gas pipeline coverage and the arrival of hydrogen-ready kilns are lowering unit costs, allowing organized manufacturers to compete aggressively in premium and mid-market price bands. Adoption of large-format slab tiles, digital-inkjet printing and thin-set overlay systems is widening design possibilities for architects and homeowners alike. Parallel growth in export volumes, particularly to the United States and Gulf Cooperation Council (GCC) countries, adds another earnings layer, even as anti-dumping probes and logistics bottlenecks at Mundra port inject near-term uncertainty.

India Ceramic Tiles Market Trends and Insights

Surging Affordable-Housing & Smart-City Projects

PMAY-U 2.0's commitment to build an additional 10 million pucca homes backed by INR 10 lakh crore (USD 120.5 billion) creates a durable order pipeline for ceramic flooring and wall solutions. The program's integration of BIS quality standards tilts procurement toward organized plants capable of consistent output, supporting gradual consolidation inside the India ceramic tiles market. Simultaneously, the Smart Cities Mission funnels INR 2.05 lakh crore (USD 24.7 billion) into 5,151 urban-renewal projects that routinely specify premium porcelain or glazed vitrified tiles for transit hubs, waterfront promenades and public-housing corridors. Together these two schemes collectively demand 700-900 million m2 of annual built-up area, magnifying domestic consumption even if export orders soften. Suppliers that align product portfolios with local municipal tender specifications gain preferred-vendor status and longer visibility on capacity utilization. Government outlays also encourage regional clusters-like Uttar Pradesh and Andhra Pradesh-to court ancillary investments, nudging the India ceramic tiles market deeper into hinterland districts.

Urban Middle-Class Renovation Boom

Disposable incomes in metro households crossed USD 5,000 per capita in 2024, prompting a lifestyle-driven refurbishment wave in kitchens, bathrooms and living rooms. Unlike bulk new-build contracts, renovation orders favor curated patterns, smaller batch volumes and quick-turn logistics, elevating margins for branded SKUs with digital-inkjet motifs. E-commerce catalogues, augmented-reality room visualizers and influencer-led design blogs accelerate consumer discovery, and direct-to-home parcel deliveries cut out layers of distribution mark-ups. Tier-2 cities such as Jaipur, Coimbatore and Vijayawada are joining the upgrade trend as property owners modernize two-decade-old structures. Financial institutions have extended ten-year home-improvement loans at single-digit interest, further lubricating spend. Collectively, renovations inject counter-cyclical resilience into the India ceramic tiles market because projects proceed even when macro housing starts wobble.

Natural-Gas Price Volatility

Spot LNG at the Indian regasification gate doubled between early-2022 and mid-2023, squeezing EBITDA margins for kilns calibrated on fixed gas contracts. Smaller operators, lacking hedging lines, were forced into 15-day shutdowns to avoid loss-making dispatches. Although long-term Qatar and Russian pipeline deals restored some visibility, traders report forward curves still 20% above pre-COVID averages. The precarious input cost environment dissuades fresh brownfield capacity, particularly for unorganized units under 10,000 m2/day. Several states have floated relief rebates, but approvals remain piecemeal. The volatility underscores why hydrogen blending and electrified kilns hold strategic value.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Large-Format Slab Tiles

- Morbi Clusters' Hydrogen-Ready Kilns Cut Energy Cost

- Anti-Dumping Duties in Key Export Destinations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The India ceramic tiles market size for porcelain registered USD 5.8 billion, and segment CAGR is forecast near 8.2% through 2030 as designers replace granite with polished porcelain in airport concourses. Glazed ceramic tiles, priced 8-12% lower, are accelerating faster at 9.01% CAGR on the back of mid-income housing and chromatic bathroom palettes. Unglazed quarry tiles keep a foothold in warehouse aisles where slip rating standards trump aesthetics. Mosaic variants, though sub-5% of revenue, fetch premium margins in boutique hospitality and pool decking applications, drawing interest from artisanal startups. During 2024-2025 at least nine Morbi plants retooled biscuit firing to produce 20 mm outdoor porcelains aimed at European landscaping contractors.

Floor applications dominate with 76.31% market share in 2024 and lead growth projections at 9.14% CAGR through 2030, reflecting the fundamental role of flooring in both residential and commercial construction projects. This segment's strength derives from ceramic tiles' superior performance characteristics compared to alternative flooring materials, including durability, maintenance ease, and design versatility across diverse applications. Wall applications represent the secondary market segment, driven by bathroom and kitchen renovations where ceramic tiles provide moisture resistance and aesthetic appeal. Roofing applications remain specialized, serving specific architectural requirements and regional preferences where ceramic tiles offer thermal performance advantages.

Floor applications dominate with 76.31% market share in 2024 and lead growth projections at 9.14% CAGR through 2030, reflecting the fundamental role of flooring in both residential and commercial construction projects. This segment's strength derives from ceramic tiles' superior performance characteristics compared to alternative flooring materials, including durability, maintenance ease, and design versatility across diverse applications. Wall applications represent the secondary market segment, driven by bathroom and kitchen renovations where ceramic tiles provide moisture resistance and aesthetic appeal. Roofing applications remain specialized, serving specific architectural requirements and regional preferences where ceramic tiles offer thermal performance advantages.

The segment benefits from ceramic tiles' competitive positioning against luxury vinyl tile (LVT) and stone plastic composite (SPC) flooring, which are gaining traction in commercial applications but remain limited by durability concerns in high-traffic environments. Regional preferences influence application patterns, with South India showing stronger adoption of ceramic tiles for wall applications compared to North India's floor-focused usage. The application mix evolution suggests opportunities for manufacturers to develop specialized products for emerging use cases while maintaining leadership in core flooring applications.

The India Ceramic Tiles Market Report is Segmented by Product Type (Porcelain Tiles, Glazed Ceramic Tiles, and More), Application (Floor, Wall, Roofing), End-User (Residential, Commercial), Construction Type (New Construction, Renovation and Replacement), Distribution Channel (Specialty Stores, Home Improvement Stores, and More), and Geography (North India, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Kajaria Ceramics Ltd

- Somany Ceramics Ltd

- H&R Johnson (India)

- Asian Granito India Ltd

- Nitco Ltd

- Orient Bell Ltd

- RAK Ceramics India

- Exxaro Tiles Ltd

- Varmora Granito

- Simpolo Ceramics

- Johnson Pedder

- Murudeshwar Ceramics (Naveen)

- Pavit Ceramics

- Grindwell Norton (Saint-Gobain India)

- Astral Tiles

- Cera Sanitaryware Ltd

- Capron Granito

- Metro City Tiles

- Itaca Ceramics

- Regent Granito

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging affordable-housing & Smart-City projects

- 4.2.2 Urban middle-class renovation boom

- 4.2.3 Shift toward large-format slab tiles

- 4.2.4 Morbi clusters' hydrogen-ready kilns cut energy cost

- 4.2.5 Digital-inkjet mass customization for small builders

- 4.2.6 Rising adoption of thin-set overlay systems

- 4.3 Market Restraints

- 4.3.1 Natural-gas price volatility

- 4.3.2 Anti-dumping duties in key export destinations

- 4.3.3 Logistics bottlenecks at Mundra port

- 4.3.4 Commercial shift to LVT/SPC flooring

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Industry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Porcelain Tiles

- 5.1.2 Glazed Ceramic Tiles

- 5.1.3 Unglazed Ceramic Tiles

- 5.1.4 Mosaic Tiles

- 5.1.5 Others (Decorative, Patterned, Handmade)

- 5.2 By Application

- 5.2.1 Floor

- 5.2.2 Wall

- 5.2.3 Roofing

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.2.1 Hospitality (Hotels, Resorts)

- 5.3.2.2 Retail Spaces

- 5.3.2.3 Offices & Institutions

- 5.3.2.4 Healthcare

- 5.3.2.5 Educational Facilities

- 5.3.2.6 Transport Hubs (Airports, Metro, Bus Terminals)

- 5.3.2.7 Other Commercial Users

- 5.4 By Construction Type

- 5.4.1 New Construction

- 5.4.2 Renovation and Replacement

- 5.5 By Distribution Channel

- 5.5.1 Specialty Tile & Stone Stores

- 5.5.2 Home Improvement & DIY Stores

- 5.5.3 Online Retail

- 5.5.4 Direct Sales to Contractors

- 5.6 By Geography

- 5.6.1 North India

- 5.6.2 South India

- 5.6.3 West India

- 5.6.4 East India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Kajaria Ceramics Ltd

- 6.4.2 Somany Ceramics Ltd

- 6.4.3 H&R Johnson (India)

- 6.4.4 Asian Granito India Ltd

- 6.4.5 Nitco Ltd

- 6.4.6 Orient Bell Ltd

- 6.4.7 RAK Ceramics India

- 6.4.8 Exxaro Tiles Ltd

- 6.4.9 Varmora Granito

- 6.4.10 Simpolo Ceramics

- 6.4.11 Johnson Pedder

- 6.4.12 Murudeshwar Ceramics (Naveen)

- 6.4.13 Pavit Ceramics

- 6.4.14 Grindwell Norton (Saint-Gobain India)

- 6.4.15 Astral Tiles

- 6.4.16 Cera Sanitaryware Ltd

- 6.4.17 Capron Granito

- 6.4.18 Metro City Tiles

- 6.4.19 Itaca Ceramics

- 6.4.20 Regent Granito

7 Market Opportunities & Future Outlook

- 7.1 Green hydrogen-fired kilns reach commercial scale

- 7.2 Tile-as-a-Service subscription models for retail chains