PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852140

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852140

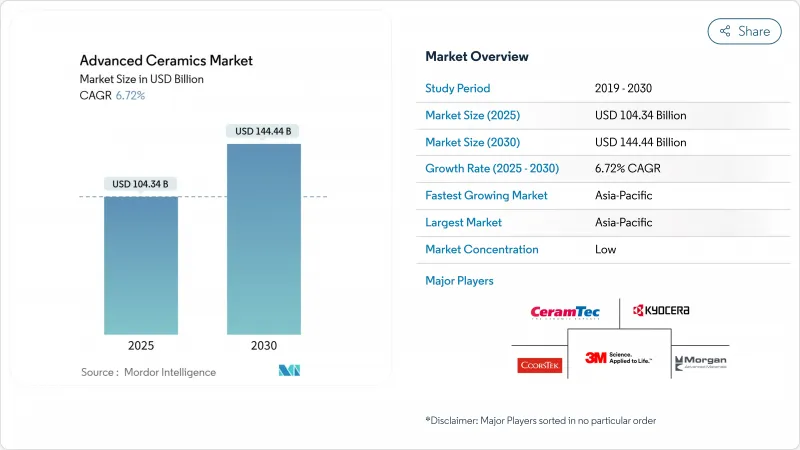

Advanced Ceramics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The advanced ceramics market is valued at USD 104.34 billion in 2025 and is forecast to expand to USD 144.44 billion by 2030, advancing at a 6.72% CAGR.

Rising demand for materials that combine lightweight, high hardness, and thermal resilience is pushing aerospace, electronics, energy, and healthcare manufacturers to shift away from metals and high-performance polymers. Material innovation, particularly around titanate-based electroceramics and ceramic matrix composites, enlarges the addressable opportunity set for suppliers. Asia-Pacific retains its leadership position due to strong semiconductor capital expenditure, while medical applications record double-digit growth as bioceramics replace metal implants. Although elevated production costs and complex sintering pathways remain headwinds, automation, additive manufacturing, and closed-loop recycling initiatives steadily improve cost curves and environmental footprints.

Global Advanced Ceramics Market Trends and Insights

Rise in Use as Alternative to Metals and Plastics

Advanced ceramics deliver hardness, wear resistance, and temperature stability that metals cannot match. Ceramic matrix composites in jet-engine hot sections cut component weight by 30% and improve fuel burn by 15% compared with nickel super-alloys. Automotive turbocharger rotors fabricated from silicon nitride withstand exhaust streams above 1,000 °C while maintaining dimensional accuracy. Industrial pump housings made from alumina and zirconia now last three to five times longer than stainless variants in abrasive slurries.

Growing Demand in the Medical Industry

Bioceramics such as alumina and zirconia exhibit proven biocompatibility and minimal ion release, which lengthens implant lifespans and decreases revision surgeries. Surgeons increasingly rely on 3D-printed silicon-nitride spinal cages tailored to patient anatomy, an advance made possible by low-temperature stereolithography. Orthopedic device makers also experiment with bioactive glass coatings that stimulate osteointegration and with drug-eluting porous ceramics for localized therapeutics.

Complex Manufacturing Process

Maintaining +-5 °C uniformity at 1,600 °C across large load sizes is challenging. Even minor temperature gradients create residual stresses that downgrade mechanical strength, forcing suppliers to perform additional inspection and culling. Precision grinding of fully sintered parts often records yields below 85% on complicated geometries. Additive manufacturing technologies such as binder jetting show promise by building near-net-shape parts that need minimal finishing, but throughput and surface finish still trail conventional routes

Other drivers and restraints analyzed in the detailed report include:

- Eco-friendliness and Reliability of Use

- Increasing Demand from Electronics and Semiconductors Industry

- End-of-Life Recycling Challenges Limiting ESG Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Alumina dominated the advanced ceramics market with a 41% share in 2024, supported by its balanced cost-performance profile and established supply chains. The material is entrenched in substrates, cutting tools, biomedical heads, and wear parts. Continuous process refinements now deliver sub-micron grain sizes that lift fracture toughness to 6 MPa*m1/2, enabling thinner components without performance trade-offs. On the demand side, electrification of transport and grid storage drives purchases of alumina-rich insulating hardware.

Titanate ceramics are the fastest-expanding material group at a 7.8% CAGR through 2030. Barium titanate multilayer capacitors remain the backbone of power-management circuits in smartphones and electric vehicles. Concurrently, lead-free potassium sodium niobate titanates gain traction in sonar transducers as a sustainable replacement for lead zirconate titanate. Recent research demonstrated ZnTiO3-ZnO nanocomposite coatings that kill 97% of Staphylococcus aureus on contact, widening titanate potential in antimicrobial surfaces.

Monolithic ceramics held 78% of the advanced ceramics market size in 2024 because single-phase alumina, zirconia, and silicon nitride are well understood and cost-efficient at scale. Standardization around ISO 602 and ASTM C1327 test methods simplifies qualification for aerospace or medical entry, sustaining volume momentum. Producers continue to improve reliability through powder morphology control, resulting in Weibull moduli above 20 for structural grades, which reduces part-to-part variability.

Although smaller in dollar terms, Ceramic matrix composites exhibit an 8.12% CAGR owing to their transformational weight-to-strength trade-off. Exhaust systems and next-generation nozzle guide vanes now use silicon-carbide fiber-reinforced silicon-carbide matrices that tolerate 1,400 °C gas streams without active cooling. Airbus and GE are flight-testing oxide-oxide CMCs in fuselage stiffeners to curb maintenance costs. Electrochemical energy companies apply carbon-fiber-reinforced alumina in solid-oxide fuel-cell interconnects to extend stack life. The rapid conversion of laboratory concepts into commercial runs underscores the composite class as a major disruptive force within the advanced ceramics industry.

The Advanced Ceramics Market Report Segments the Industry by Material Type (Alumina, Zirconia, Titanate, Silicon Carbide, and More), Class Type (Monolithic Ceramics, Ceramic Matrix Composites, and Ceramic Coatings), Application (Structural Ceramics, Bioceramics, Electroceramics, and More), End-User Industry (Electrical and Electronics, Transportation, Medical, and More), and Geography (Asia-Pacific, North America, and More).

Geography Analysis

Asia-Pacific possessed 54% of the advanced ceramics market in 2024, underpinned by dense electronics clusters, established powder supply chains, and government incentives for high-value materials. China's 14th Five-Year Plan classifies advanced ceramics as a strategic segment, unlocking tax credits and grant funding for pilot lines.

North America is witnessing a rise in consumption owing to robust aerospace, defense, and medical verticals. The United States Air Force Research Laboratory actively funds lightweight CMC combustor liners to extend jet-engine service intervals. Orthopedic device hubs in Indiana and Tennessee procure large volumes of zirconia-toughened alumina for hip components, driving concentrated regional demand.

Europe maintains a prominent footprint through Germany's advanced machinery and Italy's sanitary ware expertise. The European Commission's Advanced Materials for Industrial Leadership initiative emphasizes sustainability and recyclability, ensuring research budgets flow into low-carbon sintering and circular-economy pilots.

- 3M

- AGC Inc.

- Blasch Precision Ceramics, Inc.

- CeramTec GmbH

- CoorsTek Inc.

- Corning Incorporated

- Elan Technology

- International Syalons (Newcastle) Limited

- KYOCERA Corporation

- MARUWA Co., Ltd.

- Materion Corporation

- McDanel Advanced Material Technologies LLC

- Morgan Advanced Materials

- Murata Manufacturing Co., Ltd.

- Rauschert Heinersdorf-Pressig GmbH

- Saint-Gobain

- SPT- Group

- Vesuvius

- Wonik QnC Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in Use as Alternative to Metals and Plastics

- 4.2.2 Growing Demand in the Medical Industry

- 4.2.3 Eco-friendliness and Reliability of Use

- 4.2.4 Increasing Demand from Electronics and Semiconductors Industry

- 4.2.5 Rising Usage in Aerospace and Defense Sector

- 4.3 Market Restraints

- 4.3.1 High Production Costs

- 4.3.2 Complex Manufacturing Process

- 4.3.3 End-of-Life Recycling Challenges Limiting ESG Adoption

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Patent Analysis

- 4.7 Price Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Alumina

- 5.1.2 Zirconia

- 5.1.3 Titanate

- 5.1.4 Silicon Carbide

- 5.1.5 Silicon Nitride

- 5.1.6 Aluminum Nitride

- 5.1.7 Magnesium Silicate

- 5.1.8 Pyrolytic Boron Nitride

- 5.1.9 Others

- 5.2 By Class Type

- 5.2.1 Monolithic Ceramics

- 5.2.2 Ceramic Matrix Composites

- 5.2.3 Ceramic Coatings

- 5.3 By Application

- 5.3.1 Structural Ceramics

- 5.3.2 Bioceramics

- 5.3.3 Electroceramics

- 5.3.4 Wear and Corrosion Components

- 5.3.5 Thermal Barrier and UHTC Components

- 5.3.6 Catalyst Supports and Filters

- 5.3.7 Others (Environmental and Energy Systems)

- 5.4 By End-user Industry

- 5.4.1 Electrical and Electronics

- 5.4.2 Transportation

- 5.4.3 Medical

- 5.4.4 Industrial

- 5.4.5 Defense and Security

- 5.4.6 Chemical

- 5.4.7 Other End-user Industries (Energy and Environmental)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global overview, Market overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 AGC Inc.

- 6.4.3 Blasch Precision Ceramics, Inc.

- 6.4.4 CeramTec GmbH

- 6.4.5 CoorsTek Inc.

- 6.4.6 Corning Incorporated

- 6.4.7 Elan Technology

- 6.4.8 International Syalons (Newcastle) Limited

- 6.4.9 KYOCERA Corporation

- 6.4.10 MARUWA Co., Ltd.

- 6.4.11 Materion Corporation

- 6.4.12 McDanel Advanced Material Technologies LLC

- 6.4.13 Morgan Advanced Materials

- 6.4.14 Murata Manufacturing Co., Ltd.

- 6.4.15 Rauschert Heinersdorf-Pressig GmbH

- 6.4.16 Saint-Gobain

- 6.4.17 SPT- Group

- 6.4.18 Vesuvius

- 6.4.19 Wonik QnC Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Increasing Applications of Silicon Carbide (SiC) and Gallium Nitride (GaN)