PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852147

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852147

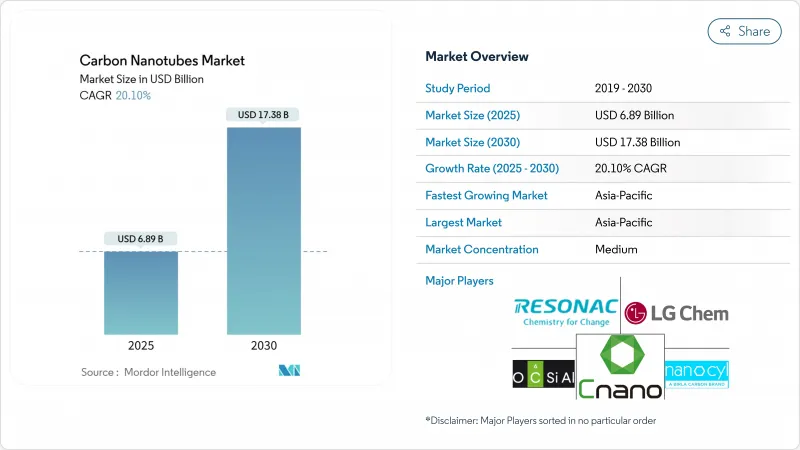

Carbon Nanotubes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Carbon Nanotubes Market size is estimated at USD 6.89 billion in 2025, and is expected to reach USD 17.38 billion by 2030, at a CAGR of 20.10% during the forecast period (2025-2030).

The strong outlook reflects the material's rapid adoption in batteries, aerospace composites, healthcare devices and water solutions. Multi-walled variants remain cost-efficient, so producers are scaling output while pursuing higher purity and uniformity. Asia-Pacific continues to dominate both demand and production capacity, helped by the region's electric-vehicle and electronics clusters. Consolidation among leading suppliers is gathering pace, illustrated by OCSiAl's purchase of Zyvex Technologies, which strengthened single-walled carbon nanotube scale and intellectual-property depth.

Global Carbon Nanotubes Market Trends and Insights

E-mobility boom accelerating CNT demand

Rising electric-vehicle output is lifting graphite anode silicon content, and carbon nanotubes ensure conductivity and mechanical stability at silicon loads near 20%, enabling 300 Wh/kg lithium-ion packs that reduce range anxiety. Automakers also specify nanotube-filled thermal interface pads that dissipate heat generated by power electronics, a need addressed by Dow and Carbice's 2024 alliance. The same conductivity advantage opens opportunities in busbars and battery-pack shielding. Start-ups producing silicon-CNT composite anodes have attracted venture funding, underscoring commercial confidence. As cell makers localize supply chains, nanotube capacity additions are being colocated near gigafactories, tightening integration between materials and battery production.

High-energy-density storage pushing technical frontiers

Grid storage and aerospace sectors require lighter, safer cells. Lithium-sulfur batteries using carbon-nanotube scaffolds anchor sulfur and suppress polysulfide shuttling, which is central to Lyten's 200 MWh plant targeted for 2025 ramp-up. Twisted single-walled carbon nanotube ropes store 2.1 MJ/kg as mechanical energy, exceeding lithium-ion energy density while avoiding flammable electrolytes. Supercapacitor makers employ multi-walled electrodes to deliver low equivalent-series resistance, ideal for rapid charge-discharge duty. Together, these advances translate to steady orders for high-conductivity grades and dispersion services.

Occupational toxicology and tightening regulation

European and U.S. agencies are drafting inhalation-exposure limits, citing fiber-like dimensions comparable with asbestos. Academic groups are refining dosimetry to link airborne mass and aspect ratio to pulmonary response. Compliance drives investment in fully enclosed reactors and automated bagging lines, raising capex for newcomers. Companies with documented safe-handling records secure contracts in automotive and aerospace programs where corporate sustainability metrics weigh heavily.

Other drivers and restraints analyzed in the detailed report include:

- Aerospace composites raising performance bar

- Desalination & sensor innovations aiding water-stressed regions

- Competition from graphene and boron-nitride nanotubes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Multi-walled carbon nanotubes accounted for 90% of 2024 share, reflecting mature chemical vapor deposition output and price points aligned with bulk additives. The segment is forecast to log a 20.51% CAGR, underpinning more than two-thirds of the carbon nanotubes market size expansion through 2030. Particle engineers are narrowing outer-diameter tolerance and reducing metal catalysts below 100 ppm, meeting electronics and medical-device thresholds. These improvements encourage adoption in conductive pastes, cell-phone speakers and supercapacitor electrodes, reinforcing volume leadership.

Single-walled carbon nanotubes remain under 10% by share yet command premium pricing in quantum and semiconductor niches. Electrostatic catalysis now yields 99.92% semiconducting purity at 0.95 nm diameter, enabling thin-film transistors on flexible substrates. Research on confined carbyne suggests future one-dimensional conductors for photonics. As niche devices commercialize, the carbon nanotubes market will capture incremental high-margin revenue without displacing multi-walled bulk demand.

The Carbon Nanotubes Market Report Segments the Industry by Type (Multi-Walled Carbon Nanotubes, Single-Walled Carbon Nanotubes, and Other Types), Manufacturing Method (Chemical Vapor Deposition (CVD), High-Pressure Carbon Monoxide (HiPco), and More), End-Use Industry (Electrical and Electronics, Energy, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa).

Geography Analysis

Asia-Pacific held 54% of global demand in 2024, and its 21.51% CAGR will sustain leadership. China's integrated battery-supply ecosystem catalyzes local nanotube manufacturers that supply gigafactories under long-term contracts. Japanese firms specialize in ultra-clean single-walled grades for displays, leveraging the "super-growth" method's high aspect ratios and alignment quality. Government incentives across South Korea and India further expand capacity through 2027, widening the regional cost advantage.

North America contributed a significant share to the total revenue. U.S. initiatives, including a USD 50 million Department of Energy grant to Cabot Corporation for Michigan production, shift supply security closer to domestic battery and defense customers. Aerospace composites and high-frequency connectors are key demand pillars, drawing on national labs' R&D strengths. Canada hosts pilot plants focused on methane-to-hydrogen pyrolysis with nanotube coproducts, linking climate and manufacturing policies.

Europe also contributed a significant share to the overall sales. German and French automakers require stringent material traceability, pushing suppliers to certify cradle-to-gate emissions. British universities spin out ventures targeting semiconductor interconnects, supported by national nanofabrication hubs. At the periphery, Middle East desalination agencies and African telecom tower installers evaluate nanotube-coated membranes and conductive coatings to tackle water and energy challenges, fostering pockets of emerging demand.

- Applied Nanostructures, Inc.

- Arkema

- Cabot Corporation

- Carbon Solutions, Inc.

- CHASM

- Cheap Tubes

- Chengdu Organic Chemicals Co., Ltd.

- CNT Co., Ltd.

- FutureCarbon GmbH

- Hanwha Group

- Hyperion Catalysis International

- Jiangsu Cnano Technology Co., Ltd.

- Kumho Petrochemical

- LG Chem

- Meijo Nano Carbon Co.,Ltd

- Nano-C

- Nanocyl SA

- OCSiAl

- Raymor Industries Inc.

- Resonac Holdings Corporation

- Thomas Swan & Co., Ltd.

- Toray Industries, Inc.

- Zyvex Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-mobility Boom Accelerating CNT Demand

- 4.2.2 Leap in High-Energy-Density Li-ion and Supercapacitor Production

- 4.2.3 Aerospace Push for Ultra-light Structural Composites

- 4.2.4 Desalination and Environmental Sensors Adoption in MEA and Asia

- 4.2.5 Additive Manufacturing Integration for Conductive Filaments

- 4.3 Market Restraints

- 4.3.1 Occupational Toxicology and Nano-regulation in Europe and United States

- 4.3.2 Competition from Graphene and Boron-Nitride Nanotubes in Thermal Apps

- 4.3.3 Patent Thickets Concentrating Licensing Costs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Patent Analysis

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Type

- 5.1.1 Multi-Walled Carbon Nanotubes

- 5.1.2 Single-Walled Carbon Nanotubes

- 5.1.3 Other Types (Armchair, Zigzag, Double-Walled)

- 5.2 By Manufacturing Method

- 5.2.1 Chemical Vapor Deposition (CVD)

- 5.2.2 High-Pressure Carbon Monoxide (HiPco)

- 5.2.3 Arc Discharge

- 5.2.4 Laser Ablation

- 5.3 By End-Use Industry

- 5.3.1 Electrical and Electronics

- 5.3.2 Energy

- 5.3.3 Automotive

- 5.3.4 Aerospace and Defense

- 5.3.5 Healthcare

- 5.3.6 Other Industries (Textiles, Construction, Plastics and Composites)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Applied Nanostructures, Inc.

- 6.4.2 Arkema

- 6.4.3 Cabot Corporation

- 6.4.4 Carbon Solutions, Inc.

- 6.4.5 CHASM

- 6.4.6 Cheap Tubes

- 6.4.7 Chengdu Organic Chemicals Co., Ltd.

- 6.4.8 CNT Co., Ltd.

- 6.4.9 FutureCarbon GmbH

- 6.4.10 Hanwha Group

- 6.4.11 Hyperion Catalysis International

- 6.4.12 Jiangsu Cnano Technology Co., Ltd.

- 6.4.13 Kumho Petrochemical

- 6.4.14 LG Chem

- 6.4.15 Meijo Nano Carbon Co.,Ltd

- 6.4.16 Nano-C

- 6.4.17 Nanocyl SA

- 6.4.18 OCSiAl

- 6.4.19 Raymor Industries Inc.

- 6.4.20 Resonac Holdings Corporation

- 6.4.21 Thomas Swan & Co., Ltd.

- 6.4.22 Toray Industries, Inc.

- 6.4.23 Zyvex Technologies

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Increasing Demand for Energy Storage Devices