PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910442

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910442

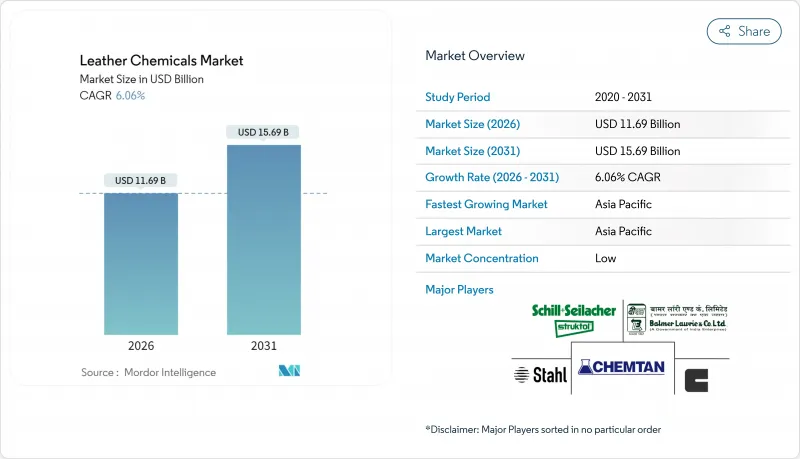

Leather Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Leather Chemicals Market is expected to grow from USD 11.02 billion in 2025 to USD 11.69 billion in 2026 and is forecast to reach USD 15.69 billion by 2031 at 6.06% CAGR over 2026-2031.

The uptrend is driven by the steady replacement of chromium-based tanning, increased demand from premium footwear and automotive interiors, and wider adoption of bio-based auxiliaries. Chrome-free chemical functions already dominate global demand, while finishing formulations are gaining traction thanks to stricter product-performance requirements. Asia-Pacific leads in both output and innovation, and the competitive field remains fragmented despite recent consolidation initiatives that seek to pair scale with sustainability.

Global Leather Chemicals Market Trends and Insights

Surge in Chrome-Free and Metal-Free Tanning Technologies

Regulators are setting strict chromium thresholds, spurring manufacturers to shift toward organic and mineral-free tanning agents. California's 2023 Chrome Plating ATCM bans new hexavalent chromium facilities and phases out decorative chrome plating, adding momentum to chrome-free adoption. Producers such as Gruppo Mastrotto have invested in vegetable-based methods, citing better biodegradability and shrinking carbon footprints. Laboratory studies confirm that biomass-based agents deliver higher degradation rates than chromium salts, easing end-of-life treatment challenges. Stahl's Granofin Easy F-90 Liq showcases how proprietary formulations save water and energy while eliminating Cr(VI) residues.

Rapid Growth of Footwear and Textile Industries

Antibacterial performance features are now routine after testing in La Rioja confirmed effective microbe kill rates for in-shoe compounds. Mainland China processes nearly 4 billion ft2 of hides per year, making it the largest single customer of beam-house and finishing chemicals in the leather chemicals market. The textile sector adds a second demand stream by utilizing similar finishing agents on mixed material uppers. Brazil's supply reacted quickly, exporting more tanned hides to China as local auto leather volumes escalated.

Strict Chromium VI Emission and Wastewater Norms

ECHA plans to stop 17 tonnes of Cr(VI) from entering ecosystems each year, imposing compliance investments that strain tanners' margins. California's Proposition 65 requires 100% certified chrome-safe leather by December 2025, forcing brands to audit upstream supply chains. The German Federal Institute for Risk Assessment reported that more than half of the tested leather items exceed the 3 mg/kg REACH limit, sparking recalls and legal exposure. Upgrading effluent plants with electrochemical oxidation or Fenton processes can slash water draw-off, but it involves multimillion-dollar capital outlay. Smaller workshops face existential risks if they cannot absorb these costs or secure chrome-free expertise.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Demand for Automotive and Aviation Upholstery

- Rising Preference for Bio-Based Fatliquors and Syntans

- Competition from Synthetic and Vegan Leather Chemistries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Finishing chemicals registered the highest 6.72% CAGR between 2026 and 2031, while tanning and dyeing agents retained 44.78% of the 2025 volume. Manufacturers adopt multifunctional topcoats that grant abrasion resistance and antimicrobial traits without fluorinated inputs. Activated Silk L1 demonstrates how bio-based polymers can replace solvent-driven lacquers while matching gloss metrics.

The tanning segment continues to pivot toward vegetable and synthetic organic systems, easing Cr(VI) discharge worries and satisfying label certification schemes. Beam-house detergents have moved toward enzyme complexes that clean and degrease at lower pH, aligning with wastewater reduction goals. Finishing suppliers thus capture premium margins, while wet-end players strengthen portfolios with turnkey eco-recipes that shorten process cycles.

The Leather Chemicals Report is Segmented by Product Type (Tanning and Dyeing Chemicals, Beam-House Chemicals, and Finishing Chemicals), Chemical Function (Chrome-Based, Chrome-Free Mineral, and Synthetic Organic), End-User Industry (Footwear, Furniture, Automotive, Textile and Fashion, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific controlled 48.37% of 2025 revenue and is forecast to grow at a 6.65% CAGR during 2026-2031. India exported USD 5.26 billion worth of leather goods in FY 2023 and employs 4.42 million workers, amplifying demand for beam-house auxiliaries and finishing agents. Regional cost advantages, integrated supply pools, and rising domestic consumption keep APAC at the epicenter of new capacity expansions. Japanese and South Korean buyers, though smaller in volume, demand high-purity syntans and topcoats, favoring suppliers with ISO 14001 plants and VOC-free recipes.

North America and Europe present mature but premium-priced outlets where compliance support often outweighs per-liter discounts. Europe tightened chromium limits to below 3 mg/kg in finished goods, driving chrome-free orders in Italy, Spain, and Germany. California prescribed 75% compliance to chrome-safe standards by mid-2025, adding urgency for upstream audits and green-tag certificates. These rules channel spending into bio-based synthetics, low-fogging fatliquors, and short-cycle recycling systems. North American auto trim plants require USMCA-proven content and favor suppliers offering regional blending stations. Together, the two regions sustain demand for sustainable high-performance chemicals.

South America supplies raw hides globally yet is increasing local finishing. Currency swings and EU traceability rules challenge cost structures but also encourage investments in automated beam-house lines. Middle Eastern tanneries leverage petrochemical feedstocks for specialty syntans, while new African projects look to shift from wet-blue exports to crust or finished leather, widening the client base for comprehensive processing solutions.

- AMIT

- Balmer Lawrie & Co. Ltd.

- Buckman

- Chemtan Company, Inc.

- CLARIANT

- Dyna Glycols

- DyStar Singapore Pte Ltd.

- Fashion Chemicals GmbH & Co. KG

- Indofil Industries Limited.

- SCHILL+SEILACHER GMBH

- Sisecam

- Stahl Holdings B.V.

- Syn-Bios S.p.A.

- TEXAPEL S.A.

- TFL

- YILDIRIM Group Of Companies

- Zschimmer & Schwarz Chemie GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Chrome-Free and Metal-Free Tanning Technologies

- 4.2.2 Rapid Growth of Footwear and Textile Industries

- 4.2.3 Increasing Demand for Automotive and Aviation Upholstery

- 4.2.4 Rising Preference for Bio-Based Fatliquors and Syntans

- 4.2.5 Digital Leather Printing Chemicals Gaining Traction

- 4.3 Market Restraints

- 4.3.1 Strict Chromium VI Emission and Wastewater Norms

- 4.3.2 High Energy and Wastewater-Treatment Cost

- 4.3.3 Competition From Synthetic and Vegan Leather Chemistries

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Tanning and Dyeing Chemicals

- 5.1.2 Beam-house Chemicals

- 5.1.3 Finishing Chemicals

- 5.2 By Chemical Function

- 5.2.1 Chrome-based

- 5.2.2 Chrome-free Mineral

- 5.2.3 Synthetic Organic

- 5.3 By End-user Industry

- 5.3.1 Footwear

- 5.3.2 Furniture

- 5.3.3 Automotive

- 5.3.4 Textile and Fashion

- 5.3.5 Other End-user Industries (Heavy Leather and Saddlery, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AMIT

- 6.4.2 Balmer Lawrie & Co. Ltd.

- 6.4.3 Buckman

- 6.4.4 Chemtan Company, Inc.

- 6.4.5 CLARIANT

- 6.4.6 Dyna Glycols

- 6.4.7 DyStar Singapore Pte Ltd.

- 6.4.8 Fashion Chemicals GmbH & Co. KG

- 6.4.9 Indofil Industries Limited.

- 6.4.10 SCHILL+SEILACHER GMBH

- 6.4.11 Sisecam

- 6.4.12 Stahl Holdings B.V.

- 6.4.13 Syn-Bios S.p.A.

- 6.4.14 TEXAPEL S.A.

- 6.4.15 TFL

- 6.4.16 YILDIRIM Group Of Companies

- 6.4.17 Zschimmer & Schwarz Chemie GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment