PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852173

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852173

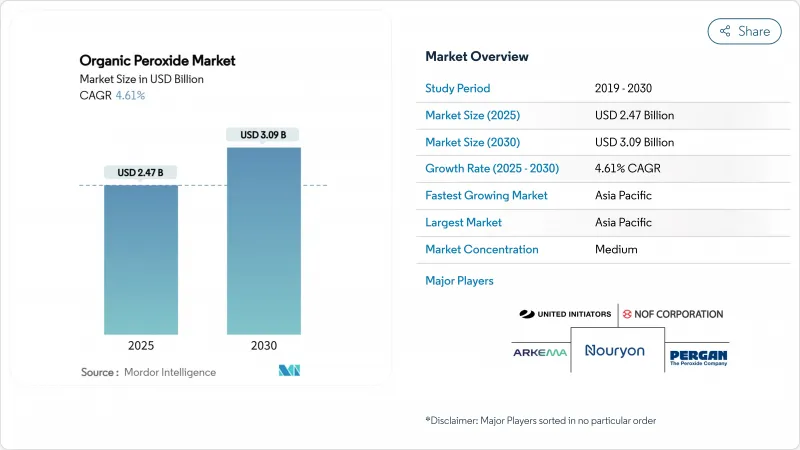

Organic Peroxide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Organic Peroxide Market size is estimated at USD 2.47 billion in 2025, and is expected to reach USD 3.09 billion by 2030, at a CAGR of 4.61% during the forecast period (2025-2030).

The rising use of advanced polyethylene and polypropylene grades, rapid uptake of EVA solar encapsulants, and the shift toward VOC-free powder coating systems underpin demand growth. Producers are scaling capacity in Asia Pacific to serve polymer and composites customers that require tight specification control, while safety-focused paste and emulsion formats gain wider acceptance. At the same time, volatile feedstock pricing and higher insurance premiums for storage facilities continue to pressure margins, steering manufacturers toward renewable feedstocks and safer handling solutions. Asia Pacific anchors both volume and incremental demand, followed by steady but more specialized growth in North America and Europe, where sustainability regulations accelerate product substitution.

Global Organic Peroxide Market Trends and Insights

Shift Toward Advanced PE and PP Grades

Rising requirements for controlled rheology polypropylene and high-melt-strength PP in packaging and automotive parts lift organic peroxide consumption across Asia Pacific. LyondellBasell raised recycled and renewable-based polymer output by 65% in 2024 to more than 200,000 t, with a target of 2 million t annually by 2030, increasing the need for organic peroxides that fine-tune molecular weight and branching. Processors report an 18% jump in PP processing efficiency when dicumyl peroxide is applied as a chain breaker, while branched PP made with Perkadox and Trigonox(R) grades delivers 30% better foam properties. As regional resin producers expand specialty capacity, the organic peroxide market gains a stable demand base.

Adoption of Organic Peroxides in EVA Solar Encapsulants

Fast-growing photovoltaic installations rely on EVA encapsulation sheets cross-linked with peroxides such as Luperox TBEC to reach gel contents above 75%, thereby enhancing module durability. China dominates EVA sheet output, and European module makers are also upgrading to higher-purity peroxide systems to curb power loss. These trends translate into steady incremental volumes for the organic peroxide market in the near term, especially for high-pressure polymerization grades that offer narrow decomposition profiles.

Insurance Premiums for Storage Facilities

Implementation of the revised ADR framework on 1 January 2025 elevates classification and inspection rigor for organic peroxide warehousing. European underwriters have lifted premiums for large-volume sites, raising operating costs and delaying expansion projects. Producers are responding by optimizing inventory levels and investing in smaller satellite depots, yet higher fixed costs constrain margin expansion for the organic peroxide market.

Other drivers and restraints analyzed in the detailed report include:

- Growth of VOC-Free Powder Coatings in Europe

- Automotive Lightweighting Drives Composite Applications

- Feedstock Supply Tightness

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Benzoyl peroxide retained a 24% revenue share of the organic peroxide market in 2024, reflecting its dual usage in polymer initiation and topical dermatology. Industrial grade volumes dominate because free-radical polymerization remains a high-throughput route for styrenics and acrylics. Nevertheless, concerns over benzene contamination in certain consumer products have raised scrutiny, spurring product reformulation.

Percarbonates, propelled by eco-friendly credentials and broad cleaning-agent appeal, are the fastest-growing sub-segment at a 4.74% CAGR. Commercialization of percarbonate-based advanced oxidation processes for wastewater remediation broadens the customer mix and supports future share gains.

Polymerization initiators captured 65% of the organic peroxide market share in 2024 and are forecast to post a 5.22% CAGR to 2030. High throughput LDPE and PP facilities favor well-characterized initiators such as tert-butyl peroxy-2-ethylhexanoate owing to predictable decomposition kinetics. Cross-linking agents are the next-largest category, used in wire-and-cable jacketing, foam insulation, and composite parts that need dimensional stability at elevated temperatures. Curing and hardening agents, though smaller in volume, gain importance in advanced resin chemistries for 3D printing and high-pressure RTM composites.

The Organic Peroxide Market Report Segments the Industry by Type (Diacyl Peroxides, Dialkyl Peroxides, Ketone Peroxides, and More), Function (Polymerization Initiators, and More), Form (Liquid, Solid, and Paste/Emulsion), Application (Polymers and Rubber, Coatings and Adhesives, Paper and Textile, Cosmetics, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia Pacific held 39% of the organic peroxide market in 2024 and is growing at a 4.89% CAGR, supported by robust downstream plastics and elastomer capacity additions. China dominates regional demand, and Nouryon's November 2024 expansion in Ningbo doubled the output of Perkadox 14 and Trigonox 101 to 6,000 tons, underscoring local appetite for controlled rheology modifiers.

North America is characterized by mature but value-added demand in automotive composites, healthcare, and high-purity semiconductor polymers. Producers emphasize safer formulations, and several have introduced emulsion-based initiators that align with stricter Department of Transportation guidelines on bulk peroxide transport.

Europe trails closely, with growth driven by environmental legislation that restricts VOC emissions and mandates safer carriage of dangerous goods. The ADR update, effective in 2025, imposes tighter storage segregation and training requirements, increasing operating costs but encouraging the adoption of paste and polymer-bound forms.

- ADEKA CORPORATION

- AKPA Kimya

- Arkema

- BASF

- Dow

- Evonik Industries AG

- Hanwha Group

- Jiangsu qiangsheng chemical co. LTD

- Kawaguchi Chemical Industry Co., LTD.

- Lianyungang Hualun Chemical Co.,Ltd.

- MITSUBISHI GAS CHEMICAL COMPANY, INC.

- MPI Chemie BV

- NOF CORPORATION

- Nouryon

- Novichem Sp. z o.o.

- PERGAN GmbH

- Plasti Pigments Pvt. Ltd.

- Shenzhen Bailingwei Technology Co., Ltd.

- Solvay

- United Chemicals

- United Initiators GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Polymer Demand Shift toward Advanced PE and PP Grades in Asia-Pacific

- 4.2.2 Rapid Adoption of Organic Peroxide

- 4.2.3 Growth of VOC-free, UV-curable Powder Coatings in Europe

- 4.2.4 Automotive Lightweighting, Elevated Use in Fiber-Reinforced Composites

- 4.2.5 Surging Utilization in Coating Applications

- 4.3 Market Restraints

- 4.3.1 High Insurance Premiums for Large-Scale Storage Facilities in EU

- 4.3.2 Supply Tightness of Feedstock

- 4.3.3 Rising Cost of Organic Peroxide

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Diacyl Peroxides

- 5.1.2 Dialkyl Peroxides

- 5.1.3 Ketone Peroxides

- 5.1.4 Hydro-Peroxides

- 5.1.5 Percarbonates

- 5.1.6 Benzoyl Peroxide

- 5.1.7 Peroxyesters

- 5.1.8 Others

- 5.2 By Function

- 5.2.1 Polymerization Initiators

- 5.2.2 Cross-Linking Agents

- 5.2.3 Curing/Hardening Agents

- 5.3 By Form

- 5.3.1 Liquid

- 5.3.2 Solid

- 5.3.3 Paste/Emulsion

- 5.4 By Application

- 5.4.1 Polymers and Rubber

- 5.4.2 Coatings and Adhesives

- 5.4.3 Paper and Textiles

- 5.4.4 Cosmetics

- 5.4.5 Healthcare

- 5.4.6 Other Application

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Nordics

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (Mergers and Acquisitions, JVs, Capacity Expansions)

- 6.3 Market Share(%)/ Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 ADEKA CORPORATION

- 6.4.2 AKPA Kimya

- 6.4.3 Arkema

- 6.4.4 BASF

- 6.4.5 Dow

- 6.4.6 Evonik Industries AG

- 6.4.7 Hanwha Group

- 6.4.8 Jiangsu qiangsheng chemical co. LTD

- 6.4.9 Kawaguchi Chemical Industry Co., LTD.

- 6.4.10 Lianyungang Hualun Chemical Co.,Ltd.

- 6.4.11 MITSUBISHI GAS CHEMICAL COMPANY, INC.

- 6.4.12 MPI Chemie BV

- 6.4.13 NOF CORPORATION

- 6.4.14 Nouryon

- 6.4.15 Novichem Sp. z o.o.

- 6.4.16 PERGAN GmbH

- 6.4.17 Plasti Pigments Pvt. Ltd.

- 6.4.18 Shenzhen Bailingwei Technology Co., Ltd.

- 6.4.19 Solvay

- 6.4.20 United Chemicals

- 6.4.21 United Initiators GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Growing Demand for Light-Weight Materials