PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852174

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852174

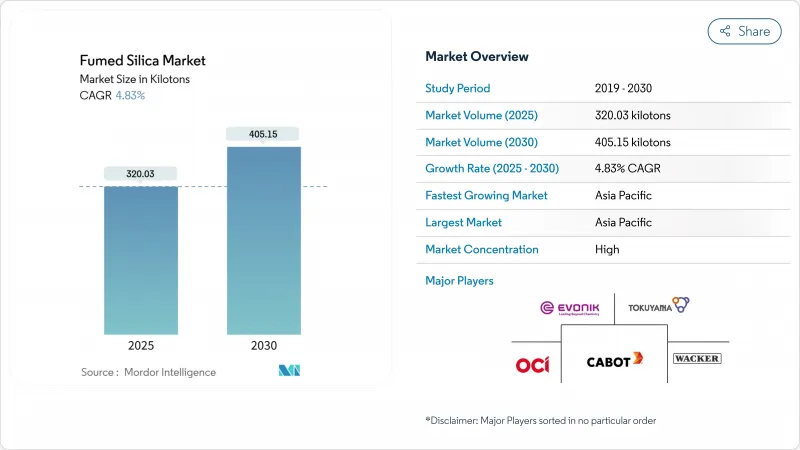

Fumed Silica - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Fumed Silica Market size is estimated at 320.03 kilotons in 2025, and is expected to reach 405.15 kilotons by 2030, at a CAGR of 4.83% during the forecast period (2025-2030).

The primary growth engines are rising demand for high-performance silicones in consumer electronics, ongoing construction activity, and expanding pharmaceutical production. The material's high surface area and low bulk density support its role as a rheology modifier and reinforcing agent across diverse formulations. Production technology is also shifting, with plasma-based reactors lowering energy costs and encouraging new entrants. At the same time, market participants are racing to embed sustainability credentials into their portfolios to secure long-term contracts with large electronics, automotive, and healthcare customers.

Global Fumed Silica Market Trends and Insights

Consumer-electronics boom in silicone elastomers in Asia

Explosive growth in smartphone, wearable, and semiconductor output across China, South Korea, and India has sharply increased demand for high-purity silicone elastomers. Fumed silica creates a three-dimensional network within silicone matrices, delivering thermal stability and electrical insulation that conventional fillers cannot match. Miniaturization trends require tight mechanical tolerances, making the additive indispensable in encapsulants, sealants, and thermal interface materials.

Rapid penetration of 3D-printed photopolymer resins across Europe automotive prototyping

Automotive OEMs in Germany, France, and Italy have embraced stereolithography for lightweight prototype parts. Fumed silica imparts thixotropy that prevents sagging yet flows smoothly under shear, enabling accurate layer deposition and reproducible dimensional control. The value proposition justifies premium pricing because failed prototypes carry high cost and schedule penalties.

Price volatility of feed-grade silicon tetrachloride in APAC

Supply disruptions and competing polysilicon demand have led to sharp swings in silicon tetrachloride prices, compressing margins for fumed silica producers. Chinese environmental actions that closed non-compliant plants exacerbated shortages. Producers are locking long-term contracts and examining alternative precursors, but short-term volatility persists.

Other drivers and restraints analyzed in the detailed report include:

- Increasing demand from the paints and coatings industry

- Rapid growth in pharmaceuticals and personal care

- Capacity additions of lower-cost precipitated silica in Europe

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hydrophilic grades accounted for 75% of the fumed silica market share in 2024 and are set to grow at a 5.31% CAGR through 2030. The silanol-rich surface promotes hydrogen bonding with polar systems, reinforcing silicone elastomers and controlling viscosity in coatings. This segment's contribution to the fumed silica market size rises steadily as electronics and construction consumption scale up.

Hydrophobic products outperform hydrophilic variants in non-polar matrices because surface modification prevents agglomeration, and these variants show faster thixotropic recovery. Manufacturers are tailoring surface chemistries to precise polarity windows, reinforcing the premium positioning of this niche.

Flame hydrolysis retained 72% of the fumed silica market share in 2024, built on reliable quality control and global capacity. The process yields high-purity amorphous silica and supports a wide product slate under brands such as AEROSIL evonik.com. However, regulatory pressure on carbon emissions is limiting incremental investment. The fumed silica industry is therefore channeling research and development toward low-carbon manufacturing pathways.

Plasma or arc vapor oxidation is expanding at 5.88% CAGR, outpacing overall fumed silica market growth. Firms such as HPQ Silicon plan commercial output in 2025, targeting customers that require lower embedded carbon and bespoke performance attributes. As new capacity ramps up, cost parity with flame hydrolysis could shift procurement preferences.

The Fumed Silica Market Report Segments the Industry by Type (Hydrophilic and Hydrophobic), Production Process (Flame Hydrolysis and Plasma/Arc Vapor Oxidation), Function (Rheology Control/Thickening, Anti-settling/Anti-caking, and Others), Application (Silicone Rubber, Adhesives and Sealants, Paints, Coatings and Inks, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and More).

Geography Analysis

Asia-Pacific controlled 48% of the fumed silica market size in 2024 and is growing at a 5.12% CAGR through 2030. Electronics clusters across China and South Korea purchase significant volumes of encapsulants and thermal interface materials. Construction demand in India and Southeast Asia underpins adhesives, sealants, and paints.

North America commands a mature but innovation-oriented share of the fumed silica market. Europe contributes a steady volume anchored by automotive manufacturing, specialty coatings, and stringent environmental standards. Regulatory pressure under the EU ETS is catalyzing a gradual technology transition.

South America and the Middle-East, and Africa collectively hold a smaller share but show upward momentum, driven by infrastructure investments and diversification of local manufacturing.

- AMS Applied Material Solutions

- Cabot Corporation

- China-Henan Huamei Chemical Co.,Ltd.

- DONGYUE GROUP

- Evonik Industries AG

- Gelest Inc.

- Henan Xunyu Chemical Co., Ltd.

- Heraeus Group

- HPQ Silicon Inc.

- Kemipex

- Kemitura

- Ningbo Ruifeng Sealing Materials Co., Ltd.

- OCI Ltd.

- Orisil

- Redox

- Tokai Carbon Co., Ltd.

- Tokuyama Corporation

- Wacker Chemie AG

- Yichang CSG Polysilicon Co., Ltd.

- Zhejiang FuShiTe Group Co., Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Consumer-electronics led boom in silicone elastomers in Asia

- 4.2.2 Rapid penetration of 3-D-printed photopolymer resins across Europe automotive prototyping

- 4.2.3 Increasing Demand from the Paints and Coatings Industry

- 4.2.4 Rapid Growth in Pharmaceuticals and Personal Care

- 4.2.5 Food anti-caking reformulations driven by ASEAN clean-label norms

- 4.3 Market Restraints

- 4.3.1 Price volatility of feed-grade silicon tetrachloride in APAC

- 4.3.2 Capacity additions of lower-cost precipitated silica in Europe

- 4.3.3 High energy intensity of flame hydrolysis vs. plasma micro-reactors in EU ETS

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Hydrophilic

- 5.1.2 Hydrophobic

- 5.2 By Production Process

- 5.2.1 Flame Hydrolysis

- 5.2.2 Plasma/Arc Vapor Oxidation

- 5.3 By Function

- 5.3.1 Rheology Control/Thickening

- 5.3.2 Anti-settling/Anti-caking

- 5.3.3 Reinforcement/Filler

- 5.4 By Application

- 5.4.1 Silicone Rubber

- 5.4.2 Adhesives and Sealants

- 5.4.3 Paints, Coatings and Inks

- 5.4.4 Plastics and Composites (UPR)

- 5.4.5 Food and Beverages

- 5.4.6 Other Applications (Pharmaceuticals and Personal Care, etc)

- 5.5 Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AMS Applied Material Solutions

- 6.4.2 Cabot Corporation

- 6.4.3 China-Henan Huamei Chemical Co.,Ltd.

- 6.4.4 DONGYUE GROUP

- 6.4.5 Evonik Industries AG

- 6.4.6 Gelest Inc.

- 6.4.7 Henan Xunyu Chemical Co., Ltd.

- 6.4.8 Heraeus Group

- 6.4.9 HPQ Silicon Inc.

- 6.4.10 Kemipex

- 6.4.11 Kemitura

- 6.4.12 Ningbo Ruifeng Sealing Materials Co., Ltd.

- 6.4.13 OCI Ltd.

- 6.4.14 Orisil

- 6.4.15 Redox

- 6.4.16 Tokai Carbon Co., Ltd.

- 6.4.17 Tokuyama Corporation

- 6.4.18 Wacker Chemie AG

- 6.4.19 Yichang CSG Polysilicon Co., Ltd.

- 6.4.20 Zhejiang FuShiTe Group Co., Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Emerging Applications of Fumed Silica