PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906033

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906033

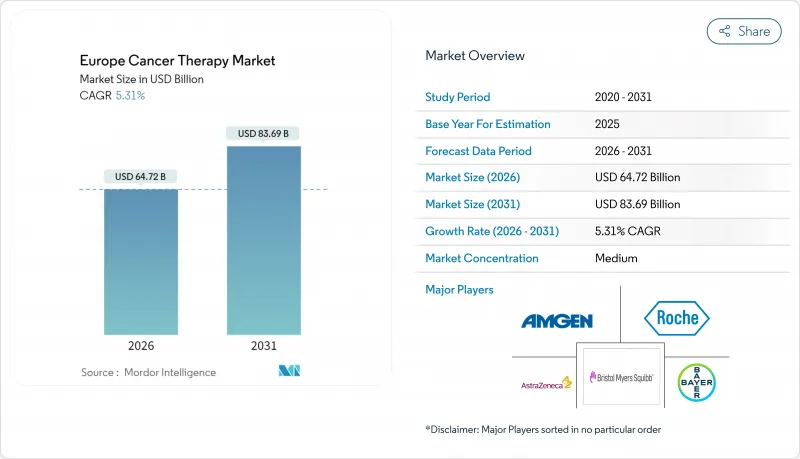

Europe Cancer Therapy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe Cancer Therapy Market is expected to grow from USD 61.46 billion in 2025 to USD 64.72 billion in 2026 and is forecast to reach USD 83.69 billion by 2031 at 5.31% CAGR over 2026-2031.

This steady trajectory reflects regulatory harmonization by the European Medicines Agency (EMA), the expansion of precision medicine under the EU Beating Cancer Plan, and sustained R&D investment in leading economies, such as Germany and France. Intensifying competition centers on antibody-drug conjugates and radioligand therapies, while the uptake of biosimilars accelerates cost containment efforts across public health systems. Cross-border CAR-T manufacturing, digital biomarker deployment, and a surge in venture capital for radiopharmaceutical start-ups further widen the addressable demand. Cost pressures, divergent health-technology assessment (HTA) timelines, and gaps in nuclear-medicine infrastructure remain the principal obstacles to timely patient access.

Europe Cancer Therapy Market Trends and Insights

Precision-Oncology Drug Approvals Surge Post-EMA Reforms

EMA modernization has accelerated precision-oncology pathways, with 28 oncology opinions in 2024 versus historical single-digit figures. Conditional marketing authorizations shortened time to market for biomarker-driven agents such as lazertinib, which reached European patients within 12 months of pivotal data read-out and delivered 23.7 months median progression-free survival against 16.6 months for comparator therapy. Companies now prioritizing real-world-evidence generation gain a durable competitive edge, whereas developers reliant on legacy models face erosion in launch velocity. Harmonized procedures also reduce duplicative submissions, freeing capital for late-stage trials and life-cycle management.

Biosimilar Oncology Uptake Lowering Therapy Costs

Europe's biosimilar penetration triggered double-digit volume growth across molecules such as trastuzumab and rituximab, driving price erosion beyond 40% in leading markets. Physician confidence broadened adoption after real-world equivalence studies, enabling payers to reallocate savings to innovative therapies. Originators respond by emphasizing superior clinical differentiation and bundled service offerings. Multi-source competition intensifies procurement pressure, favoring manufacturers with high-throughput biologics capacity and robust pharmacovigilance data packages.

Divergent HTA Reimbursement Timelines Across EU-5

The W.A.I.T. (Waiting to Access Innovative Therapies) indicator survey shows an average 531-day lag between EMA approval and patient availability across the five largest markets, reflecting heterogeneous evidence and pricing requirements. While the 2025 Joint Clinical Assessment regulation aims to align methodologies, transitional frictions may widen gaps as national agencies recalibrate their value frameworks. Larger pharmaceutical firms leverage multi-disciplinary market-access teams to navigate parallel submissions, whereas smaller innovators risk launch postponements and revenue shortfalls.

Other drivers and restraints analyzed in the detailed report include:

- Genomic Screening Roll-Outs in EU27 National Cancer Plans

- Cross-Border CAR-T Manufacturing Hubs in Benelux Initiative

- Hospital Capacity Gap for Nuclear-Medicine-Based Therapies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chemotherapy retained a 41.92% share of the Europe cancer therapy market size in 2025, reflecting its entrenched role in combination regimens. Yet targeted therapy is forecast to post a 6.14% CAGR, propelled by HER2-low breast cancer approvals and next-generation EGFR inhibitors that extend progression-free intervals. A maturing immunotherapy backbone is increasingly paired with precision inhibitors, enabling deeper responses across various tumor types and elevating biomarker testing rates.

Increasing clinical trial density underscores a strategic emphasis on tumor-agnostic indications, with basket study designs compressing development cycles. Biosimilar erosion in traditional cytotoxics accelerates revenue migration toward precision platforms, prompting legacy manufacturers to replenish pipelines via licensing or bolt-on acquisitions. The shift also reorients hospital formularies toward outpatient administration, reinforcing payer preference for cost-effective, biomarker-guided protocols.

Breast cancer dominated the Europe cancer therapy market, accounting for a 25.12% share in 2025, driven by established screening programs and well-established treatment algorithms. However, lung cancer is slated for the fastest 6.77% CAGR through 2031 as first-line immunotherapy combinations and exon-20 insertion inhibitors unlock previously refractory segments.

Environmental policy tightening on smoking and air-quality metrics may gradually reduce incidence. Yet, the rapid adoption of molecular diagnostics broadens eligible patient pools for targeted regimens in the near term. Pharmaceutical companies thus prioritize portfolio depth across genomic subsets, balancing blockbuster volume in hormone-positive breast cancer with high-growth revenue in niche lung-cancer mutations.

The Europe Cancer Therapy Market Report is Segmented by Therapy Type (Chemotherapy, Targeted Therapy, and More), Cancer Type (Breast Cancer, Lung Cancer, and More), Drug Class (PD-1/PD-L1 Inhibitors, Tyrosine Kinase Inhibitors, and More), Mode of Administration (Intravenous, Subcutaneous, and More), and Country (Germany, United Kingdom, France, Italy, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Roche

- Novartis

- AstraZeneca

- Pfizer

- Bristol-Myers Squibb

- Merck

- Sanofi

- Johnson & Johnson ( Janssen Biotech )

- GlaxoSmithKline

- Bayer

- Eli Lilly and Company

- Amgen

- Abbvie

- Boehringer Ingelheim Int'l GmbH

- Ipsen

- Daiichi Sankyo

- Takeda Pharmaceuticals

- Servier SAS

- Hikma Pharmaceuticals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Precision-Oncology Drug Approvals Surge Post-EMA Reforms

- 4.2.2 Biosimilar Oncology Uptake Lowering Therapy Costs

- 4.2.3 Genomic Screening Roll-Outs in EU27 National Cancer Plans

- 4.2.4 Cross-Border CAR-T Manufacturing Hubs in Benelux Initiative

- 4.2.5 VC Funding Boom or Radioligand Start-Ups

- 4.2.6 AI-Driven Trial-Matching Platforms Shorten Recruitment Time

- 4.3 Market Restraints

- 4.3.1 Divergent HTA Reimbursement Timelines Across EU-5

- 4.3.2 Hospital Capacity Gap for Nuclear-Medicine-Based Therapies

- 4.3.3 Oncology Workforce Shortages in CEE Nations

- 4.3.4 Rising Supply-Chain Risk for Critical API Imports

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Therapy Type

- 5.1.1 Chemotherapy

- 5.1.2 Targeted Therapy

- 5.1.3 Immunotherapy

- 5.1.4 Hormonal Therapy

- 5.1.5 Other Therapy Type

- 5.2 By Cancer Type

- 5.2.1 Breast Cancer

- 5.2.2 Lung Cancer

- 5.2.3 Colorectal Cancer

- 5.2.4 Prostate Cancer

- 5.2.5 Hematologic Cancers

- 5.2.6 Other Cancer Types

- 5.3 By Drug Class

- 5.3.1 PD-1/PD-L1 Inhibitors

- 5.3.2 Tyrosine Kinase Inhibitors

- 5.3.3 CDK4/6 Inhibitors

- 5.3.4 Hormone Antagonists

- 5.3.5 Antibody-Drug Conjugates

- 5.3.6 Other Drug Classes

- 5.4 By Mode of Administration

- 5.4.1 Intravenous

- 5.4.2 Subcutaneous

- 5.4.3 Oral

- 5.4.4 Other Mode of Administration

- 5.5 Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 F. Hoffmann-La Roche AG

- 6.3.2 Novartis AG

- 6.3.3 AstraZeneca PLC

- 6.3.4 Pfizer Inc.

- 6.3.5 Bristol-Myers Squibb Company

- 6.3.6 Merck & Co., Inc.

- 6.3.7 Sanofi S.A.

- 6.3.8 Johnson & Johnson ( Janssen Biotech )

- 6.3.9 GlaxoSmithKline PLC

- 6.3.10 Bayer AG

- 6.3.11 Eli Lilly and Company

- 6.3.12 Amgen Inc.

- 6.3.13 AbbVie Inc.

- 6.3.14 Boehringer Ingelheim Int'l GmbH

- 6.3.15 Ipsen S.A.

- 6.3.16 Daiichi Sankyo Company Ltd.

- 6.3.17 Takeda Pharmaceutical Company Ltd.

- 6.3.18 Servier SAS

- 6.3.19 Hikma Pharmaceuticals PLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment