PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906055

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906055

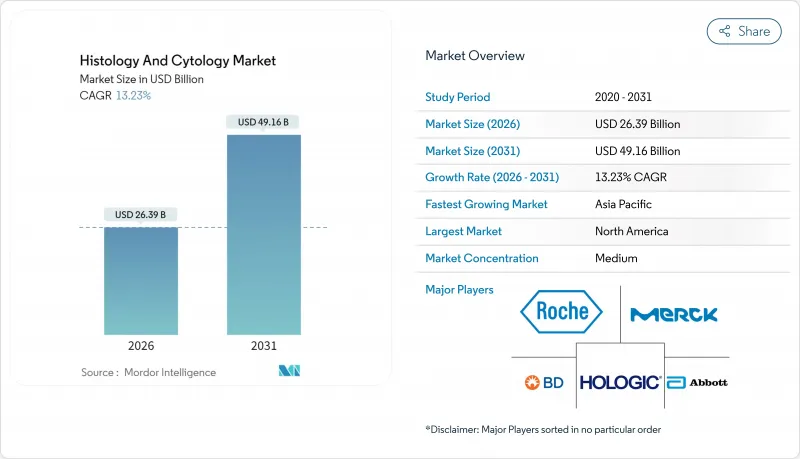

Histology And Cytology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The histology and cytology market is expected to grow from USD 23.31 billion in 2025 to USD 26.39 billion in 2026 and is forecast to reach USD 49.16 billion by 2031 at 13.23% CAGR over 2026-2031.

The acceleration arises from AI-enabled whole-slide imaging, liquid biopsy advances, and lab automation that together mitigate global pathologist shortages while meeting higher cancer-screening volumes and precision-medicine demands. Consumables and reagents continue to underpin revenues, yet cloud-hosted diagnostic services post the fastest gains as health systems favor variable-cost outsourcing over capital expenditure. Clinically, histology retains primacy for tissue staging, but cytology benefits from minimally invasive liquid-based methods that enable real-time tumor monitoring. Competitive intensity increases as leading manufacturers close strategic acquisitions that bundle scanners, reagents, and AI software into unified offerings. Regional growth divides along digital-readiness lines: North America leads on share, whereas Asia-Pacific's leapfrog adoption of automation generates the quickest incremental revenue.

Global Histology And Cytology Market Trends and Insights

AI-Enabled Whole-Slide Imaging Adoption

FDA-cleared scanners now digitize entire slides at diagnostic resolution, permitting cloud review that offsets workforce gaps and halves turnaround in high-volume centers. Academic-industry programs such as Danaher and Stanford's smart-microscopy venture generate additional revenue streams by pairing spatial biology with AI scoring algorithms. New CPT codes from the College of American Pathologists authorize billing for digital-workflow tasks, transforming previous cost centers into reimbursable services. European cost-effectiveness studies show that labs recoup capital outlays within six years by boosting throughput and enabling remote reads. The main adoption hurdle remains scanner prices of USD 50,000-300,000, so vendors explore subscription models that bundle hardware, software, and maintenance.

Rise in Companion Diagnostics for Oncology

Targeted-therapy pipelines rely on validated biomarker tests; Roche's PATHWAY HER2 assay for biliary-tract cancer illustrates first-mover advantages in niche indications. Flow-cytometry collaborations such as BD-Labcorp expand conventional cell-analysis platforms into treatment-selection tools. Thermo Fisher's myeloMATCH trial applies broad NGS panels to align patients with trials, accelerating enrollment and de-risking drug development. FDA approvals have quickened as assay-drug pairings demonstrate survival benefits, giving diagnostics firms defensible revenue backed by drug-label inclusion. The trend scales beyond oncology into autoimmune and infectious disease as therapeutics become biomarker-guided.

Shortage of Pathologists in Rural Regions

Only 3% of UK histopathology departments report adequate staffing, with 78% holding vacancies that delay diagnoses. U.S. surveys forecast 19.6% cytology retirements by 2027, outpacing training-program output. Telepathology can redistribute slides, yet broadband deficits and funding gaps limit reach. AI triage systems lessen manual load but still require human sign-out. Without policy incentives to relocate or train specialists, rural disparity persists, tempering growth of the histology and cytology market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Minimally Invasive Biopsies

- Rapid Lab Automation in Emerging Economies

- High Capital Cost of Digital Scanners

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Histology controlled 66.71% of 2025 revenue; however, cytology is surging at a 13.84% CAGR as laboratories embrace non-invasive liquid-biopsy protocols that provide serial monitoring without repeated excisions. This demand propels consumable usage, especially antigen-specific antibodies required for immunohistochemistry verification of circulating tumor cells. Cytology expansion also leverages AI-guided image analysis that accelerates Pap slide review and flags atypical cells for human confirmation. Laboratories thereby reallocate skilled staff toward complex differential diagnoses, raising overall productivity.

Cytology's ascent encourages vendors to integrate dual-modality scanners capable of both bright-field tissue and thin-layer cell imaging, maximizing equipment utilization. The histology and cytology market size attributed to cytology is forecast to expand fastest in outpatient women's-health clinics where cervical self-collection funnels higher sample volumes into centralized labs. Nonetheless, histology remains indispensable for surgical-margin assessment and in-situ architecture evaluation, ensuring continued reagent and microtome demand.

Consumables and reagents generated 47.77% of 2025 value as stains, antibodies, and RNA probes remain recurring necessities for every block or slide processed. The histology and cytology market size for this product class scales linearly with biopsy volumes, providing predictable revenue for reagent suppliers. Manufacturers differentiate by offering ready-to-use kits pre-optimized for digital scanners, minimizing manual adjustments.

Services, though smaller today, exhibit a 13.71% CAGR as providers deliver cloud-based slide digitization, AI scoring, and second-opinion consults. Outsourced models appeal to clinics lacking capital or personnel and enable 24-hour turnaround across time zones. Vendors bundle logistics, quality checks, and LIS integration, presenting compelling total-cost-of-ownership savings. Instrument sales plateau because extended hardware lifecycles and shared-use depots satisfy existing capacity, shifting supplier focus toward consumable pull-through and service annuities.

The Histology and Cytology Market Report Segments the Industry Into by Type of Examination (Histology, Cytology), by Test Type (Microscopy Tests, Molecular Genetics Tests, Flow Cytomtery), by End User (Hospitals and Clinics, Academic and Research Institutes, Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). Get Five Years of Historic Data and Five-Year Forecasts.

Geography Analysis

North America maintains 37.82% share thanks to robust reimbursement, widespread scanner approvals, and early AI-algorithm validation. Leading cancer centers conduct digital-first workflows, and multistate IDNs negotiate value-based contracts that reimburse performance metrics rather than per-slide fees. Nonetheless, rural understaffing persists, prompting telepathology networks that pool subspecialty expertise across state lines. Proposed 2026 Medicare fee reductions inject uncertainty, but private insurers offset risk by rewarding demonstrable accuracy gains.

Asia-Pacific posts the highest 13.78% CAGR, driven by China's nationwide cancer-screening expansion and India's public-private lab partnerships that deploy automated staining lines. Governments prioritize leapfrog technologies to bridge specialist gaps without replicating legacy infrastructure. Japanese vendors pilot end-to-end digital-pathology suites in local hospitals, combining high-speed scanners with natural-language pathology reporting. ASEAN regulatory harmonization eases device clearance, encouraging multinationals to site regional hubs that cut import duties and service delays.

Europe records steady growth anchored in collaborative research and strong data-privacy safeguards. Germany's hospital-modernization grants accelerate scanner procurement, and the UK's NHS Digital Pathology program scales teleconsultation across trusts. France and Italy foster public-academic alliances that commercialize AI de-identification pipelines compliant with GDPR. Brexit prompts UK firms to pursue dual registration in EMA and MHRA pathways, adding regulatory overhead but also opening flexibility for innovative trial designs. Overall adoption aligns with national e-health roadmaps, positioning Europe as a disciplined yet attractive market segment for vendors.

- Danaher Corp (Leica Biosystems)

- Thermo Fisher Scientific

- Roche

- Beckton Dickinson

- Abbott Laboratories

- Merck

- Agilent Technologies

- Hologic

- Sakura Finetek Japan Co., Ltd.

- 3DHistech

- Sysmex

- Koninklijke Philips

- Bio-Techne

- Cell Signaling Technology

- Biocare Medical

- Hamamatsu Photonics

- Olympus

- PerkinElmer

- Miltenyi Biotec B.V. & Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-enabled whole-slide imaging adoption

- 4.2.2 Rise in companion diagnostics for oncology

- 4.2.3 Growing demand for minimally-invasive biopsies

- 4.2.4 Rapid lab automation in emerging economies

- 4.2.5 Mainstream digital pathology reimbursements

- 4.2.6 Expansion of biobanking for personalized medicine

- 4.3 Market Restraints

- 4.3.1 Shortage of pathologists in rural regions

- 4.3.2 High capital cost of digital scanners

- 4.3.3 Data-privacy concerns for cloud pathology

- 4.3.4 Limited standardization of liquid-based cytology

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD Million)

- 5.1 By Technique

- 5.1.1 Histology

- 5.1.2 Cytology

- 5.2 By Product

- 5.2.1 Instruments

- 5.2.2 Consumables & Reagents

- 5.2.3 Services

- 5.3 By Test Type

- 5.3.1 Microscopy Tests

- 5.3.1.1 Cytogenic Tests

- 5.3.1.1.1 Karyotyping

- 5.3.1.1.2 Fluorescent In-situ Hybridization (FISH)

- 5.3.1.2 Polymerase Chain Reaction

- 5.3.1.3 Other Microscopy Tests

- 5.3.1.1 Cytogenic Tests

- 5.3.2 Molecular Genetics Tests

- 5.3.3 Flow Cytomtery

- 5.3.1 Microscopy Tests

- 5.4 By Application

- 5.4.1 Clinical Diagnostics

- 5.4.2 Drug Discovery & Development

- 5.4.3 Research

- 5.5 By End User

- 5.5.1 Hospitals & Diagnostic Labs

- 5.5.2 Academic & Research Institutes

- 5.5.3 Pharmaceutical & Biotechnology Companies

- 5.5.4 Contract Research Organizations (CROs)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 GCC

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Danaher Corp (Leica Biosystems)

- 6.3.2 Thermo Fisher Scientific Inc.

- 6.3.3 F. Hoffmann-La Roche Ltd.

- 6.3.4 Becton, Dickinson and Company

- 6.3.5 Abbott Laboratories

- 6.3.6 Merck KGaA

- 6.3.7 Agilent Technologies Inc.

- 6.3.8 Hologic Inc.

- 6.3.9 Sakura Finetek Japan Co., Ltd.

- 6.3.10 3DHISTECH Ltd.

- 6.3.11 Sysmex Corporation

- 6.3.12 Koninklijke Philips N.V.

- 6.3.13 Bio-Techne Corporation

- 6.3.14 Cell Signaling Technology, Inc.

- 6.3.15 Biocare Medical LLC

- 6.3.16 Hamamatsu Photonics K.K.

- 6.3.17 Olympus Corporation

- 6.3.18 PerkinElmer Inc.

- 6.3.19 Miltenyi Biotec B.V. & Co. KG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment