PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906079

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906079

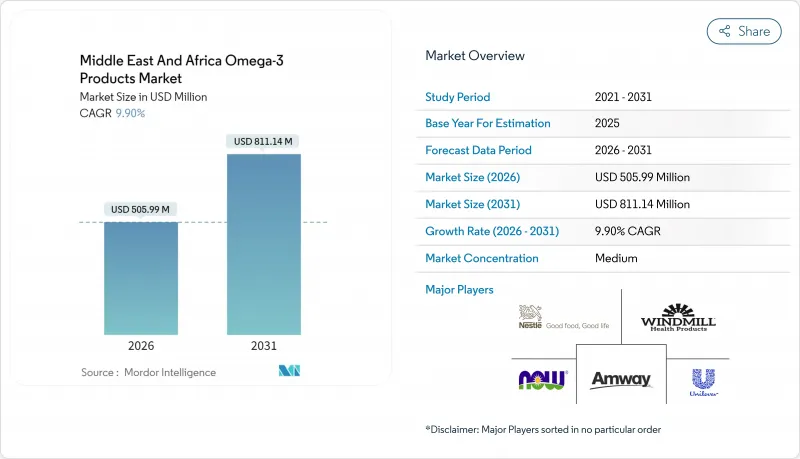

Middle East And Africa Omega-3 Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Middle East and Africa omega-3 products market size in 2026 is estimated at USD 505.99 million, growing from 2025 value of USD 460.41 million with 2031 projections showing USD 811.14 million, growing at 9.9% CAGR over 2026-2031.

This growth is driven by increasing cardiovascular health concerns, government regulations mandating food fortification, and growing consumption of fortified foods among urban youth. Multinational companies are increasing their regional production of concentrated algal-based omega-3 to address fish oil price volatility. Premium supplement manufacturers are expanding their presence in pharmacies through medical endorsements. E-commerce platforms are improving product accessibility, particularly in GCC countries, where smartphone penetration exceeds 95% and cross-border e-commerce infrastructure is well-developed. While market competition remains moderate, industry consolidation, exemplified by Louis Dreyfus Company's acquisition of BASF's Food and Health Performance Ingredients division, indicates increasing control over raw material supply and pricing mechanisms.

Middle East And Africa Omega-3 Products Market Trends and Insights

Government-backed DHA enrichment programs in prenatal and infant formula

Government regulations requiring DHA fortification in prenatal and infant nutrition products establish consistent institutional purchasing volumes, which stabilize market demand independently of consumer spending patterns. The Saudi Arabian Ministry of Health has incorporated omega-3 supplementation into its maternal healthcare protocols. At the same time, the Dubai Municipality in the United Arab Emirates enforces specific labeling requirements for DHA-enriched infant formulas. These regulatory requirements have established omega-3 as an essential nutritional component rather than a premium supplement, reducing price sensitivity and providing stable revenue streams for suppliers. The institutional purchasing channel enables bulk procurement agreements that enhance manufacturer profit margins while maintaining reliable supply to healthcare facilities. The implementation of these regulations has created a structured framework for quality control, standardization, and compliance monitoring across the healthcare system, further strengthening the market's foundation. Additionally, these mandates have encouraged research and development initiatives in DHA fortification technologies, leading to improved product formulations and delivery systems.

Regional algae-fermentation scale-ups enabling vegan supply

The establishment of algae fermentation facilities in the Middle East and Africa (MEA) region reduces dependence on fish oil imports and strengthens supply chain resilience against El Nino-related anchovy shortages, which have historically affected global omega-3 availability. The regional facilities provide a more sustainable and reliable source of omega-3 fatty acids, reducing the impact of global supply chain disruptions. DSM-Firmenich's life's DHA B54-0100 algal oil production requires a 25-day cultivation cycle, compared to 24-month fish oil sourcing timelines. This production method enables regional manufacturers to maintain stable pricing and availability, which is essential for halal-certified and vegan products in Muslim-majority markets. The shorter production cycle also allows manufacturers to respond more quickly to market demands and maintain consistent product quality. Local fermentation capacity also helps companies comply with strict import registration requirements across Gulf Cooperation Council (GCC) countries, while supporting the region's food security initiatives and economic diversification goals.

High raw material costs due to fish oil price volatility

Supply disruptions in Peruvian anchovy fisheries due to El Nino and reduced Moroccan sardine catches have led to significant fish oil price volatility in the market. According to the Global Organization for EPA and DHA Omega-3s, Peru's cancelled fishing seasons and 30-60% decline in Moroccan catches have created substantial supply shortages, compelling suppliers to prioritize existing customers over new market development. These supply constraints have resulted in manufacturers either absorbing reduced profit margins or implementing price increases. The impact is particularly pronounced in emerging markets across Egypt, Morocco, and Nigeria, where consumers have limited purchasing power to absorb higher prices, thus impeding market expansion and penetration in these price-sensitive regions. The ongoing supply chain challenges and price fluctuations continue to pose significant barriers to market growth in these developing economies.

Other drivers and restraints analyzed in the detailed report include:

- Rising prevalence of cardiovascular diseases and dyslipidemia

- Premiumization of supplements via high-concentrate fish oils

- Import-registration hurdles and inconsistent Gulf Cooperation Council countries (GCC) labelling rules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dietary supplements hold a dominant 55.32% market share in 2025, supported by strong consumer acceptance and premium positioning in affluent urban markets. The segment's growth is reinforced by pharmacy distribution networks and healthcare provider recommendations that influence consumer purchasing decisions. Functional food and beverages are projected to grow at a 10.65% CAGR through 2031, as food companies utilize fortification technologies to reach price-sensitive consumers who consider supplements discretionary purchases.

Infant nutrition maintains a stable market position, backed by government DHA enrichment initiatives and mandatory formula fortification regulations. Pharmaceutical applications, while limited in volume, command premium pricing through prescription sales and insurance coverage. The "Others" segment includes new applications in cosmetics and pet nutrition, indicating market expansion beyond traditional health uses. According to World Bank guidelines, DHA fortification in dairy and processed foods requires microencapsulation or powder formulations to prevent taste and texture alterations.

The Middle East and Africa Omega-3 Products Market is Segmented by Product Type (Dietary Supplements, Functional Food and Beverages, and More), by Source (Marine, Plant and Algae), by Distribution Channel (Grocery Retailers, Pharmacies and Drug Stores, and More), and by Geography (South Africa, United Arab Emirates, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- BASF SE

- DSM-Firmenich

- Croda International Plc

- GC Rieber VivoMega

- Golden Omega

- Epax Norway

- Cargill Health Technologies

- Orkla Health

- Abbott Laboratories

- Amway Nutrilite

- Herbalife Nutrition

- Unilever PLC

- NOW Health Group, Inc.-

- Windmill Health Products

- Nestle SA

- Reckitt (Mead Johnson EnfaDHA)

- Seven Seas Ltd.

- Nuseed Nutriterra

- Polaris SAS

- KD Pharma Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in fortified food and beverage launches by multinationals

- 4.2.2 Government-backed DHA enrichment programs in prenatal and infant formula

- 4.2.3 Regional algae-fermentation scale-ups enabling vegan supply

- 4.2.4 Rising prevalence of cardiovascular diseases and dyslipidemia

- 4.2.5 Premiumization of supplements via high-concentrate fish oils

- 4.2.6 Accelerating aging demographics increasing demand for omega-3 supplements

- 4.3 Market Restraints

- 4.3.1 High raw material costs due to fish oil price volatility

- 4.3.2 Import-registration hurdles and inconsistent Gulf Cooperation Council countries (GCC) labelling rules

- 4.3.3 Price-sensitive shift to cheaper alpha-linolenic acid (ALA) products

- 4.3.4 Stringent regulatory requirements for health claims and product approvals

- 4.4 Supply Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECAST (VALUE)

- 5.1 By Product Type

- 5.1.1 Dietary Supplements

- 5.1.2 Functional Food and Beverages

- 5.1.3 Infant Nutrition

- 5.1.4 Pharmaceuticals

- 5.1.5 Others

- 5.2 By Source

- 5.2.1 Marine

- 5.2.1.1 Fish

- 5.2.1.2 Krill

- 5.2.1.3 Others

- 5.2.2 Plant and Algae

- 5.2.1 Marine

- 5.3 By Distribution Channel

- 5.3.1 Grocery Retailers

- 5.3.2 Pharmacies and Drug Store

- 5.3.3 Online Retail Channel

- 5.3.4 Other Distribution Channels

- 5.4 Geography

- 5.4.1 South Africa

- 5.4.2 Saudi Arabia

- 5.4.3 United Arab Emirates

- 5.4.4 Nigeria

- 5.4.5 Egypt

- 5.4.6 Morocco

- 5.4.7 Turkey

- 5.4.8 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Positioning Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.3.1 BASF SE

- 6.3.2 DSM-Firmenich

- 6.3.3 Croda International Plc

- 6.3.4 GC Rieber VivoMega

- 6.3.5 Golden Omega

- 6.3.6 Epax Norway

- 6.3.7 Cargill Health Technologies

- 6.3.8 Orkla Health

- 6.3.9 Abbott Laboratories

- 6.3.10 Amway Nutrilite

- 6.3.11 Herbalife Nutrition

- 6.3.12 Unilever PLC

- 6.3.13 NOW Health Group, Inc.-

- 6.3.14 Windmill Health Products

- 6.3.15 Nestle SA

- 6.3.16 Reckitt (Mead Johnson EnfaDHA)

- 6.3.17 Seven Seas Ltd.

- 6.3.18 Nuseed Nutriterra

- 6.3.19 Polaris SAS

- 6.3.20 KD Pharma Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK