PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906101

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906101

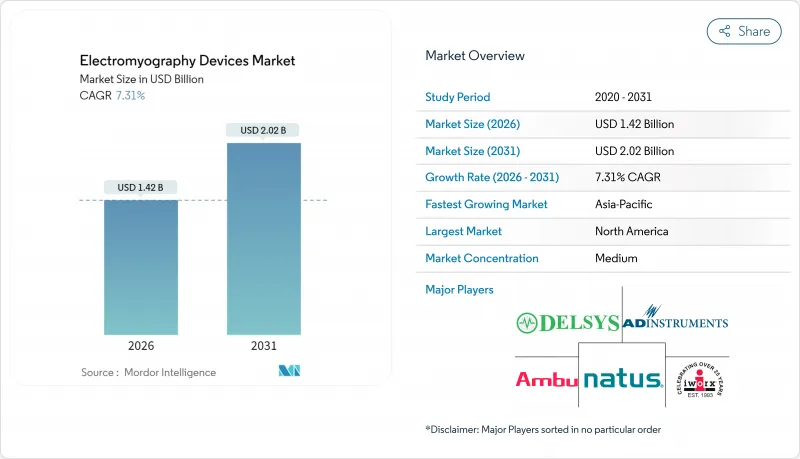

Electromyography Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Electromyography devices market size in 2026 is estimated at USD 1.42 billion, growing from 2025 value of USD 1.32 billion with 2031 projections showing USD 2.02 billion, growing at 7.31% CAGR over 2026-2031.

Demographic aging, broader clinical applications, and technological advances in wearable and AI-enabled systems collectively fuel this expansion. Rising neuromuscular disease prevalence sustains diagnostic demand, while miniaturized sensors and cloud analytics broaden use beyond hospital walls into rehabilitation, sports medicine, and home monitoring. Regulatory clearances for advanced devices shorten innovation cycles, and single-use electrode adoption mitigates infection risk, supporting provider uptake. Competitive strategies concentrate on integrated hardware-software platforms that deliver predictive insights and seamless workflows, positioning electromyography at the center of precision neuromuscular care.

Global Electromyography Devices Market Trends and Insights

Rising Prevalence of Neuromuscular Disorders and Aging Population

Rising life expectancy elevates the incidence of conditions such as amyotrophic lateral sclerosis and myasthenia gravis, raising diagnostic volumes across primary care and geriatric settings. EMG offers a cost-effective alternative to imaging for confirming neuromuscular impairment, and payers increasingly reimburse testing to manage long-term disability costs. Consistent demand, irrespective of economic cycles, stabilizes revenue for device suppliers while encouraging primary-care physicians to adopt point-of-care EMG solutions that shorten referral pathways and speed therapeutic intervention.

Technological Advances in Portable and Wearable EMG Devices

Miniaturized electronics and wireless connectivity now deliver clinical-grade accuracy in devices under 50 grams, enabling continuous monitoring during daily activity. Battery life exceeding 48 hours eliminates charging constraints, and on-board machine-learning filters remove artifacts, reducing specialist oversight. These features expand EMG into consumer wellness and sports performance arenas without compromising medical reliability. The shift also stimulates recurring revenue through companion software subscriptions that analyze longitudinal muscle data.

High Capital and Maintenance Cost of EMG Systems

Comprehensive platforms cost USD 50,000-USD 200,000 and demand annual service contracts near 12% of purchase price. Smaller facilities struggle to justify investment when reimbursement fails to cover total ownership costs. Infrastructure upgrades-shielded rooms, isolation transformers, and regular calibration-add to the burden. Consequently, EMG capacity clusters in tertiary hospitals, limiting access for patients outside metropolitan hubs.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption of Intra-operative Neuromonitoring

- AI-Enabled Real-Time EMG Analytics for Predictive Diagnostics

- Shortage of Trained Neurophysiologists and Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surface devices accounted for a 45.62% electromyography devices market share in 2025, underscoring their versatility across routine neuromuscular evaluations. The electromyography devices market size for surface devices continues to rise as clinicians trust established protocols and reimbursement is straightforward. Wearable systems, however, post the fastest 7.95% CAGR by delivering continuous, activity-based data that enrich rehabilitation and athletic performance programs.

Needle EMG remains indispensable for deep-muscle assessment, sustaining stable demand even as less invasive modalities grow. High-density arrays, once confined to academia, now attract specialty clinics analyzing complex movement disorders. FDA clearance of the Glide surface electrode system exemplifies regulatory endorsement of patient-friendly designs that enhance signal quality. Consumables drive recurring revenue: single-use dry electrodes reduce cross-infection risk and streamline workflow for physiotherapy centers. Infection-control studies report potential sepsis treatment costs of USD 33,718 per affected patient, making disposable solutions financially prudent. As outpatient volumes climb, electrode shipments will increasingly anchor supplier revenue.

Standalone configurations captured 38.25% of electromyography devices market share in 2025 and simultaneously posted an 8.22% CAGR, reflecting clinician preference for purpose-built systems offering optimized signal quality and intuitive workflows. Integrated EMG/EEG platforms find niche use in epilepsy and sleep clinics where simultaneous brain-muscle data inform diagnosis, yet design compromises can limit depth in either modality. FDA Class II device pathways also favor focused validation, simplifying approvals for single-purpose equipment. Hospitals value the reduced setup time and dedicated analysis software embedded in standalone units, which shortens exam cycles and increases daily throughput.

The Electromyography Devices Market Report is Segmented by Product Type (Surface EMG Devices, Needle EMG Devices, and More), Modality (Stand-Alone EMG Systems, Integrated EMG/EEG Systems), Application (Neuromuscular Disorder Diagnosis, Pain Management & Rehabilitation, and More), End User (Hospitals, Specialty Clinics, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America combines 27.95% market share with a dense specialist network and payer support for diagnostic EMG procedures. Commercial insurers reimburse standard tests, yet classify some sports-related surface studies as investigational, tempering segment expansion. FDA pathways expedite device upgrade cycles, but rural shortages of neurophysiologists persist, slowing penetration beyond urban centers.

Asia-Pacific registers the fastest 9.12% CAGR through targeted public-health budgets and private investment in diagnostic capability. China expands tertiary-care hospitals while encouraging domestic device manufacturing to curb import reliance. Japan's advanced aging boosts electromyography volumes, and national reimbursement lists endorse high-precision testing. India's mid-tier hospitals demand cost-efficient systems that deliver acceptable performance without the premium features favored in wealthier markets. Local assembly and flexible financing help suppliers compete.

Europe maintains consistent growth under unified MDR certification that simplifies cross-border distribution. GDPR compliance imposes rigorous data-security controls, prompting vendors to embed encryption, user consent, and regional hosting options. Germany, France, and the United Kingdom lead uptake due to mature neurology services, while Eastern Europe sees gradual adoption as EU structural funds modernize healthcare. South America and Middle East/Africa open new sales channels as government-hospital partnerships deploy mobile EMG labs to underserved communities.

- Abbott Laboratories

- Cadwell

- Cometa Systems srl

- Compumedics Ltd.

- G.Tec Medical Engineering GmbH

- Inomed Medizintechnik

- Medtronic

- Natus Medical

- NeuroMetrix

- Neurosoft LLC

- Nihon Kohden

- Noraxon USA, Inc.

- OT Bioelettronica Srl

- Plexon Inc.

- TMSi (Artinis Medical Systems BV)

- Delsys

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising prevalence of neuromuscular disorders and ageing population

- 4.2.2 Technological advances in portable & wearable EMG devices

- 4.2.3 Growing adoption of intra-operative neuromonitoring

- 4.2.4 AI-enabled real-time EMG analytics for predictive diagnostics

- 4.2.5 Surge in low-cost single-use dry electrodes for physiotherapy clinics

- 4.3 Market Restraints

- 4.3.1 High capital & maintenance cost of EMG systems

- 4.3.2 Shortage of trained neurophysiologists & technicians

- 4.3.3 Data-privacy concerns around cloud-based EMG platforms

- 4.3.4 Limited reimbursement for sports-medicine EMG assessments

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Surface EMG Devices

- 5.1.2 Needle EMG Devices

- 5.1.3 Wearable / Portable EMG Systems

- 5.1.4 High-Density EMG Systems

- 5.1.5 EMG Electrodes & Accessories

- 5.2 By Modality

- 5.2.1 Stand-alone EMG Systems

- 5.2.2 Integrated EMG/EEG Systems

- 5.3 By Application

- 5.3.1 Neuromuscular Disorder Diagnosis

- 5.3.2 Pain Management & Rehabilitation

- 5.3.3 Orthopedics & Sports Medicine

- 5.3.4 Intraoperative Monitoring

- 5.3.5 Research & Academia

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Specialty Clinics

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Sports Rehabilitation Centers

- 5.4.5 Academic & Research Institutes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Cadwell Industries Inc.

- 6.3.3 Cometa Systems srl

- 6.3.4 Compumedics Ltd.

- 6.3.5 G.Tec Medical Engineering GmbH

- 6.3.6 Inomed Medizintechnik GmbH

- 6.3.7 Medtronic plc

- 6.3.8 Natus Medical Incorporated

- 6.3.9 NeuroMetrix, Inc.

- 6.3.10 Neurosoft LLC

- 6.3.11 Nihon Kohden Corporation

- 6.3.12 Noraxon USA, Inc.

- 6.3.13 OT Bioelettronica Srl

- 6.3.14 Plexon Inc.

- 6.3.15 TMSi (Artinis Medical Systems BV)

- 6.3.16 Delsys

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment