PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906111

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906111

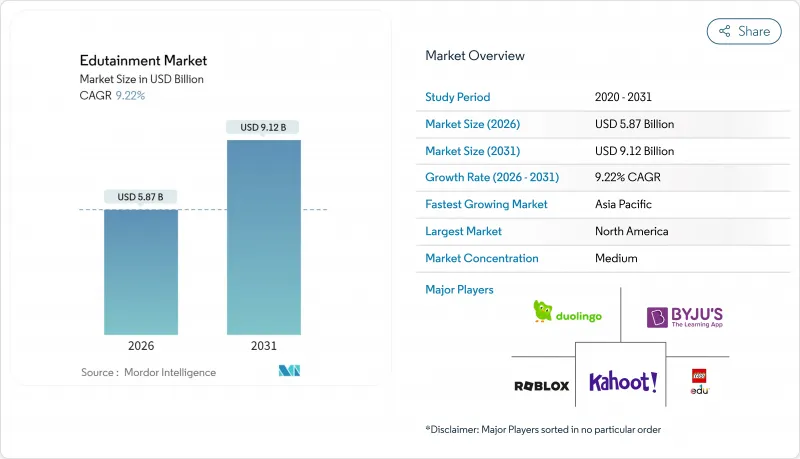

Edutainment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The edutainment market was valued at USD 5.37 billion in 2025 and estimated to grow from USD 5.87 billion in 2026 to reach USD 9.12 billion by 2031, at a CAGR of 9.22% during the forecast period (2026-2031).

This measured growth reflects a maturing landscape in which established platforms consolidate user bases while emerging technologies such as 5G and augmented reality transform content delivery. Interactive products continue to attract the largest daily active user pools, yet hybrid formats that meld game mechanics with structured instruction are scaling rapidly. Mobile apps dominate distribution thanks to global 5G roll-outs that enable real-time, multiplayer learning sessions, while corporate purchasers expand spending on immersive soft-skill up-skilling modules. The edutainment market is also shaped by intensifying regulatory scrutiny over children's data privacy, favoring companies that can balance engagement with compliance. Meanwhile, falling content-production costs from generative-AI authoring tools widen entry paths for niche providers and regional specialists.

Global Edutainment Market Trends and Insights

5G-Enabled Mobile Micro-Learning Boom

Ultra-low latency networks transform educational content delivery by enabling real-time collaborative experiences that previously required desktop computing power. 5G infrastructure deployment reached 85% population coverage across major metropolitan areas in 2024, reducing content buffering delays that historically disrupted immersive learning sessions . The technology's impact extends beyond faster downloads to support augmented reality applications that overlay contextual information onto physical environments, creating location-based learning opportunities in museums, retail spaces, and outdoor settings. Corporate training programs increasingly leverage 5G-enabled mobile devices for just-in-time skill development, allowing employees to access procedural guidance during actual work tasks rather than separate training sessions. This shift toward ambient learning integration represents a fundamental departure from scheduled educational activities toward continuous capability enhancement embedded within daily workflows.

Rapid Adoption of Gamified Language-Learning Apps

Behavioral psychology research demonstrates that variable reward schedules in gamified applications generate higher user retention rates than traditional educational software, with daily active usage increasing 40-60% when competitive elements and social features are integrated. Duolingo's streak mechanics and league competitions drove 51% growth in daily active users during 2024, demonstrating how game design principles sustain long-term engagement beyond initial novelty periods . The success of language learning applications creates template opportunities for other subject areas, as mathematics and science educators adopt similar progression systems, achievement badges, and peer comparison features. Revenue models benefit from this engagement pattern, as sustained daily usage increases conversion rates from free to premium subscriptions while generating advertising inventory for supplementary monetization streams.

Fragmented Curriculum Standards Slowing Procurement

Educational content must align with diverse state, provincial, and national curriculum frameworks, creating development costs that scale exponentially with geographic market expansion. The United States maintains 50 different state education standards alongside Common Core adoption variations, while European Union countries implement 27 distinct national curricula that resist harmonization efforts. Content localization requirements extend beyond language translation to encompass cultural references, historical perspectives, and pedagogical approaches that reflect regional educational philosophies. This fragmentation prevents economies of scale in content production and forces companies to choose between broad market coverage with generic materials or deep market penetration with customized offerings that limit scalability potential.

Other drivers and restraints analyzed in the detailed report include:

- Government STEM Mandates in K-12 Curricula

- Corporate Up-Skilling Budgets for Immersive Soft-Skills

- High Upfront AR/VR Hardware Costs in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Interactive products maintain a 47.05% market share in 2025, reflecting sustained demand for gamified learning experiences that combine entertainment mechanics with educational objectives. Hybrid solutions demonstrate the fastest growth at 18.11% CAGR through 2031, as content creators blend interactive elements with traditional instructional videos and assessment tools to maximize engagement across diverse learning preferences. The hybrid approach addresses institutional concerns about screen time limitations while preserving the motivational benefits of game-based learning through carefully balanced content portfolios. Non-interactive products retain relevance in formal educational settings where curriculum compliance requires structured presentation of information, though their static nature limits user engagement compared to dynamic alternatives.

Explorative products represent emerging opportunities as virtual field trips and simulation-based learning gain acceptance among educators seeking authentic experiential learning without logistical constraints. The COVID-19 pandemic accelerated the adoption of virtual laboratory experiences and historical site tours, creating precedents for immersive educational content that transcends physical limitations. Generative AI tools increasingly support hybrid product development by automating content adaptation across different interaction modes, reducing production costs while maintaining pedagogical effectiveness across varied learning contexts.

The Edutainment Market Report is Segmented by Product Type (Interactive, Non-Interactive, Hybrid, Explorative), End-Use Age Group (Children, Teenagers, Young Adults, Adults), Platform (Mobile Apps, PC/Console, Web-Based, AR/VR, TV/Streaming), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintains 33.10% market share in 2025, supported by established educational technology infrastructure and corporate training budgets that prioritize employee development investments. Asia-Pacific demonstrates the fastest regional growth at 10.21% CAGR, driven by government digitization initiatives, expanding middle-class populations, and mobile-first technology adoption patterns that bypass traditional computing infrastructure. European markets emphasize data privacy compliance and pedagogical research validation, creating higher barriers to entry but also premium pricing opportunities for solutions that meet stringent regulatory requirements.

Middle East and Africa represent emerging opportunities as internet connectivity improves and government education investments increase, though economic volatility and infrastructure limitations constrain near-term growth potential. South America benefits from Spanish and Portuguese language content localization efforts by global platforms, while regional content creators develop culturally relevant educational materials that address local curriculum requirements and learning preferences. The geographic distribution reflects varying stages of digital transformation rather than inherent market size limitations, suggesting convergence potential as infrastructure development progresses across emerging economies.

- Duolingo

- BYJU'S

- Kahoot!

- Roblox Corporation

- LEGO Education

- Coursera

- Osmo (Tangible Play)

- Adventure Academy (Age of Learning)

- Code.org

- Prodigy Education

- BBC Bitesize

- Sesame Workshop

- KidZania

- Disney Imagicademy

- Quizizz

- Kahoot DragonBox

- Labster

- Google for Education

- Microsoft Minecraft Education

- GooseChase

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G-enabled mobile micro-learning boom

- 4.2.2 Rapid adoption of gamified language-learning apps

- 4.2.3 Government STEM mandates in K-12 curricula

- 4.2.4 Corporate up-skilling budgets for immersive soft-skills

- 4.2.5 Edutainment IP extensions by global entertainment studios

- 4.2.6 Generative-AI tools slashing content-production costs

- 4.3 Market Restraints

- 4.3.1 Fragmented curriculum standards slowing procurement

- 4.3.2 Screen-time health concerns prompting regulatory scrutiny

- 4.3.3 High upfront AR/VR hardware costs in emerging markets

- 4.3.4 Teacher training gaps for interactive pedagogy

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Interactive

- 5.1.2 Non-Interactive

- 5.1.3 Hybrid

- 5.1.4 Explorative

- 5.2 By End-Use Age Group

- 5.2.1 Children

- 5.2.2 Teenagers

- 5.2.3 Young Adults

- 5.2.4 Adults

- 5.3 By Platform

- 5.3.1 Mobile Apps

- 5.3.2 PC / Console

- 5.3.3 Web-based

- 5.3.4 AR / VR

- 5.3.5 TV / Streaming

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 BENELUX

- 5.4.3.6.1 Belgium

- 5.4.3.6.2 Netherlands

- 5.4.3.6.3 Luxembourg

- 5.4.3.7 NORDICS

- 5.4.3.7.1 Denmark

- 5.4.3.7.2 Finland

- 5.4.3.7.3 Iceland

- 5.4.3.7.4 Norway

- 5.4.3.7.5 Sweden

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 India

- 5.4.4.2 China

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 South East Asia

- 5.4.4.6.1 Singapore

- 5.4.4.6.2 Malaysia

- 5.4.4.6.3 Thailand

- 5.4.4.6.4 Indonesia

- 5.4.4.6.5 Vietnam

- 5.4.4.6.6 Philippines

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Duolingo

- 6.4.2 BYJU'S

- 6.4.3 Kahoot!

- 6.4.4 Roblox Corporation

- 6.4.5 LEGO Education

- 6.4.6 Coursera

- 6.4.7 Osmo (Tangible Play)

- 6.4.8 Adventure Academy (Age of Learning)

- 6.4.9 Code.org

- 6.4.10 Prodigy Education

- 6.4.11 BBC Bitesize

- 6.4.12 Sesame Workshop

- 6.4.13 KidZania

- 6.4.14 Disney Imagicademy

- 6.4.15 Quizizz

- 6.4.16 Kahoot DragonBox

- 6.4.17 Labster

- 6.4.18 Google for Education

- 6.4.19 Microsoft Minecraft Education

- 6.4.20 GooseChase

7 Market Opportunities & Future Outlook

- 7.1 AI-generated adaptive story-worlds for language immersion

- 7.2 Location-based XR learning arcs in shopping-mall FECs