PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906142

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906142

Polymer Coated Fabric - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

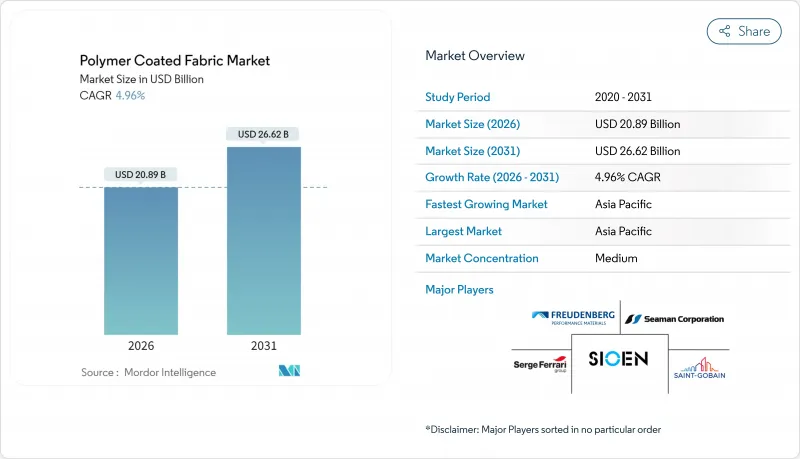

Polymer Coated Fabric Market size in 2026 is estimated at USD 20.89 billion, growing from 2025 value of USD 19.90 billion with 2031 projections showing USD 26.62 billion, growing at 4.96% CAGR over 2026-2031.

The outlook mirrors sustained investments in lightweight, high-performance materials that meet decarbonization targets while complying with more stringent chemical regulations. Demand consolidation in transportation interiors, protective clothing, and climate-resilient construction keeps the polymer coated fabric market on a steady growth track. Producers leverage coating chemistries that fuse durability with recyclability, allowing end-users to meet lifecycle cost and disclosure mandates. Competitive intensity remains moderate, yet strategic acquisitions, regional capacity expansion, and PFAS-free innovation sharpen differentiation across product lines.

Global Polymer Coated Fabric Market Trends and Insights

Investments in Flexible Photovoltaic Back-Sheet Fabrics

Solar-rich economies champion fabric-based photovoltaics that conform to curved or lightweight structures. PTFE-coated glass fiber substrates deliver weather tolerance and enable 20-25-year operating life of flexible modules, accelerating adoption in building-integrated solar facades. Chinese textile-solar synergies underpin commercial scale, while EU architects specify low-mass solar membranes to meet net-zero building codes.

Increasing Demand for Lightweight, Sustainable Interior Materials

Automotive and aerospace OEMs see 15-20% weight savings when polymer coated fabrics replace heavier substrates, translating directly to fuel efficiency gains. Continental AG integrates rice-husk silica and natural rubber into its coated fabric range, demonstrating how renewable fillers meet durability specifications without cost penalties.

Supply-Chain Localization Disrupting Global Trade Flows

Geopolitical tensions spur regionalized production, raising capital needs for duplicate coating lines across continents and compressing economies of scale. U.S. buyers diversify sourcing toward India and Southeast Asia to mitigate tariff exposure.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Protective-Clothing Standards Across APAC Manufacturing

- Adoption of Antimicrobial Coatings in Healthcare Furnishings

- Environmental Scrutiny of PVC and Phthalates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PVC held 41.55% polymer-coated fabric market share in 2025, reflecting entrenched cost and processing advantages. Polyurethane, however, is projected to post a 5.88% CAGR to 2031 as converters adapt to phthalate restrictions and recyclability mandates. Lubrizol's ESTANE RNW TPU offers a 59% lower carbon footprint while maintaining abrasion resistance, illustrating how greener chemistries transition from niche to mainstream.

Silicone and polyethylene retain specialized roles in extreme-temperature or chemically inert uses, whereas bio-based hybrids gain traction in consumer electronics casings and luxury accessories. Technological roadmaps reveal that leading suppliers pair coating innovation with substrate engineering. Freudenberg's fine-filament spunbond supports thinner, lighter membranes, lowering solvent uptake and boosting coating line throughput. This integrated approach underscores how performance gains derive from both polymer advances and fabric architecture.

The Polymer Coated Fabric Report is Segmented by Product Type (PVC (Polyvinyl Chloride), Polyurethane (PU), Polyethylene, and Others), Application (Transportation, Industrial Equipment Covers, Roofing and Awning, Protective Clothing, Furniture, Sports and Leisure, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 46.10% polymer-coated fabric market share in 2025 and is projected to register a 5.72% CAGR through 2031. India's Textile Mission, backed by USD 629 million in 2025 budget allocations, earmarks funds for technical-textile research and development and pilot coating facilities. Public infrastructure programs, from metro rail to flood-resilient roofing, convert this capacity into sustained coated fabric off-take.

North America secures a technology-driven niche where aerospace and medical OEMs demand low-VOC, PFAS-free materials. Reshoring of electric-vehicle production amplifies local sourcing for seat fabrics and battery-pack covers. The polymer-coated fabric market sees suppliers investing in U.S. greenfield plants built for carbon-neutral operation, as evidenced by Trelleborg's Rutherford County project, slated for LEED certification

Europe remains a regulation-led market incubating solvent-free, waterborne coatings aligned with the Industrial Emissions Directive. OEM preference for full material disclosure favors certified suppliers, creating price resilience for high-compliance products. Middle East and Africa, though smaller, post above-average growth on the back of climate-resilient construction in the Gulf and industrial diversification in South Africa. Limited domestic coating lines present outsourcing opportunities for incumbents willing to invest in regional service hubs.

- Continental AG

- Cooley Group

- Freudenberg Performance Materials Holding GmbH

- Heytex Gruppe

- OMNOVA North America Inc.

- Saint-Gobain

- Seaman Corporation

- Serge Ferrari Group

- Sioen Industries NV

- SPRADLING INTERNATIONAL GmbH

- SRF Limited

- Trelleborg AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Lightweight, Sustainable Interior Materials

- 4.2.2 Growth in Protective-Clothing Standards Across APAC Manufacturing

- 4.2.3 Surge in Architectural Tensile Structures for Climate-Resilient Infrastructure

- 4.2.4 Adoption of Antimicrobial Coatings in Healthcare Furnishings

- 4.2.5 Investments in Flexible PV Back-Sheet Fabrics

- 4.3 Market Restraints

- 4.3.1 Volatility of Crude-Derived Polymer Prices

- 4.3.2 Environmental Scrutiny of PVC and Phthalates

- 4.3.3 Supply-Chain Localization Disrupting Global Trade Flows

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 PVC (Polyvinyl Chloride)

- 5.1.2 PU (Polyurethane)

- 5.1.3 Polyethylene

- 5.1.4 Silicone

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Transportation

- 5.2.2 Industrial Equipment Covers

- 5.2.3 Roofing and Awning

- 5.2.4 Protective Clothing

- 5.2.5 Furniture

- 5.2.6 Sports and Leisure

- 5.2.7 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Continental AG

- 6.4.2 Cooley Group

- 6.4.3 Freudenberg Performance Materials Holding GmbH

- 6.4.4 Heytex Gruppe

- 6.4.5 OMNOVA North America Inc.

- 6.4.6 Saint-Gobain

- 6.4.7 Seaman Corporation

- 6.4.8 Serge Ferrari Group

- 6.4.9 Sioen Industries NV

- 6.4.10 SPRADLING INTERNATIONAL GmbH

- 6.4.11 SRF Limited

- 6.4.12 Trelleborg AB

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment