PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906143

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906143

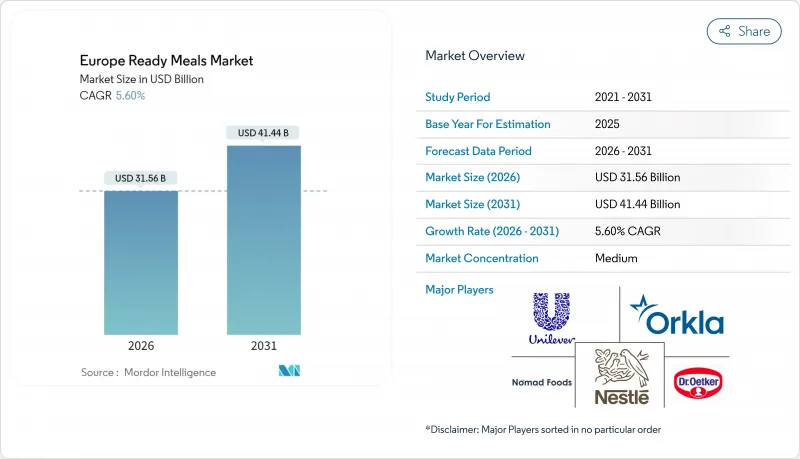

Europe Ready Meals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe ready meals market is expected to grow from USD 29.89 billion in 2025 to USD 31.56 billion in 2026 and is forecast to reach USD 41.44 billion by 2031 at 5.6% CAGR over 2026-2031.

The market's expansion reflects fundamental changes in European consumer behavior, with busy professionals and families increasingly seeking convenient meal solutions. The implementation of Europe Regulation 2025/40 on recyclable packaging is reshaping manufacturers' operational costs, while the moderation in food inflation to 2.4-4.9% enables companies to maintain more stable pricing strategies. The market benefits from several demographic shifts, including the continued trend of urbanization, the ongoing reduction in average household sizes, and the sustained increase in female workforce participation - factors that collectively strengthen the demand for quality, pre-portioned meals. The competitive environment continues to evolve as established food manufacturers leverage their extensive supply chain networks and distribution capabilities, while innovative start-ups address emerging consumer preferences for plant-based options, personalized nutrition, and sustainable products. The growth of digital platforms, especially quick-commerce applications, has created new distribution channels, particularly resonating with millennial and Gen Z consumers who prioritize convenience and immediate delivery options.

Europe Ready Meals Market Trends and Insights

Rising Trend of On-the-Go Consumption Demanding Convenience and Portability

Changes in European consumer mobility patterns are fundamentally reshaping how individuals structure their daily meal consumption, creating a robust and growing market for portable ready meal solutions. According to the Agriculture and Horticulture Development Board's comprehensive research, ready meals now represent 41% of red meat convenience products, demonstrating resilient market performance despite volume decreases in traditional food categories . This transformation reflects a significant evolution in consumer behavior, where conventional fixed mealtimes are transitioning to flexible eating patterns that accommodate modern professional schedules and daily commuting requirements. The ongoing urbanization and increasing population density across major European cities further amplify this market dynamic, as residents adapt to smaller living spaces that limit cooking capabilities while managing extended commuting hours between residential and workplace locations. The concurrent demographic shifts of an aging population combined with high workforce participation rates have elevated convenience foods from an occasional choice to an essential component of daily life for many European consumers.

Innovations in Product Formats, Flavors, and Nutritional Profiles

Product innovation cycles are accelerating as manufacturers work to meet stringent regulatory requirements while adapting to sophisticated consumer preferences. The establishment of Nomad Foods' Future Foods Lab in June 2025 exemplifies how traditional food companies are building strategic partnerships with startups to harness innovative technologies and gain deeper consumer behavior insights. Recent developments in freeze-dried technology have enabled manufacturers to produce shelf-stable products that deliver fresh, authentic taste experiences, effectively addressing consumer concerns about processed food quality without compromising on convenience. Ready meal manufacturers are diversifying their product portfolios by integrating authentic regional flavors and diverse ethnic cuisines, helping them expand their market presence beyond conventional European taste preferences. Through the strategic incorporation of functional ingredients, manufacturers are transforming ready meals into nutritionally beneficial options, positioning them as wholesome dietary choices rather than mere convenience alternatives.

Increased Consumer Demand for Freshly Prepared Meals

European consumers demonstrate a strong inclination toward fresh food options over ready meals, primarily driven by their emphasis on nutritional benefits and superior taste experiences. The growing trend of home cooking has become deeply ingrained in consumer behavior, with many households developing and maintaining regular meal preparation routines. Markets with rich culinary heritage, particularly France, Italy, and Spain, exhibit notable resistance to ready meal adoption, as their deeply rooted food traditions and communal dining practices create natural barriers to convenience food acceptance. The gradual stabilization of food prices has enabled consumers to redirect their spending toward fresh ingredients, moving away from processed alternatives. This shift in consumer preference particularly impacts the premium ready meal segment, as improved household purchasing power makes fresh food alternatives increasingly accessible and appealing.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Personalized Meal Options

- Advances in Packaging Technology Enhancing Shelf Life and Sustainability

- Regulatory Challenges Related to Food Labeling, Health Claims, and Safety Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The freeze-dried segment demonstrates significant market potential, growing at a 5.78% CAGR through 2031. This growth trajectory positions freeze-dried products as a notable challenger to the well-established Frozen Ready Meals segment, which currently commands a substantial 39.78% market share in 2025. The freeze-dried preservation method delivers extended shelf stability without the need for refrigeration, enabling companies to expand their distribution networks and reduce cold chain expenses while maintaining the nutritional content and taste quality of their products.

Frozen Ready Meals continue to maintain their market leadership position through strong consumer acceptance and an optimized retail infrastructure. Their competitive pricing structure makes these products accessible to consumers across various income levels. In contrast, Chilled Ready Meals occupy the premium market segment, offering products with shorter shelf life but perceived higher quality. This premium positioning attracts consumers who prioritize fresh-like characteristics and are willing to pay higher prices for such attributes.

The free-form ingredients market continues to demonstrate robust growth, advancing at a 6.05% CAGR through 2031. This expansion is primarily fueled by increasing consumer awareness and demand for products with clean labels and allergen-free formulations. In contrast, conventional ingredients maintain their strong market position with an 82.05% share in 2025, supported by their inherent cost advantages and well-established supply chain networks. The BMEL Food Report 2024 highlights a significant shift in consumer preferences, with more than half of consumers actively seeking processed foods containing reduced sugar and fat content.

This evolving consumer behavior has prompted manufacturers to undertake extensive reformulation efforts across both conventional and free-form categories. Free-form products successfully maintain premium pricing strategies, justified by their health-focused positioning and specialized manufacturing processes that eliminate common allergens and artificial additives. Meanwhile, conventional ingredients continue to dominate the market through their ability to leverage economies of scale, long-standing supplier relationships, and broad consumer familiarity that minimizes the need for extensive market education.

The Europe Ready Meals Market Report is Segmented by Type (Frozen Ready Meals, Chilled Ready Meals and More), Ingredients (Conventional and Free-Form), Category (Vegetarian and Non-Vegetarian), Distribution Channel (Supermarkets/Hypermarkets, Convenience/Grocery Stores and More) and Geography (United Kingdom, Germany, France, Italy, Spain and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Nomad Foods Ltd.

- Nestle S.A.

- Dr. Oetker GmbH

- Unilever PLC

- Orkla ASA

- Kerry Group plc

- Fjordland AS

- Saarioinen Oy

- VegMe AB

- Bell Food Group AG

- Greencore Group plc

- Bakkavor Group plc

- 2 Sisters Food Group

- Fresh Food Group (Di Luca)

- Delhaize Ready Meals

- Pladis Foods Ready Meals

- Frosta AG

- Iceland Foods Ltd

- Schafer's Fertiggerichte

- Apetito AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising trend of on-the-go consumption demanding convenience and portability

- 4.2.2 Innovations in product formats, flavors, and nutritional profiles

- 4.2.3 Expansion of personalized meal options

- 4.2.4 Advances in packaging technology enhancing shelf life and sustainability

- 4.2.5 Growing consumer acceptance of free-from and functional food claims

- 4.2.6 Increasing penetration of online grocery shopping and e-commerce platforms

- 4.3 Market Restraints

- 4.3.1 Increased consumer demand for freshly prepared meals

- 4.3.2 Regulatory challenges related to food labeling, health claims, and safety standards

- 4.3.3 Environmental concerns over plastic and non-biodegradable packaging

- 4.3.4 Challenges in maintaining consistent taste and quality across product lines

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Frozen Ready Meals

- 5.1.2 Chilled Ready Meals

- 5.1.3 Shelf-Stable Ready Meals

- 5.1.4 Freeze-Dried Ready Meals

- 5.2 By Ingredient

- 5.2.1 Conventional

- 5.2.2 Free-Form

- 5.3 By Category

- 5.3.1 Vegetarian

- 5.3.2 Non-Vegetarian

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Convenience/Grocery Stores

- 5.4.3 Online Retail Stores

- 5.4.4 Other Distribution Channel

- 5.5 By Geography

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 Italy

- 5.5.4 France

- 5.5.5 Spain

- 5.5.6 Netherlands

- 5.5.7 Poland

- 5.5.8 Belgium

- 5.5.9 Sweden

- 5.5.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nomad Foods Ltd.

- 6.4.2 Nestle S.A.

- 6.4.3 Dr. Oetker GmbH

- 6.4.4 Unilever PLC

- 6.4.5 Orkla ASA

- 6.4.6 Kerry Group plc

- 6.4.7 Fjordland AS

- 6.4.8 Saarioinen Oy

- 6.4.9 VegMe AB

- 6.4.10 Bell Food Group AG

- 6.4.11 Greencore Group plc

- 6.4.12 Bakkavor Group plc

- 6.4.13 2 Sisters Food Group

- 6.4.14 Fresh Food Group (Di Luca)

- 6.4.15 Delhaize Ready Meals

- 6.4.16 Pladis Foods Ready Meals

- 6.4.17 Frosta AG

- 6.4.18 Iceland Foods Ltd

- 6.4.19 Schafer's Fertiggerichte

- 6.4.20 Apetito AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK