PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906179

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906179

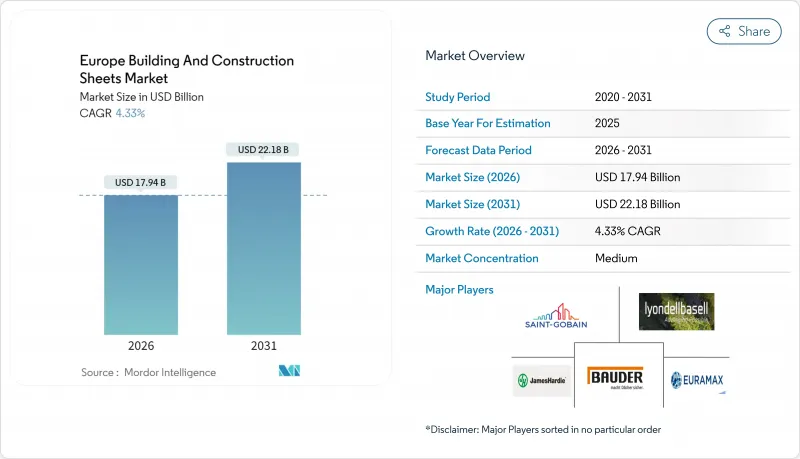

Europe Building And Construction Sheets - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe Building & Construction Sheets Market size in 2026 is estimated at USD 17.94 billion, growing from 2025 value of USD 17.2 billion with 2031 projections showing USD 22.18 billion, growing at 4.33% CAGR over 2026-2031.

This outlook underscores the market's durability in a volatile macro environment and its alignment with European Union climate directives that mandate zero-emission buildings by 2030. Regulatory pressure is redirecting specifications toward sheets that combine structural performance with solar harvesting or enhanced thermal insulation. Simultaneously, USD 156.23 billion in annual public funding is stimulating demand for renovation-focused sheet systems, while the fast-rising data-centre sector and modular construction practices are widening commercial opportunities. Intensifying consolidation, particularly among suppliers that fuse digital monitoring with low-carbon production, is reshaping competitive dynamics across the Europe building construction sheets market.

Europe Building And Construction Sheets Market Trends and Insights

Stricter Energy-Efficiency Regulations for Building Envelopes

The European building and construction sheets market is undergoing a significant transformation driven by stringent regulations and sustainability goals. Under the revised Energy Performance of Buildings Directive, member states must achieve zero-emission building status by 2030. This mandate pushes specifiers to prioritize sheets that combine structural strength with high thermal resistance or photovoltaic layers. Additionally, life-cycle warming potential assessments, also due by 2030, are driving up the demand for recycled inputs and low-carbon manufacturing. Germany is making a significant move with its USD 520.78 billion climate fund, dedicating at least USD 104.15 billion to decarbonizing construction, which in turn amplifies volume requirements. This legislative momentum is boosting premium pricing and intensifying R&D efforts in the market. Suppliers with certified low embodied-carbon footprints are now securing preferred-bidder status on public projects, positioning themselves for long-term growth opportunities.

Expanded Public Funding for Renovation Programmes

The Europe building construction sheets market is witnessing significant growth, driven by increasing investments in energy-efficient retrofits. Annual EU grants of USD 156.23 billion are driving energy retrofits, upgrading facades, roofs, and cladding systems without major structural changes. Spain's National Energy Efficiency Fund allocates USD 380 million annually, prioritising vulnerable households and underperforming buildings. This focus leans towards cost-effective polymer and hybrid sheets, ensuring tangible kilowatt-hour savings. France has reintroduced zero-interest loans and tax breaks for energy-efficient upgrades, boosting demand even as new construction activity slows. Financing guidelines mandate verifiable performance, leading builders to opt for smart sheets with integrated sensors that provide real-time thermal data. These factors collectively sustain the demand for specialised renovation-grade products in the region.

Volatile Energy Prices Elevating Production Costs

The Europe building and construction sheets market is currently navigating challenges stemming from energy price volatility and regulatory pressures. While wholesale gas rates have retreated from their 2023 highs, electricity tariffs for manufacturers remain above historical averages, squeezing profit margins for steel, aluminium, and polymer sheet producers. The potential extension of the EU Emissions Trading System is further elevating carbon costs, particularly for blast-furnace operations. Companies are adopting on-site solar solutions and power-purchase agreements to mitigate these challenges, but these require significant capital investments and lengthy permitting processes. Cost inflation is also impacting project bids, causing delays in award cycles or material substitutions. Despite these hurdles, the market is expected to stabilize as firms adapt to evolving energy and regulatory landscapes.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Data-Centre Construction Increasing Demand for Structural Decking

- Rising Adoption of Modular and Off-Site Construction Methods

- Shortage of Skilled Installation Labour

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal sheets secured 32.65% of 2025 revenue, reinforcing their status as the structural backbone of the Europe building construction sheets market. Demand leans on steel's load-bearing capacity and aluminium's corrosion resistance, both increasingly produced through low-carbon pathways such as electric arc furnaces powered by renewable electricity. ArcelorMittal and Tata Steel Europe actively promote recycled-content grades that cut embodied emissions by up to 40%. In parallel, building-integrated photovoltaics adopt aluminium skins as frameless carriers for thin-film cells, linking metal demand directly to green-energy targets.

Polymer sheets deliver the fastest segment CAGR of 5.29% toward 2031 as contractors favour lightweight panels for retrofits that avoid structural reinforcement. Formulations incorporating fire retardants and UV stabilisers extend service life, while bio-based resins open a lower-carbon alternative. Hybrid systems embed flexible solar laminates or phase-change materials within multilayer polymer membranes, broadening functional scope. Bitumen and rubber maintain roles in waterproofing and vibration damping, yet continual regulatory tightening on volatile compounds challenges their market presence. Overall, material innovation strengthens supply-side differentiation across the Europe building construction sheets market.

The Europe Building and Construction Sheets Market Report is Segmented by Material (Bitumen, Rubber, Metal, Polymer and Others), by Construction Type (New Construction and Renovation), by End-User (Residential, Commercial and Infrastructure), and by Country (United Kingdom, Germany, France, Italy, Spain and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Saint-Gobain

- LyondellBasell

- James Hardie Industries plc

- Paul Bauder GmbH

- Euramax International

- Celotex Limited

- Rauch Spanplattenwerk GmbH

- Rizolin LLC

- Icopal (BMI Group)

- CBG Composites GmbH

- Kingspan Group plc

- Tata Steel Europe

- ArcelorMittal Construction

- Sika AG

- Soprema Group

- Firestone Building Products (Holcim Elevate)

- IKO Industries

- Owens Corning

- BASF SE

- Knauf Insulation

- Coroplast Fritz Muller GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter energy-efficiency regulations for building envelopes

- 4.2.2 Expanded public funding for renovation programmes

- 4.2.3 Growth in data-centre construction increasing demand for structural decking

- 4.2.4 Rising adoption of modular and off-site construction methods

- 4.2.5 Integration of solar technologies into roofing and cladding systems

- 4.2.6 Shift toward locally sourced, low-carbon sheet materials

- 4.3 Market Restraints

- 4.3.1 Volatile energy prices elevating production costs

- 4.3.2 Trade measures limiting access to low-cost imports

- 4.3.3 Shortage of skilled installation labour

- 4.3.4 Tighter credit conditions damping new-build pipelines

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape (EU Green Deal & EPBD)

- 4.6 Technological Outlook

- 4.7 Sustainability & Circularity Initiatives

- 4.8 Digitalisation & Off-site Construction Impact

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material

- 5.1.1 Bitumen

- 5.1.2 Rubber

- 5.1.3 Metal

- 5.1.4 Polymer

- 5.1.5 Others

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Renovation

- 5.3 By End-user

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Infrastructure

- 5.4 By Country

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Saint-Gobain

- 6.4.2 LyondellBasell

- 6.4.3 James Hardie Industries plc

- 6.4.4 Paul Bauder GmbH

- 6.4.5 Euramax International

- 6.4.6 Celotex Limited

- 6.4.7 Rauch Spanplattenwerk GmbH

- 6.4.8 Rizolin LLC

- 6.4.9 Icopal (BMI Group)

- 6.4.10 CBG Composites GmbH

- 6.4.11 Kingspan Group plc

- 6.4.12 Tata Steel Europe

- 6.4.13 ArcelorMittal Construction

- 6.4.14 Sika AG

- 6.4.15 Soprema Group

- 6.4.16 Firestone Building Products (Holcim Elevate)

- 6.4.17 IKO Industries

- 6.4.18 Owens Corning

- 6.4.19 BASF SE

- 6.4.20 Knauf Insulation

- 6.4.21 Coroplast Fritz Muller GmbH

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment