PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906182

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906182

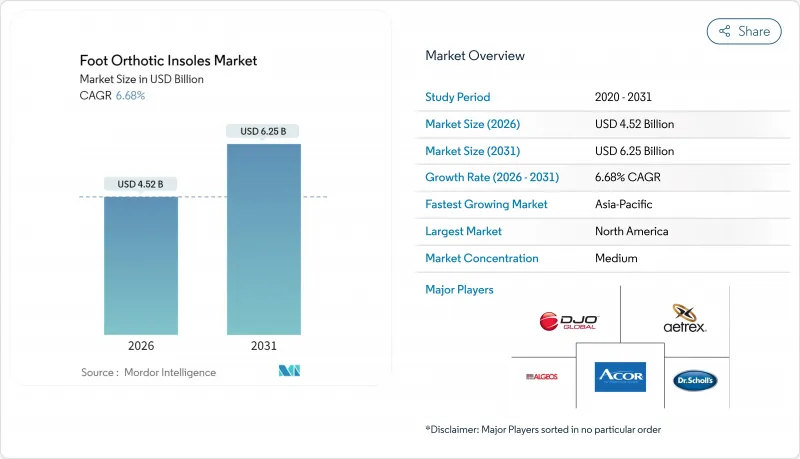

Foot Orthotic Insoles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Foot orthotic insoles market size in 2026 is estimated at USD 4.52 billion, growing from 2025 value of USD 4.24 billion with 2031 projections showing USD 6.25 billion, growing at 6.68% CAGR over 2026-2031.

Growth is powered by the spread of 3-D printing, demographic ageing, and rising diabetes prevalence. Broader sports participation and the pursuit of injury-prevention tools add incremental demand, while sustainability mandates accelerate the switch to bio-based and recycled foams. Cost and turnaround benefits from additive manufacturing encourage custom fits at scale, opening fresh direct-to-consumer (DTC) avenues. On the supply side, firms hedge against polymer volatility by diversifying into bio-EVA and recycled materials, limiting exposure to natural-rubber shortfalls. Competitive intensity stays moderate: established brands still leverage clinical networks, but smaller entrants exploit smartphone foot-scanning, AI gait analytics, and cloud-based design software to close capability gaps.

Global Foot Orthotic Insoles Market Trends and Insights

Rising Adoption of 3-D Printed Custom Orthotics

Digital workflows cut production times from weeks to hours. A single-build SLS printer can fabricate durable insoles in 24 hours, exceeding 4 million bend cycles in lab tests formlabs.com. Variable-stiffness spacer designs redistribute plantar pressure more evenly than uniform-density units, lifting comfort and therapeutic outcomes. Accessible hardware reduces capital barriers, letting smaller labs enter the custom arena. Smartphone scanning apps deliver millimetre accuracy, routing foot geometry to cloud-based CAD engines for home-fitted orders.

Growth in Geriatric & Diabetic Population Base

One-third of individuals over 65 report foot pain, often linked to fat-pad atrophy or ulcer risk primecareprosthetics.com. Pressure-alternating insoles under development cut peak loads at high-risk sites and target a cohort of 39 million Americans living with diabetes. Systematic reviews confirm custom offloading devices outperform prefabricated options in ulcer prevention, though adherence and reimbursement gaps temper adoption. Sensor-integrated diabetic models now stream plantar pressure and temperature readings to clinicians, enabling early intervention.

High Cost of Fully Custom Devices & Weak Reimbursement

Medicare covers orthotics only for specific diagnoses and shoulders 80% post-deductible, leaving sizable out-of-pocket burdens. Clinical trials prove custom offloaders superior for ulcer prevention, yet coding gaps in the HCPCS schedule slow uptake of novel formats.Start-ups counter by targeting the cash-pay segment with browser-based scanning kits and price points below USD 200 per pair.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Sports Participation & Injury-Prevention Focus

- Move Toward Eco-Based Bio-EVA & Recycled Foams

- Supply Volatility in EVA & Specialty Polymers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Customized offerings control 52.63% of foot orthotic insoles market revenue in 2025 and are tracking a 10% CAGR. Rapid additive manufacturing trims lead times to under 48 hours, encouraging labs to switch from plaster casting to scan-to-print pipelines. A flagship 3-D-printed series uses dual-density Poron Vive layers around a personalised arch scaffold, delivering measured gains in peak-pressure redistribution. The value proposition resonates among diabetic and athletic cohorts where biomechanical nuance matters. Prefabricated models still command volume in price-sensitive outlets, yet growth lags as consumers perceive limited therapeutic relief.

Accessible phone-scanning apps with AI gait analytics widen the addressable base for custom fits, particularly in regions with sparse podiatry coverage. Variable-stiffness spacer grids crafted via selective laser sintering help manufacturers meet prescriptive tolerances without tooling changes. Competitive parity in design capability pushes firms to differentiate through turnaround speed, eco-friendly materials, and subscription refresh plans.

Thermoplastics keep their 54.10% grip on 2025 revenue due to low cost and proven processing. Yet carbon-fiber composites post a 9.32% CAGR as athletes chase measurable performance uplifts. In a clinical setting, aerospace-grade carbon plates boosted standing long-jump distance by 1.6 inches and improved vertical-force output by 11%. Adoption extends from sprint spikes to court shoes where torsional rigidity stabilises forefoot roll.

EVAs remain staple cushioning agents, but feedstock constraints steer manufacturers toward sugarcane-derived grades with carbon-negative credentials. Polyethylene foams gain favour in children's orthotics for their light weight and recyclability. Flexible carbon-fiber fabrics introduce new mid-foot hinge behaviour, merging energy return with ground-feel for endurance runners.

The Foot Orthotic Insoles Market Report is Segmented by Product (Prefabricated, Customized), Material (Thermoplastics, Polyethylene Foams, Ethyl-Vinyl Acetates, Carbon-Fiber Composites, Leather, Other Materials), Application (Sports & Athletics, Personal Comfort, Medical), Distribution Channel (Hospitals & Clinics, Specialty Footwear Stores, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 43.10% of 2025 revenue. The region benefits from robust reimbursement mechanisms and high awareness of orthotic therapy for chronic conditions. Medicare's coverage, though conditional, stimulates prescription activity, while sports culture drives discretionary performance purchases. Regional innovation clusters in additive manufacturing enhance domestic supply resilience and minimise lead times.

Asia-Pacific is the fastest-growing territory at an 8.54% CAGR through 2031. Manufacturing clusters in Vietnam and southern China supply global footwear brands, anchoring local know-how in midsole foams and carbon-fiber plates. Rising middle-class earnings and broader diabetes screening fuel demand for medical orthotics, although awareness gaps persist outside tier-one cities. National health plans in Japan now subsidise diabetic offloading devices, setting precedents for neighbouring markets.

Europe maintains steady expansion, driven by stringent sustainability regulations that reward bio-EVA and recyclable materials. Healthcare systems reimburse medical orthotics, yet coverage levels diverge across member states. Consumers show marked willingness to pay premiums for eco-labelled footwear, encouraging retailers to offer carbon-neutral insole lines. Research networks in Germany and the Netherlands pioneer flexible carbon-fiber matrices and real-time sensor integration.

- DJO Global

- Dr. Scholl's Wellness Co.

- Acor Orthopedic Inc.

- Aetrex Worldwide Inc.

- Algeo

- KLM Laboratories Inc.

- Arden Orthotics Ltd

- Bauerfeind

- ComfortFit Orthotic Labs Inc.

- Bolton Bros

- Superfeet Worldwide Inc.

- PowerStep (Stable Step LLC)

- Sorbothane Inc.

- Currex GmbH

- Profoot Inc.

- VKTRY Gear

- Ottobock SE & Co. KGaA (Pohlig)

- Tread Labs

- Pedag International

- Footbalance System Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption Of 3-D Printed Custom Orthotics

- 4.2.2 Growth In Geriatric & Diabetic Population Base

- 4.2.3 Increasing Sports Participation & Injury-Prevention Focus

- 4.2.4 Move Toward Eco-Based Bio-EVA & Recycled Foams

- 4.2.5 Retailer Shift To Private-Label "Fit-While-You-Wait" Kiosks

- 4.2.6 Smartphones' Lidar Foot-Scan Apis Enabling Home Fitting

- 4.3 Market Restraints

- 4.3.1 Limited Consumer Awareness In Low-Income Regions

- 4.3.2 High Cost Of Fully Custom Devices & Weak Reimbursement

- 4.3.3 Biomechanical Risks From DTC Comfort-Only Inserts

- 4.3.4 Supply Volatility In EVA & Specialty Polymers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Product

- 5.1.1 Prefabricated

- 5.1.2 Customized

- 5.2 By Material

- 5.2.1 Thermoplastics

- 5.2.2 Polyethylene Foams

- 5.2.3 Ethyl-Vinyl Acetates (EVAs)

- 5.2.4 Carbon-Fiber Composites

- 5.2.5 Leather

- 5.2.6 Other Materials

- 5.3 By Application

- 5.3.1 Sports & Athletics

- 5.3.2 Personal Comfort

- 5.3.3 Medical

- 5.4 By Distribution Channel

- 5.4.1 Hospitals & Clinics

- 5.4.2 Specialty Footwear Stores

- 5.4.3 Sports Retailers

- 5.4.4 Online Retail

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 DJO Global Inc.

- 6.3.2 Dr. Scholl's Wellness Co.

- 6.3.3 Acor Orthopedic Inc.

- 6.3.4 Aetrex Worldwide Inc.

- 6.3.5 Algeo Limited

- 6.3.6 KLM Laboratories Inc.

- 6.3.7 Arden Orthotics Ltd

- 6.3.8 Bauerfeind AG

- 6.3.9 ComfortFit Orthotic Labs Inc.

- 6.3.10 Bolton Bros

- 6.3.11 Superfeet Worldwide Inc.

- 6.3.12 PowerStep (Stable Step LLC)

- 6.3.13 Sorbothane Inc.

- 6.3.14 Currex GmbH

- 6.3.15 Profoot Inc.

- 6.3.16 VKTRY Gear

- 6.3.17 Ottobock SE & Co. KGaA (Pohlig)

- 6.3.18 Tread Labs

- 6.3.19 Pedag International

- 6.3.20 Footbalance System Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment