PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906189

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906189

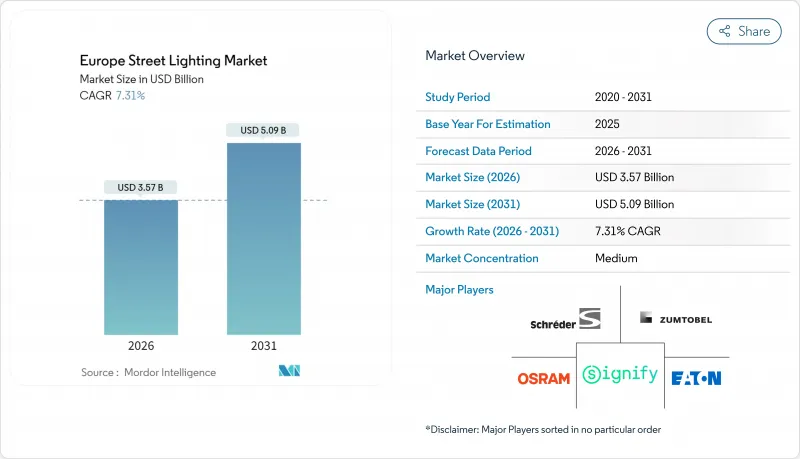

Europe Street Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The European street lighting market was valued at USD 3.33 billion in 2025 and estimated to grow from USD 3.57 billion in 2026 to reach USD 5.09 billion by 2031, at a CAGR of 7.31% during the forecast period (2026-2031).

Policy drivers-including the EU-wide fluorescent-lamp ban, looming mercury restrictions on high-pressure discharge lamps, and binding public-sector energy-efficiency targets-anchor demand for connected LED luminaires that can cut electricity use by 50-80% versus legacy fixtures. Germany leads adoption through large-scale retrofit programs, while Italy leverages National Recovery and Resilience Plan funds to accelerate smart lighting roll-outs. Hardware still dominates sales, yet software- and service-centric contracts are growing almost 9% annually as municipalities shift toward outcomes-based purchasing. Cost declines in LEDs, sensors, and wireless modules reinforce the European street lighting market as a foundational layer for 5G small cells and city-wide IoT sensor networks.

Europe Street Lighting Market Trends and Insights

EU Ban on Fluorescent Lamps and Strict Efficiency Targets

RoHS phase-outs removed compact fluorescent and T5/T8 tubes from sale in August 2023, triggering immediate retrofits across an estimated 11 billion lamp points and accelerating the European street lighting market. Municipalities also face binding 11.7% public-sector energy-consumption cuts by 2030, turning connected LED luminaires into compliance essentials. Signify calculates that converting the continent's remaining conventional streetlights would trim overall electricity demand from 13% to 8%, roughly equal to shutting 267 average power plants. Procurement urgency has intensified because non-compliance now attracts financial penalties under updated Energy Efficiency Directive rules.

Smart-City Stimulus Accelerating Smart-Lighting Roll-Outs

The EU Smart Cities Marketplace has channeled EUR 924 million (USD 1.076 billion) into 100 projects, positioning intelligent luminaires as foundational 5G and IoT nodes. Tampere's pilot used BrightSites poles to deliver high-speed wireless backhaul at 40% lower cost than trenching fiber. Munich's 48,000-unit LED upgrade includes adaptive dimming that slashes energy use by 93% during off-peak hours. As one of 100 EU cities pledged to be climate-neutral by 2030, Barcelona centrally monitors more than half of its 146,000 lighting points while upholding 20-30 lux safety levels.

High Upfront CAPEX for Smart Retrofits

Full smart-ready replacements cost EUR 300-500 per pole versus EUR 150-200 for basic LED swaps, delaying adoption in cash-constrained municipalities and tempering the European street lighting market trajectory. EU evidence calls highlight a financing gap, even though grants exist, pushing vendors to propose light-as-a-service contracts that shift investment off balance sheet. Yet procurement codes in several member states still struggle to accommodate outcome-based models, slowing deal closure.

Other drivers and restraints analyzed in the detailed report include:

- Falling LED, Sensor and Connectivity Costs

- EU Recovery and Resilience Facility Funding

- LED Driver Reliability and Thermal Failure Issues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional luminaires still represented 59.45% of the Europe street lighting market in 2025, but smart systems are accelerating at a 9.11% CAGR as city managers chase connectivity and energy analytics. Germany's Munich retrofit illustrates the pivot: 48,000 upgraded poles use adaptive dimming to save 93% of overnight power, a data point that resonates across the European street lighting industry planning.

Barcelona's centralized control over 146,000 points shows scalability; remote commands keep illumination at 20-30 lux while trimming real-time load, reinforcing confidence in smart upgrades within the European street lighting market.

Municipalities that already switched to LEDs now consider a second wave focused on sensors, traffic monitoring, and 5G small-cell attachment, underpinning service revenue streams. Strasbourg proves dimming policies can coexist with safety by timing partial shut-offs between 01:00-05:00 and cutting energy by 30%. Funding schemes under the Smart Cities Marketplace keep smart-lighting pilots within reach for mid-sized cities, boosting future demand.

LEDs captured 69.10% share of the European street lighting market size in 2025 and are on track for an 8.56% CAGR through 2031 under the mercury-phase-out timetable. Legacy fluorescent and HID products linger only where budgets delay retrofits or where extreme-output fixtures remain unmatched.

Performance leaps - from 35 lm/W to 100 lm/W - plus 50,000-hour durability mean most tenders now specify LEDs by default, locking in market leadership. Signify already derives 90% of sales from LED products, signaling maturity even as reliability concerns spur R&D on thermal solutions. EU 2040 climate rules requiring a 90% emissions cut make LED roll-outs non-negotiable for municipalities pursuing net-zero pathways.

The Europe Street Lighting Market Report is Segmented by Lighting Type (Conventional Lighting, and Smart Lighting), Light Source (LEDs, Fluorescent Lamps, and HID Lamps), Offering (Hardware, and Software, and Services), Connectivity Technology (Wired, and Wireless), Installation Type (New Installation, and Retrofit), and Country (Germany, United Kingdom, France, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Signify N.V.

- Zumtobel Group AG

- Schreder SA

- Eaton Corporation plc (Cooper Lighting)

- OSRAM GmbH

- Acuity Brands Inc.

- Cree Lighting, a division of IDEAL Industries

- Itron Inc.

- Telensa Ltd.

- Sensus, a Xylem Brand

- Flashnet SRL

- Lucy Zodion Ltd.

- Gelighting Solutions LLC

- Thorn Lighting Ltd. (Zumtobel)

- Le-Tehnika d.o.o. (Luxtella)

- Hubbell Incorporated

- Urban Control Ltd.

- Flashnet Smart-City

- AEC Illuminazione Srl

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU ban on fluorescent lamps and strict efficiency targets

- 4.2.2 Smart-city stimulus accelerating smart-lighting roll-outs

- 4.2.3 Falling LED, sensor and connectivity costs

- 4.2.4 EU Recovery and Resilience Facility funding

- 4.2.5 Secondary-replacement wave for first-gen LEDs (2024-30)

- 4.2.6 Street-light poles as edge-IoT real-estate

- 4.3 Market Restraints

- 4.3.1 High upfront CAPEX for smart retrofits

- 4.3.2 LED driver reliability and thermal failure issues

- 4.3.3 Cyber-security and GDPR compliance hurdles

- 4.3.4 Semiconductor-grade component supply volatility

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Lighting Type

- 5.1.1 Conventional Lighting

- 5.1.2 Smart Lighting

- 5.2 By Light Source

- 5.2.1 LEDs

- 5.2.2 Fluorescent Lamps

- 5.2.3 HID Lamps

- 5.3 By Offering

- 5.3.1 Hardware

- 5.3.1.1 Lights and Bulbs

- 5.3.1.2 Luminaires

- 5.3.1.3 Control Systems

- 5.3.2 Software and Services

- 5.3.1 Hardware

- 5.4 By Connectivity Technology

- 5.4.1 Wired (PLC, DALI, Ethernet)

- 5.4.2 Wireless (Zigbee, LoRa-WAN, NB-IoT, 5G)

- 5.5 By Installation Type

- 5.5.1 New Installation

- 5.5.2 Retrofit / Secondary Replacement

- 5.6 By Country

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Signify N.V.

- 6.4.2 Zumtobel Group AG

- 6.4.3 Schreder SA

- 6.4.4 Eaton Corporation plc (Cooper Lighting)

- 6.4.5 OSRAM GmbH

- 6.4.6 Acuity Brands Inc.

- 6.4.7 Cree Lighting, a division of IDEAL Industries

- 6.4.8 Itron Inc.

- 6.4.9 Telensa Ltd.

- 6.4.10 Sensus, a Xylem Brand

- 6.4.11 Flashnet SRL

- 6.4.12 Lucy Zodion Ltd.

- 6.4.13 Gelighting Solutions LLC

- 6.4.14 Thorn Lighting Ltd. (Zumtobel)

- 6.4.15 Le-Tehnika d.o.o. (Luxtella)

- 6.4.16 Hubbell Incorporated

- 6.4.17 Urban Control Ltd.

- 6.4.18 Flashnet Smart-City

- 6.4.19 AEC Illuminazione Srl

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment