PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906202

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906202

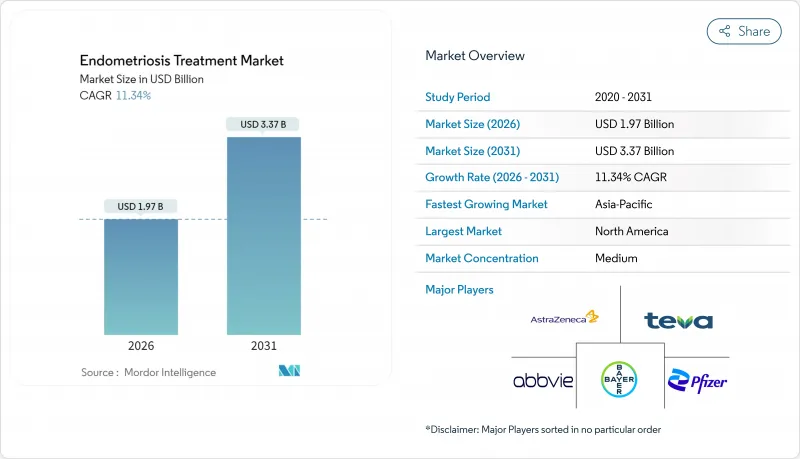

Endometriosis Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Endometriosis Treatment Market market is expected to grow from USD 1.77 billion in 2025 to USD 1.97 billion in 2026 and is forecast to reach USD 3.37 billion by 2031 at 11.34% CAGR over 2026-2031.

Rising disease prevalence, sustained public-health campaigns, and a wave of regulatory approvals for oral gonadotropin-releasing hormone (GnRH) antagonists are setting a new treatment standard. Venture-capital inflows into non-hormonal pipelines, the proliferation of FemTech platforms, and government-funded action plans are expanding patient reach while reshaping competitive strategies. Meanwhile, diagnostic delays, high lifetime costs, and specialist shortages continue to temper uptake, steering innovators toward digital triage tools and minimally invasive care pathways that can bridge access gaps.

Global Endometriosis Treatment Market Trends and Insights

Rising Prevalence Among Reproductive-Age Women

More than 190 million women now live with endometriosis worldwide, and prevalence among Asian populations stands near 15%, markedly higher than the 5-10% range reported in Western cohorts. The demographic trend toward delayed parenthood, coupled with urban lifestyle shifts, is enlarging the at-risk population base in emerging markets. Productivity losses and excess healthcare utilization frame a USD 200 billion global economic burden that has prompted pharmaceutical enterprises to create dedicated women's-health divisions. Environmental research linking phthalate exposure to symptom aggravation is incentivizing new metabolic and environmental-medicine approaches. Stakeholders are intensifying epidemiological surveillance to quantify sub-regional hotspots, a strategy expected to refine market-entry decisions over the long term.

Growing Awareness and Earlier Diagnosis Initiatives

Public-sector outreach is compressing the historic seven-year diagnostic lag. Australia's National Action Plan, backed by AUD 87.19 million, is scaling specialist GP clinics and patient-education programs. The World Health Organization's 2024 declaration elevating endometriosis to priority-condition status has galvanized policy harmonization and insurance-coding revisions across Europe and North America. Digital symptom trackers such as Lyv's app flag high-risk profiles and direct users toward specialist care, with machine-learning algorithms boosting triage accuracy. Medical-school curricula are integrating endometriosis modules for the first time, a move likely to diminish misdiagnosis and under-treatment. Collectively, these measures are enlarging the treated population and stimulating prescription volumes.

High Lifetime Treatment and Surgery Cost Burden

Median patient spending rises from USD 4,318 in the pre-diagnosis phase to USD 17,230 within six months post-diagnosis, a 300% escalation that strains household budgets and payer systems. Coverage gaps for therapies priced above USD 1,000 per month intensify inequities, although value-based contracts and manufacturer assistance funds are partly offsetting out-of-pocket exposure. Surgical recurrence rates approaching 40% within five years add repeat procedure costs, while emergency-room visits occur 60% more frequently than in matched controls. These dynamics deter aggressive management and may limit near-term uptake of premium therapies despite demonstrable clinical benefits.

Other drivers and restraints analyzed in the detailed report include:

- Launch of GnRH Antagonist Class

- Surge in FemTech Remote-Monitoring Platforms

- Limited Specialist Surgeons Driving Wait-Times to More Than 12 Months

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Gonadotropin-releasing hormone therapies captured 51.62% of Endometriosis treatment market share in 2025, buoyed by the blockbuster entry of oral antagonists that removed injection barriers and delivered superior symptom control. Robust payer acceptance in North America and Europe sustained premium pricing, reinforcing revenue leadership. However, oral contraceptives are accelerating at a 12.22% CAGR as younger patients prioritize fertility preservation and lower adverse-event profiles. Market expansion is additionally shaped by NSAIDs providing first-line pain relief despite limited disease-modifying effect. The shift toward combination regimens that temper hypoestrogenic side effects is fostering strategic alliances between hormonal and non-hormonal developers, signaling an impending competitive re-balancing.

Looking ahead, innovation pipelines spotlight prolactin-receptor antagonists, metabolic modulators, and cannabinoid formulations, all of which promise disease control without systemic hormone suppression. Clinical momentum around agents such as HMI-115 and dichloroacetate could diversify therapeutic options, ultimately reducing the class risk faced by GnRH incumbents. Should bone-density concerns remain manageable, the Endometriosis treatment market is expected to maintain a heterogeneous portfolio that caters to symptom severity, fertility intent, and co-morbid profile.

Superficial peritoneal lesions constituted 41.86% of diagnosed cases in 2025, benefiting from earlier detection through routine laparoscopy. Improved imaging protocols have simultaneously elevated recognition of deeply infiltrating disease, which is advancing at an 11.71% CAGR on the back of refined MRI staging and specialized surgical techniques. Pharmaceutical sponsors are stratifying clinical trials by lesion depth to document differential efficacy across phenotypes.

Endometriomas maintain steady surgical volumes due to high recurrence risk, yet non-invasive modalities such as high-intensity focused ultrasound and targeted nanoparticle ablation are under investigation. Rare extrapelvic manifestations, though numerically small, are receiving newfound attention through precision-diagnostic initiatives, offering a test-bed for biomarker-based treatment assignment. Cross-type data integration is anticipated to refine prognostic algorithms and inform future regulatory submissions.

The Endometriosis Treatment Market Report is Segmented by Drug Class (NSAIDs, Gonadotropin Releasing Hormone, and More), Endometriosis Type (Superficial Peritoneal, and More), Treatment Type (Pain Management Drugs, and More), Route of Administration (Oral, and More), Distribution Channel (Hospital Pharmacies, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 41.58% of 2025 revenue, buoyed by advanced reimbursement frameworks, strong advocacy networks, and early adoption of oral GnRH antagonists. The Biden administration's USD 200 million investment in women's-health research is fast-tracking precision-medicine conduits. Yet insurance disparities persist, with Black patients receiving fewer prescriptions for endometriosis-related pain and comorbid conditions, highlighting an ongoing equity challenge. Telehealth is narrowing rural gaps, although infrastructure gaps restrain full penetration.

Asia-Pacific is the fastest-growing arena, advancing at a 13.05% CAGR through 2031 on the back of healthcare system expansion, urban migration, and heightened awareness campaigns. Prevalence standing near 15% underscores a large untreated pool that modern fertility trends continue to enlarge. Harmonized regulatory pathways in Japan, South Korea, and Australia are shortening approval cycles, while China's integration of traditional herbal protocols with pharmaceutical regimens offers culturally attuned care models. Strategic collaborations between multinational firms and local manufacturers are scaling distribution across tier-two cities.

Europe retains a mature demand profile characterized by broad access but constrained national health budgets. The European Medicines Agency streamlines drug access across member states, yet divergent reimbursement policies can lengthen country-level launch timelines. Brexit continues to complicate regulatory alignment between the United Kingdom and continental Europe, prompting companies to maintain dual submission strategies. Middle East and Africa show incremental gains driven by rising private insurance coverage and emerging center-of-excellence programs in the Gulf. South America, led by Brazil, is rolling out centralized procurement models that lower therapy costs and stimulate uptake.

- Abbvie

- Bayer

- Pfizer

- Myovant Sciences / Sumitomo Pharma

- Organon

- Eli Lilly and Company

- Sun Pharmaceuticals Industries

- Teva Pharmaceutical Industries

- Cipla

- TerSera Therapeutics

- AstraZeneca

- Takeda Pharmaceuticals

- Neurocrine Biosciences

- ObsEva SA

- Gedeon Richter Plc

- Sandoz Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence Among Reproductive-Age Women

- 4.2.2 Growing Awareness and Earlier Diagnosis Initiatives

- 4.2.3 Launch of GnRH Antagonist Class

- 4.2.4 Surge in FemTech Remote-Monitoring Platforms

- 4.2.5 Venture Funding for Non-Hormonal R&D Pipelines

- 4.2.6 Government Endometriosis Action Plans

- 4.3 Market Restraints

- 4.3.1 High Lifetime Treatment and Surgery Cost Burden

- 4.3.2 Adverse Effects / Bone-Density Loss from Long-Term Hormone Use

- 4.3.3 Racial and Socio-Economic Disparities in Prescription Access

- 4.3.4 Limited Specialist Surgeons Driving Wait-Times to More Than 12 Months

- 4.4 Regulatory Landscape

- 4.5 Pipeline Analysis

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Drug Class

- 5.1.1 NSAIDs

- 5.1.2 Oral Contraceptives

- 5.1.3 Gonadotropin Releasing Hormone

- 5.1.4 Other Drug Classes

- 5.2 By Endometriosis Type

- 5.2.1 Superficial Peritoneal Endometriosis

- 5.2.2 Endometriomas

- 5.2.3 Deeply Infiltrating Endometriosis

- 5.2.4 Other Types

- 5.3 By Treatment Type

- 5.3.1 Pain Management Drugs

- 5.3.2 Hormone Therapy

- 5.4 By Route of Administration

- 5.4.1 Oral

- 5.4.2 Injectable

- 5.4.3 Others

- 5.5 By Distribution Channel

- 5.5.1 Hospital Pharmacies

- 5.5.2 Retail and Drugstores

- 5.5.3 Online Pharmacies

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Bayer AG

- 6.3.3 Pfizer Inc.

- 6.3.4 Myovant Sciences / Sumitomo Pharma

- 6.3.5 Organon & Co.

- 6.3.6 Eli Lilly & Co.

- 6.3.7 Sun Pharmaceutical Industries

- 6.3.8 Teva Pharmaceutical Industries

- 6.3.9 Cipla Ltd.

- 6.3.10 TerSera Therapeutics

- 6.3.11 AstraZeneca

- 6.3.12 Takeda Pharmaceutical

- 6.3.13 Neurocrine Biosciences

- 6.3.14 ObsEva SA

- 6.3.15 Gedeon Richter Plc

- 6.3.16 Sandoz AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment