PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906210

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906210

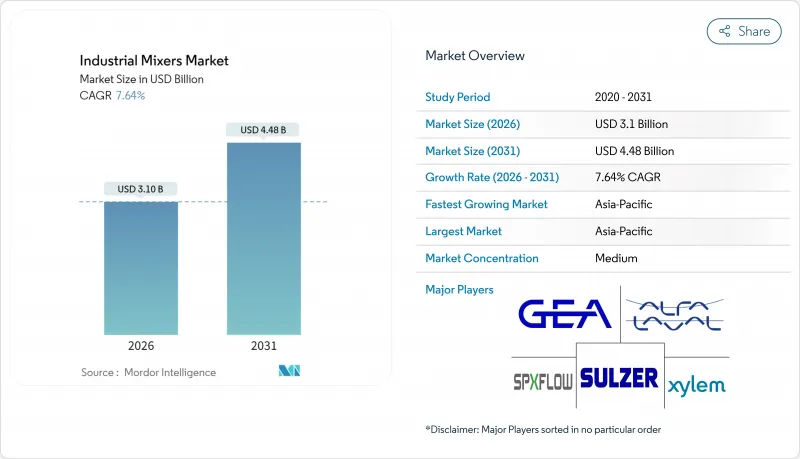

Industrial Mixers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The industrial mixers market is expected to grow from USD 2.88 billion in 2025 to USD 3.1 billion in 2026 and is forecast to reach USD 4.48 billion by 2031 at 7.64% CAGR over 2026-2031.

Strong regulatory oversight in food and pharmaceutical processing, rising demand for energy-efficient high-torque drives, and expanding wastewater treatment infrastructure are key factors driving steady gains for the industrial mixers market. Rapid urbanization in Asia-Pacific, the push for continuous manufacturing in life sciences, and digital retrofits that enable predictive maintenance further widen adoption. Vendors differentiate through hygienic design, intelligent control systems, and modular skid packages that shorten installation time while boosting process reliability.

Global Industrial Mixers Market Trends and Insights

Stricter Sanitary Mandates in Food and Pharma

Food-grade and pharmaceutical plants now specify electropolished surfaces, crevice-free welds, and validated clean-in-place protocols to satisfy EHEDG 2024 updates and FDA 21 CFR 110.35 requirements. Equipment suppliers that deliver certified hygienic designs secure premium pricing while smaller fabricators face rising compliance costs. In pharmaceuticals, continuous production lines rely on documented mixing uniformity, driving the procurement of high-shear and magnetically driven mixers that are validated under good manufacturing practice audits. Retrofits to legacy agitators often fail validation, accelerating outright replacement. This dynamic strengthens competitive barriers and cements long-term service contracts around sanitary assets.

Energy-Efficient High-Torque Motor Adoption

IE5 synchronous reluctance motors, paired with variable-frequency drives, reduce mixer energy draw by up to 20% compared to legacy induction units, while delivering the torque needed for high-viscosity slurries. Regulations already mandate IE4 minimum efficiency above 0.75 kW, and similar rules under discussion in India and Brazil will accelerate fleet renewal. Plant engineers link drives to edge analytics that reduce speed during low-load phases, extending seal life and lowering power bills across the industrial mixer market. Vendors that bundle motors with digital control panels command higher margins and cultivate data-driven service revenues.

Raw-Material Price Volatility (Stainless Steel, Alloys)

Stainless steel prices fluctuated by 15-20% in 2024 as nickel prices traded between USD 16,500 and USD 20,000 per metric ton, eroding margins for mixer fabricators. Specialty alloys, such as Hastelloy C-276, followed similar spikes tied to aerospace demand, forcing OEMs to renegotiate long-term frame contracts and hedge their purchases. Larger vendors leverage global procurement and inventory pooling to buffer cost shocks, but regional job shops struggle to pass increases through, curbing new capacity additions in the industrial mixers industry. Supply-chain diversification into Indonesia and the United States may stabilize pricing, but it introduces higher baseline costs that will be passed through to equipment prices.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Wastewater Recycling Capacity Additions

- Bioreactor Retrofits for Cultivated-Meat Pilots

- High Capex vs. Alternative Inline Dosing Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Agitators commanded a 35.85% share of the industrial mixers market in 2025, underpinned by decades of performance data in bulk chemical, mineral processing, and water treatment operations. Their robust frames and modular impeller libraries allow economical customization across vessel sizes exceeding 100 m3. The industrial mixers market size for agitators is expected to grow steadily as replacement cycles align with increasingly stringent sanitary and energy norms. High-shear mixers, however, are expected to grow at an 8.05% CAGR, driven by demand for emulsification in biotechnology and advanced materials. Inline rotor-stator designs deliver micron-level particle reduction, supporting continuous wet-milling and pre-dispersion tasks that upstream equipment cannot meet. Suppliers integrate real-time torque and temperature sensors that feed digital twins, thereby improving scale-up accuracy and reducing validation time in regulated segments, such as the pharmaceutical industry.

Digital integration reshapes every product line. Agitator vendors embed vibration sensors on gearbox housings and shafts, feeding AI models that forecast bearing life. Submersible mixer makers redesign housings with composite shrouds that cut weight while resisting chloride stress cracking in seawater desalination plants. Static and jet mixers, which are normally energy-neutral, now ship with differential-pressure transmitters that allow operators to verify mixing intensity without intrusive probes. Across categories, IoT frameworks enable pay-per-mix service models, where OEMs bill for uptime rather than equipment alone, thereby expanding recurring revenue streams within the industrial mixers market.

The Industrial Mixers Market Report is Segmented by Product Type (Agitators, Special Mixers, Submersible Mixers, and More), End-User Industry (Chemicals, Water and Wastewater, Food and Beverage, Petrochemicals, Pharmaceuticals, Energy, and More), Power Rating (< 5 KW, 5-15 KW, and More), and Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific holds 29.55% of global revenue and is on track for an 8.18% CAGR through 2031, reflecting government-backed chemical capacity additions, expanding pharmaceutical exports, and aggressive municipal wastewater spending in China and India. In China, refinery off-gas hydrogen recycling creates demand for ATEX-compliant jet mixers, while mega-sized membrane bioreactor projects specify high-efficiency submersible units. India's production-linked incentive scheme for active pharmaceutical ingredients stimulates upgrades to inline high-shear mixers, and Southeast Asia's palm-oil downstream clusters adopt special agitators for deodorization stages. Local fabrication lowers cost, but international OEMs dominate premium tiers that demand documented validation.

North America commands a sizable installed base anchored by biotech clusters in Boston, San Diego, and Toronto. Continuous biologic manufacturing lines require sanitary high-shear mixers with single-use flow paths, while shale gas processing relies on jet mixers for crude desalting. Stringent FDA and EPA regulations promote replacement cycles that favor energy-efficient designs. Mexico's chemical and food manufacturing industries import modular mixing skids from the United States, utilizing near-shore supply chains to minimize lead times. Digital retrofits funded under the U.S. Inflation Reduction Act channel investment toward predictive maintenance modules across legacy fleets within the industrial mixers market.

Europe emphasizes sustainability and operational excellence, guided by the EU Green Deal. Plants adopt IE5 motors, magnetically coupled seals, and low-carbon stainless alloys certified under environmental product declarations. Chemical parks in Germany and the Netherlands prioritize mixers that integrate with plant-wide digital twins. ATEX and IECEx mandates for hydrogen electrolysis units increase certification costs, yet they also protect incumbent suppliers with robust documentation systems. Circular economy initiatives are expanding demand for mixers in plastic recycling, anaerobic digestion, and organic fertilizer production. Collectively, these drivers promote a balanced yet technologically intensive outlook for the industrial mixer market in Europe.

- SPX FLOW Inc.

- Sulzer Ltd.

- Alfa Laval AB

- Xylem Inc.

- GEA Group AG

- EKATO HOLDING GmbH

- Philadelphia Mixing Solutions Ltd.

- Charles Ross & Son Company

- Silverson Machines Inc.

- IKA-Werke GmbH & Co. KG

- amixon GmbH

- Komax Systems Inc.

- Landia A/S

- Satake Chemical Equipment Mfg. Ltd.

- Dynamix Agitators Inc.

- Statiflo International Ltd.

- Scott Turbon Mixer Inc.

- INOXPA S.A.U.

- Enviropax Inc.

- Arde Barinco Inc.

- ITT Bornemann GmbH

- Zhejiang Great Wall Mixers Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter sanitary mandates in food and pharma

- 4.2.2 Energy-efficient high-torque motor adoption

- 4.2.3 Surge in wastewater recycling capacity additions

- 4.2.4 Bioreactor retrofits for cultivated-meat pilots

- 4.2.5 On-site chemical blending for battery-grade materials

- 4.2.6 Modular "mix-on-demand" skids for remote mining camps

- 4.3 Market Restraints

- 4.3.1 Raw-material price volatility (stainless steel, alloys)

- 4.3.2 High capex vs. alternative inline dosing systems

- 4.3.3 Rising ATEX/IECEx certification costs for hydrogen hubs

- 4.3.4 Skilled-operator shortage for large-diameter agitators

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Agitators

- 5.1.2 Special Mixers

- 5.1.3 Submersible Mixers

- 5.1.4 High-shear Mixers

- 5.1.5 Static Mixers

- 5.1.6 Jet Mixers

- 5.1.7 Other Product Types

- 5.2 By End-User Industry

- 5.2.1 Chemicals

- 5.2.2 Water and Wastewater

- 5.2.3 Food and Beverage

- 5.2.4 Petrochemicals

- 5.2.5 Pharmaceuticals

- 5.2.6 Pulp and Paper

- 5.2.7 Energy (Power and Renewables)

- 5.2.8 Mining and Minerals

- 5.2.9 Other Process Industries

- 5.3 By Power Rating

- 5.3.1 < 5 kW

- 5.3.2 5 - 15 kW

- 5.3.3 15 - 50 kW

- 5.3.4 > 50 kW

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 South-East Asia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Egypt

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SPX FLOW Inc.

- 6.4.2 Sulzer Ltd.

- 6.4.3 Alfa Laval AB

- 6.4.4 Xylem Inc.

- 6.4.5 GEA Group AG

- 6.4.6 EKATO HOLDING GmbH

- 6.4.7 Philadelphia Mixing Solutions Ltd.

- 6.4.8 Charles Ross & Son Company

- 6.4.9 Silverson Machines Inc.

- 6.4.10 IKA-Werke GmbH & Co. KG

- 6.4.11 amixon GmbH

- 6.4.12 Komax Systems Inc.

- 6.4.13 Landia A/S

- 6.4.14 Satake Chemical Equipment Mfg. Ltd.

- 6.4.15 Dynamix Agitators Inc.

- 6.4.16 Statiflo International Ltd.

- 6.4.17 Scott Turbon Mixer Inc.

- 6.4.18 INOXPA S.A.U.

- 6.4.19 Enviropax Inc.

- 6.4.20 Arde Barinco Inc.

- 6.4.21 ITT Bornemann GmbH

- 6.4.22 Zhejiang Great Wall Mixers Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment