PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906889

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906889

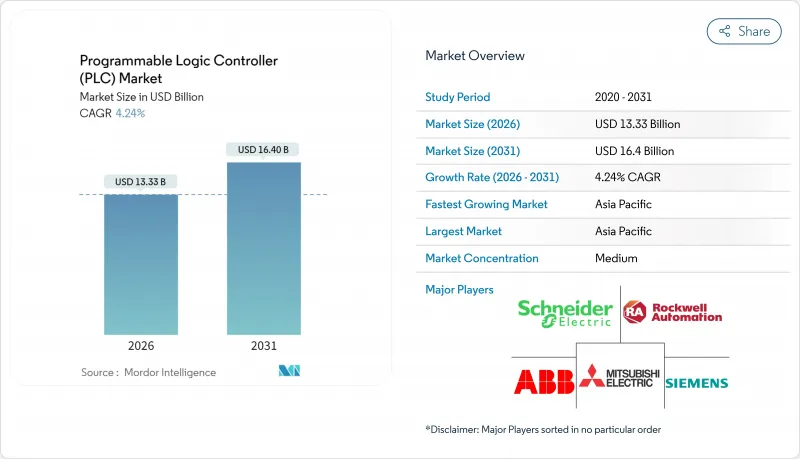

Programmable Logic Controller (PLC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Programmable Logic Controller Market is expected to grow from USD 12.79 billion in 2025 to USD 13.33 billion in 2026 and is forecast to reach USD 16.4 billion by 2031 at 4.24% CAGR over 2026-2031.

Steady expansion reflects ongoing modernization of factory floors, rising cybersecurity-driven reshoring, and the gradual shift from fixed hardware to software-defined automation. The Asia-Pacific region leads in both scale and momentum, as subsidy-backed capacity additions in China and India boost baseline demand for compact controllers. Modular architectures remain the cornerstone of large plants; yet, virtualized solutions are gaining market share as users seek flexible deployments on standard industrial PCs. Utilities, automotive electrification, and grid-edge projects anchor near-term purchases, while predictive-maintenance initiatives extend the revenue stream toward services. Supply-chain dual-sourcing and stronger cybersecurity mandates raise switching costs, allowing established brands to protect pricing even as component shortages ease.

Global Programmable Logic Controller (PLC) Market Trends and Insights

Accelerated Industry 4.0 Adoption in Manufacturing

Factories digitalize to boost productivity, and PLCs act as the local data hubs that connect machines with enterprise software. The German Federal Ministry for Economic Affairs reported a jump to 78% Industry 4.0 adoption in 2024, up from 65% in 2023, underscoring the momentum behind controller upgrades. Subsidies in China and India further lower the cost of automation for small producers, while Audi's virtual PLC rollout cut commissioning time by 23% and improved real-time optimization, validating the transition toward software-centric control. Rising ISO 9001 traceability requirements obligate manufacturers to replace legacy hardware with modern controllers that support granular data logging and seamless ERP integration. Across discrete and process industries, demand concentrates on PLCs with built-in edge analytics that shorten feedback loops without compromising cybersecurity protocols.

IIoT and Cloud Integration Enabling Predictive Maintenance

Edge-ready PLCs analyze vibration, temperature, and power metrics locally, sending only refined insights to cloud dashboards for fleetwide health monitoring. Schneider Electric's EcoStruxure platform exemplifies the hybrid model, fusing on-premise logic with cloud algorithms for continuous optimization. 5G connectivity and digital-twin software now coordinate distributed PLC nodes in real time, supporting autonomous process adjustments that curb unplanned downtime. Utilities and metals plants that deploy predictive maintenance report sharper OEE gains and lower spare-parts inventories, validating the investment case despite residual cybersecurity concerns.

High Up-Front Capital Cost for Small Manufacturers

Average project outlays of USD 15,000-50,000 still deter many micro-scale firms, especially when integration, training, and downtime are counted. Limited cash reserves often lead to over-specification because novice buyers adopt a one-size-fits-all mindset to mitigate perceived risk. Financing schemes and vendor leasing ease pressure, but cannot fully offset conservative investment cultures. Subscription-based virtual PLCs promise lower entry points, yet nascent offerings leave adoption uneven, particularly in regions where internet reliability lags.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Compact Automation Among SMEs

- Shift to Software-Defined PLC Workstations

- Escalating Cybersecurity Threats to Connected PLCs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Modular configurations dominated with 41.56% programmable logic controller market share in 2025, reflecting their ability to expand I/O and compute power alongside plant upgrades. The architecture lets engineers add motion, safety, or AI cards without forklift replacements, supporting mixed-model lines in automotive and consumer electronics. Soft PLCs, though still niche, are advancing at a 7.22% CAGR as hypervisors deliver deterministic performance and vendors embed hardened kernels.

Across both discrete and process industries, demand centers on controllers that host edge analytics for anomaly detection at the machine level. Compact PLCs retain appeal for stand-alone machines, while distributed PLCs serve large refineries and power stations that favor fault-tolerant, geographically separated nodes. As OPC-UA over TSN matures, users expect seamless interoperability, further commoditizing hardware and shifting differentiation to software toolchains and support ecosystems.

Hardware and software together held 84.67% of the programmable logic controller market size in 2025, yet service revenue is expanding at 7.76% CAGR as users pivot from CapEx to OpEx models. Integration complexity climbs with each layer of IIoT connectivity, elevating demand for vendor-led consulting and application engineering.

Predictive maintenance packages bundle remote monitoring, firmware management, and AI-driven diagnostics, creating sticky multi-year contracts. Vendors also ramp training academies in emerging economies to close the skills gap and lock in brand familiarity. Cloud-hosted support portals lower travel costs, while augmented-reality guides shorten onsite repair cycles, reinforcing service pull even in hardware-centric replacement projects.

PLC Market Report is Segmented by Product Type (Compact PLC, Modular PLC, Distributed PLC, Soft PLC, Other Products), Component (Hardware and Software, Services), Product Size (Nano PLC, Micro PLC, Small PLC, Medium PLC, Large PLC), End-User Industry (Automotive, Food and Beverage, Chemical and Petrochemical, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific's manufacturing resurgence underpins both scale and speed, with 35.10% revenue in 2025 and 6.12% CAGR to 2031. China's post-pandemic stimulus subsidized controller upgrades in automotive and electronics, while India's industrial corridor builds encourage first-time PLC rollouts. Japan's Quality-4.0 initiatives keep demand high for deterministic, nano-second-level controllers used in electronics placement machines. South Korean shipyards and fabs specify redundant PLC clusters for mission-critical uptime, anchoring high-margin orders.

Europe's sustainability push frames controller purchases around energy management and circular-economy compliance. The EU Cyber Resilience Act of 2024 obliges OEMs to certify security-by-design, boosting demand for products with encrypted communications and built-in anomaly detection. German automakers pilot software-defined PLC sandboxes, while France and Italy automate aerospace composites lines with fail-safe logic.

North American users prioritize secure supply chains and domestic semiconductor content. The Infrastructure Investment and Jobs Act funds substation refurbishments that incorporate modern controllers for load-balancing and fault isolation. Mexico's nearshore boom ramps automotive harness production, requiring swift deployment of compact PLCs. Canada's mining and lumber sectors favor rugged gear with extended temperature ratings. Overall, regional buyers weigh cybersecurity credentials and on-shore repair support heavily in tender scoring.

- Siemens AG

- Rockwell Automation Inc.

- Schneider Electric SE

- Mitsubishi Electric Corporation

- ABB Ltd.

- Omron Corporation

- Emerson Electric Co.

- Honeywell International Inc.

- Beckhoff Automation GmbH & Co. KG

- Delta Electronics Inc.

- Bosch Rexroth AG

- Panasonic Holdings Corporation

- Fuji Electric Co. Ltd.

- Hitachi Ltd.

- IDEC Corporation

- Keyence Corporation

- Toshiba Corporation

- General Electric Company

- Parker Hannifin Corporation

- Eaton Corporation plc

- Yokogawa Electric Corporation

- Inovance Technology Co. Ltd.

- Hollysys Automation Technologies Ltd.

- WAGO Kontakttechnik GmbH & Co. KG

- B&R Industrial Automation GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Industry-4.0 adoption in manufacturing

- 4.2.2 Growing demand for compact automation among SMEs

- 4.2.3 IIoT and cloud integration enabling predictive maintenance

- 4.2.4 Shift to software-defined PLC workstations

- 4.2.5 Adoption of open industrial protocols (OPC-UA over TSN)

- 4.2.6 Cybersecurity-driven domestic sourcing mandates

- 4.3 Market Restraints

- 4.3.1 High up-front capital cost for small manufacturers

- 4.3.2 Escalating cybersecurity threats to connected PLCs

- 4.3.3 Substitution risk from industrial PCs and soft-PLCs

- 4.3.4 Semiconductor supply volatility inflating lead times

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Compact PLC

- 5.1.2 Modular PLC

- 5.1.3 Distributed PLC

- 5.1.4 Soft PLC

- 5.1.5 Other Products

- 5.2 By Component

- 5.2.1 Hardware and Software

- 5.2.2 Services

- 5.2.2.1 Installation and Integration

- 5.2.2.2 Training and Support

- 5.2.2.3 Maintenance

- 5.3 By Product Size

- 5.3.1 Nano PLC

- 5.3.2 Micro PLC

- 5.3.3 Small PLC

- 5.3.4 Medium PLC

- 5.3.5 Large PLC

- 5.4 By End-user Industry

- 5.4.1 Automotive

- 5.4.2 Food and Beverage

- 5.4.3 Chemical and Petrochemical

- 5.4.4 Oil and Gas

- 5.4.5 Energy and Utilities

- 5.4.6 Water and Wastewater Treatment

- 5.4.7 Pharmaceutical

- 5.4.8 Pulp and Paper

- 5.4.9 Metals and Mining

- 5.4.10 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 South-East Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level overview, Market level overview, Core segments, Financials as available, Strategic information, Market rank/share for key companies, Products and Services, and Recent developments)

- 6.4.1 Siemens AG

- 6.4.2 Rockwell Automation Inc.

- 6.4.3 Schneider Electric SE

- 6.4.4 Mitsubishi Electric Corporation

- 6.4.5 ABB Ltd.

- 6.4.6 Omron Corporation

- 6.4.7 Emerson Electric Co.

- 6.4.8 Honeywell International Inc.

- 6.4.9 Beckhoff Automation GmbH & Co. KG

- 6.4.10 Delta Electronics Inc.

- 6.4.11 Bosch Rexroth AG

- 6.4.12 Panasonic Holdings Corporation

- 6.4.13 Fuji Electric Co. Ltd.

- 6.4.14 Hitachi Ltd.

- 6.4.15 IDEC Corporation

- 6.4.16 Keyence Corporation

- 6.4.17 Toshiba Corporation

- 6.4.18 General Electric Company

- 6.4.19 Parker Hannifin Corporation

- 6.4.20 Eaton Corporation plc

- 6.4.21 Yokogawa Electric Corporation

- 6.4.22 Inovance Technology Co. Ltd.

- 6.4.23 Hollysys Automation Technologies Ltd.

- 6.4.24 WAGO Kontakttechnik GmbH & Co. KG

- 6.4.25 B&R Industrial Automation GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment