PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906904

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906904

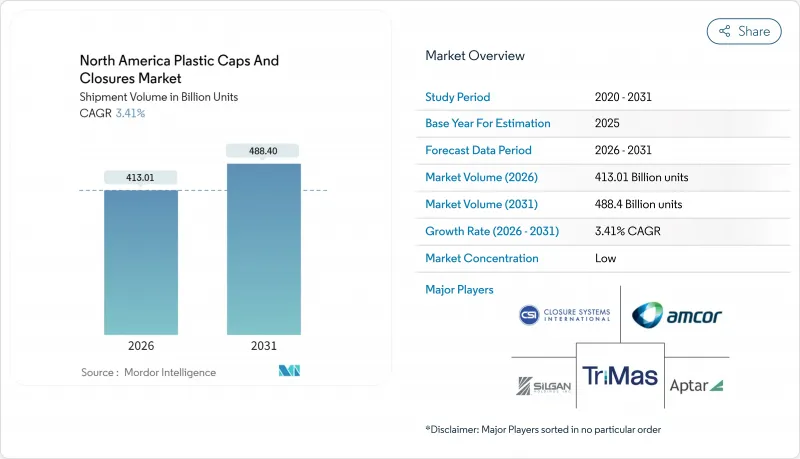

North America Plastic Caps And Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The North America plastic caps and closures market is expected to grow from 399.39 billion units in 2025 to 413.01 billion units in 2026 and is forecast to reach 488.4 billion units by 2031 at 3.41% CAGR over 2026-2031.

This growth reflects the market's role in safeguarding product quality across beverages, food, pharmaceuticals, and personal-care items while meeting rigorous safety and sustainability expectations. Functional beverage launches, e-commerce-driven pharmaceutical sales, and state-level recycled-content mandates continue to steer demand for specialized, high-performance closures. At the same time, brand owners favor tethered, mono-material, and child-resistant solutions that align with circular-economy goals. Cost pressures from virgin-resin fees and climate-related supply disruptions push manufacturers to automate production and integrate recycled feedstocks, ensuring competitive resilience. Industry participants also pursue mergers and AI-enabled defect-inspection systems to enhance efficiency and secure scale advantages.

North America Plastic Caps And Closures Market Trends and Insights

Demand Surge for Bottled and Functional Beverages

Enhanced waters, relaxation mocktails, and caffeinated sports drinks continue to penetrate retail channels, lifting closure volumes beyond traditional hydration categories. Premium positioning drives investments in pressure-resistant, tamper-evident designs that preserve carbonation up to 4 volumes of CO2 while supporting brand shelf differentiation. Beverage formulators also require closures that protect sensitive nutraceutical ingredients and comply with U.S. Food and Drug Administration supplement labeling. In addition, Mexican consumer spending growth bolsters regional beverage production, amplifying unit demand for lightweight yet robust caps. Supply-chain reliability remains essential as manufacturers coordinate with fillers to deliver consistent torque and seal performance during high-speed bottling.

Brand-Owner Push for Tethered / E-commerce-Ready Closures

Direct-to-consumer shipping has made Amazon ISTA-6 compliance a gating requirement for personal-care and beverage launches. Brand owners therefore prioritize tethered formats that stay attached to the neck finish, mitigate leakage, and avoid cap loss inside shipping cartons. Aptar's Future Disc Top exemplifies this, pairing a secure lock with 100% polyethylene construction that simplifies curbside recycling. Grocery retailers likewise favor tethered designs because they streamline automated capping lines and cut downtime tied to cap-to-bottle mismatches. Patented hinge geometries now support multiple open-close cycles without compromising tamper evidence or consumer convenience.

Extended Producer Responsibility (EPR) Fees on Virgin Resin

California and three other states now levy producer-funded recycling fees that climb with virgin resin intensity, directly raising closure unit costs. Producers have begun shifting portfolios toward recycled or bio-based feedstocks to blunt fee exposure, yet the market supply of PCR polypropylene remains limited. Fee schedules differ by jurisdiction, complicating compliance for multi-state fillers, while reporting obligations create new administrative tasks. Smaller converters lacking regulatory staff face the greatest burden, potentially accelerating consolidation as they sell assets to scale players.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward PP Mono-Material Caps for Easier Recycling

- On-Line Pharma and Nutraceutical Boom Fuels CRC Demand

- Rise of Stand-Up Pouches with Fitments Replacing Screw Caps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyethylene retained the largest 41.98% slice of the plastic caps and closures market in 2025 on the back of cost efficiency and versatile processing. Nevertheless, polyethylene terephthalate marked the quickest advance at a 6.45% CAGR as brand owners linked sustainability pledges with single-polymer packaging streams. PET closures now leverage intrinsic recyclability and mature reclaim networks to close material loops in beverage and personal-care segments. Innovations in crystallinity control and additive packages lift heat-resistance, enabling hot-fill juices without sacrificing seal integrity. Origin Materials recently demonstrated polyester resin closures compatible with standard filling lines, signaling scale-ready alternatives for converters.

Manufacturers also explore post-consumer PET content targets of 25% to sidestep EPR levies, pushing demand for food-grade recycled pellets. Meanwhile, polypropylene holds ground in aggressive chemical and pharma uses because of superior stress-crack resistance. Bio-based polymers, though niche, gain regulatory attention where compostability mandates apply. Together, these shifts create a mosaic of material choices that hinge on total-cost-of-ownership and recyclability metrics.

Threaded formats, long the default due to universal neck compatibility, secured 46.85% share in 2025. Yet child-resistant closures outpaced all categories at 5.55% CAGR through 2031 as e-commerce pharmacies shipped increasing prescription volumes directly to consumers. Tightening FDA guidance now requires CRCs on certain over-the-counter nutraceutical powders, further broadening addressable volumes. Berry Global's selectively openable design illustrates ongoing R&D, merging dual-input safety with adult-friendly ergonomics.

Dispensing variants hold appeal in personal-care lotions and household cleaners where controlled flow minimizes waste. Snap-fit and press-on solutions remain useful in dairy products needing quick application and economical tooling. Across closure types, embedded QR codes supporting authenticity verification and recycling instructions emerge as value-added differentiators in direct-to-consumer channels.

The North America Plastic Caps and Closures Market Report is Segmented by Material (Polyethylene, PET, Polypropylene, and More), Type (Threaded, Dispensing, and More), End-User Industry (Beverage, Food, Pharmaceutical and Healthcare, Cosmetics and Toiletries, and More), Manufacturing Process (Injection Molding, Compression Molding, 3-D Printing, and More), and Geography. The Market Forecasts are Provided in Terms of Volume (Units).

List of Companies Covered in this Report:

- Silgan Holdings Inc.

- Amcor plc

- AptarGroup Inc.

- Closure Systems International Inc.

- TriMas Corporation

- Guala Closures SpA

- Tetra Pak Group

- O.Berk Company LLC

- BERICAP Holding GmbH

- Pano Cap Canada Ltd

- Erie Molded Plastics Inc.

- Crown Holdings Inc.

- Phoenix Closures Inc.

- Mold-Rite Plastics LLC

- Comar LLC

- Husky Technologies

- SACMI Imola S.C.

- Sonoco Products Company

- Plastipak Holdings Inc.

- Albea Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand surge for bottled and functional beverages

- 4.2.2 Brand-owner push for tethered / e-commerce-ready closures

- 4.2.3 Shift toward PP mono-material caps for easier recycling

- 4.2.4 On-line pharma and nutraceutical boom fuels CRC demand

- 4.2.5 AI-enabled in-line vision lowers defect rates and costs

- 4.3 Market Restraints

- 4.3.1 Extended Producer Responsibility (EPR) fees on virgin resin

- 4.3.2 Rise of stand-up pouches with fitments replacing screw caps

- 4.3.3 U.S./Canada rPET content mandates squeeze virgin PP demand

- 4.3.4 Beverage brand trials of aluminium crown re-seals

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Geopolitical Scenarios

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By Material

- 5.1.1 Polyethylene (PE)

- 5.1.2 Polyethylene Terephthalate (PET)

- 5.1.3 Polypropylene (PP)

- 5.1.4 Other Materials

- 5.2 By Type

- 5.2.1 Threaded

- 5.2.2 Dispensing

- 5.2.3 Unthreaded

- 5.2.4 Child-Resistant

- 5.3 By End-user Industry

- 5.3.1 Beverage

- 5.3.1.1 Bottled Water

- 5.3.1.2 Soft Drinks

- 5.3.1.3 Spirits

- 5.3.1.4 Other Beverages

- 5.3.2 Food

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Cosmetics and Toiletries

- 5.3.5 Household Chemicals

- 5.3.6 Other Industries

- 5.3.1 Beverage

- 5.4 By Manufacturing Process

- 5.4.1 Injection Molding

- 5.4.2 Compression Molding

- 5.4.3 3-D Printing / Rapid Prototyping

- 5.4.4 Other Manufacturing Process

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Silgan Holdings Inc.

- 6.4.2 Amcor plc

- 6.4.3 AptarGroup Inc.

- 6.4.4 Closure Systems International Inc.

- 6.4.5 TriMas Corporation

- 6.4.6 Guala Closures SpA

- 6.4.7 Tetra Pak Group

- 6.4.8 O.Berk Company LLC

- 6.4.9 BERICAP Holding GmbH

- 6.4.10 Pano Cap Canada Ltd

- 6.4.11 Erie Molded Plastics Inc.

- 6.4.12 Crown Holdings Inc.

- 6.4.13 Phoenix Closures Inc.

- 6.4.14 Mold-Rite Plastics LLC

- 6.4.15 Comar LLC

- 6.4.16 Husky Technologies

- 6.4.17 SACMI Imola S.C.

- 6.4.18 Sonoco Products Company

- 6.4.19 Plastipak Holdings Inc.

- 6.4.20 Albea Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment