PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906922

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906922

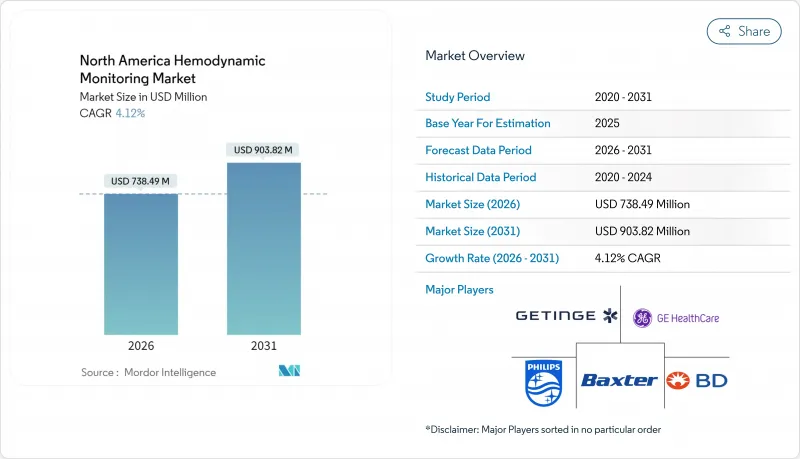

North America Hemodynamic Monitoring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The North America hemodynamic monitoring market size in 2026 is estimated at USD 738.49 million, growing from 2025 value of USD 709.26 million with 2031 projections showing USD 903.82 million, growing at 4.12% CAGR over 2026-2031.

This trajectory reflects hospital consolidation, reimbursement tied to quality, and the rapid integration of AI-enabled analytics that transform pressure or flow values into actionable predictions. Vendor platforms now bundle hardware, software, disposables, and cloud subscriptions, giving health systems a predictable total cost of ownership. A swift pivot toward minimally invasive or wearable sensors reduces infection risk and broadens usage beyond the intensive-care unit, while Medicare's remote-monitoring codes help preserve capital spending even as operating budgets tighten.

North America Hemodynamic Monitoring Market Trends and Insights

AI-Driven Clinical Decision-Support in ICUs

Predictive algorithms are turning hemodynamic monitoring from reactive measurement into proactive therapy. Edwards Lifesciences' Hypotension Prediction Index (HPI) shows 83% sensitivity and specificity in flagging intraoperative hypotension up to 15 minutes in advance, cutting time-weighted average hypotension by 85% versus standard care. Early trials report shorter ICU stays and better renal metrics, yet clear mortality benefit remains elusive, leaving space for next-generation platforms that fuse prediction with closed-loop drug titration. The U.S. Food and Drug Administration now classifies adjunctive cardiovascular indicators under 21 CFR 870.2200, providing an explicit path for AI-rich software modules. These clearances accelerate adoption and keep the North America hemodynamic monitoring market on a technology refresh cycle.

Growing Prevalence of Heart-Failure & Critical-Care Admissions

An aging population pushes heart-failure prevalence upward and boosts demand for continuous pressure trending. Meta-analysis of three randomized trials with over 1,500 patients found implantable hemodynamic monitors cut mortality by 25% (HR 0.75) and heart-failure hospitalizations by 36% (HR 0.64). Cost-effectiveness modeling shows remote pressure monitoring saves USD 6,723 per patient over five years by avoiding readmissions. Such evidence underpins Medicare's decision to reimburse remote physiologic monitoring, propelling shipments and cementing the North America hemodynamic monitoring market as an RPM cornerstone.

Shortage of Critical-Care Nurses Trained on Advanced Monitors

Turnover exceeding 25% at community hospitals forces continuous retraining and slows deployment of sophisticated consoles. Needs assessments show gaps in waveform interpretation and equipment setup that undermine monitoring accuracy. Vendors counter with color-coded dashboards, context-aware alarms, and embedded tutorials, yet staffing imbalances continue to dampen the North America hemodynamic monitoring market CAGR by an estimated 0.6 percentage point.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Ambulatory / Home Hemodynamic Programs

- Favorable U.S. Reimbursement via Bundled-Payment Incentives

- High Device & Disposable Costs for Smaller Hospitals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hemodynamic Monitoring Systems secured 56.12% of the North America hemodynamic monitoring market in 2025, underscoring buyers' preference for end-to-end ecosystems calibrated for ICU workflows. Although unit growth is modest, steady disposable pull-through keeps vendors' service revenue intact. The North America hemodynamic monitoring market size for systems should slip from USD 401.1 million in 2026 to USD 382.9 million by 2031 as hospitals stretch replacement cycles; however, AI software upgrades and cybersecurity modules will buoy margins.

Sensors, rising at a 4.98% CAGR, represent the innovation vanguard. Miniaturized optical or impedance sensors integrate directly with telemetry patches, opening chronic-care and ambulatory channels. Terumo's CDI OneView, which displays 22 parameters in the OR, illustrates convergence of high acuity and multi-metric analytics. As algorithms perfect signal quality under motion or low perfusion, sensor makers are primed to lift their slice of the North America hemodynamic monitoring market share.

Cardiac Output remains the backbone at 39.12% share thanks to clinician familiarity and robust procedural coding. Non-invasive pulse-contour and bioreactance platforms offset declining catheter use, sustaining spending across ICUs and cath labs. Oxygen Saturation Monitoring, however, shows a 5.43% CAGR as multi-wavelength probes extend utility to tissue oximetry and venous saturation. Masimo's rainbow SET drove healthcare revenue to USD 372 million in Q1 2025, validating appetite for broadened non-invasive diagnostics. Pressure and volume indices persist as clinical staples, but the real differentiation lies in composite scores that synthesize multiple parameters into single actionable numbers, reducing cognitive load amid nurse shortages.

The North America Hemodynamic Monitoring Market Report is Segmented by Product Type (Hemodynamic Monitoring Systems, Catheters, Sensors, Disposables & Accessories), Monitoring Type (Cardiac Output, Pressure, Volume, Oxygen Saturation, Others), End User (Hospitals, Cath Labs, Ascs, Home-Care, Others), and Geography (United States, Canada, Mexico). Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Edwards Lifesciences Corp.

- Baxter

- ICU Medical

- GE HealthCare Technologies Inc.

- Koninklijke Philips

- Getinge

- Nihon Kohden Corp.

- Mindray Bio-Medical Electronics Co. Ltd.

- Terumo Corp.

- Medtronic

- Masimo Corp.

- Osypka Medical

- CNSystems Medizintechnik GmbH

- Dragerwerk

- Deltex Medical Group plc

- Tensys Medical

- Merit Medical Systems

- Beckton Dickinson

- Retia Medical LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing adoption of minimally-invasive monitoring platforms

- 4.2.2 Growing prevalence of heart-failure & critical-care admissions

- 4.2.3 Expansion of ambulatory / home hemodynamic programmes

- 4.2.4 Favourable US reimbursement via bundled-payment incentives

- 4.2.5 AI-driven clinical decision-support in ICUs

- 4.2.6 Hospital shift toward outcome-based purchasing models

- 4.3 Market Restraints

- 4.3.1 Shortage of critical-care nurses trained on advanced monitors

- 4.3.2 High device & disposable costs for smaller hospitals

- 4.3.3 Measurement-accuracy issues in obese / arrhythmic patients

- 4.3.4 Data-interoperability gaps across multi-vendor equipment

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Hemodynamic Monitoring Systems

- 5.1.1.1 Invasive Systems

- 5.1.1.2 Minimally Invasive Systems

- 5.1.1.3 Non-Invasive Systems

- 5.1.2 Hemodynamic Monitoring Catheters

- 5.1.3 Hemodynamic Monitoring Sensors

- 5.1.4 Disposables & Accessories

- 5.1.1 Hemodynamic Monitoring Systems

- 5.2 By Monitoring Type

- 5.2.1 Cardiac Output Monitoring

- 5.2.2 Pressure Monitoring

- 5.2.3 Volume Monitoring

- 5.2.4 Oxygen Saturation Monitoring

- 5.2.5 Others

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Cath Labs & Interventional Centers

- 5.3.3 Ambulatory Surgical Centers

- 5.3.4 Home-Care Settings

- 5.3.5 Other End Users

- 5.4 By North America

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Edwards Lifesciences Corp.

- 6.3.2 Baxter International Inc.

- 6.3.3 ICU Medical Inc.

- 6.3.4 GE HealthCare Technologies Inc.

- 6.3.5 Koninklijke Philips N.V.

- 6.3.6 Getinge AB

- 6.3.7 Nihon Kohden Corp.

- 6.3.8 Mindray Bio-Medical Electronics Co. Ltd.

- 6.3.9 Terumo Corp.

- 6.3.10 Medtronic plc

- 6.3.11 Masimo Corp.

- 6.3.12 Osypka Medical GmbH

- 6.3.13 CNSystems Medizintechnik GmbH

- 6.3.14 Dragerwerk AG & Co. KGaA

- 6.3.15 Deltex Medical Group plc

- 6.3.16 Tensys Medical Inc.

- 6.3.17 Merit Medical Systems Inc.

- 6.3.18 Becton, Dickinson and Company

- 6.3.19 Retia Medical LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment