PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907325

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907325

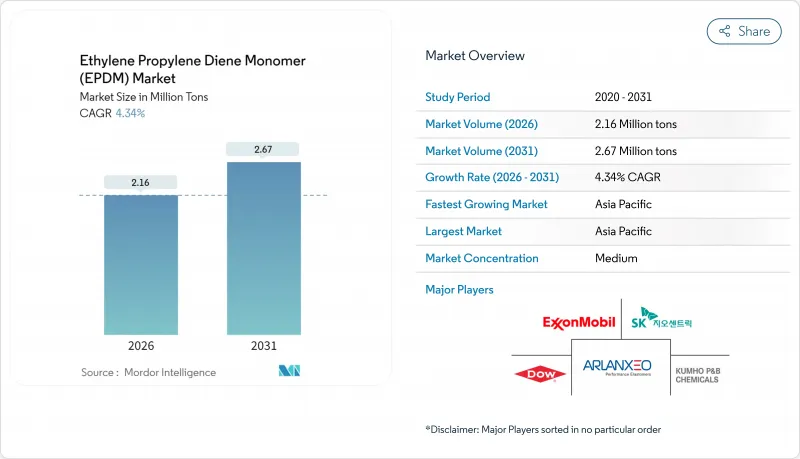

Ethylene Propylene Diene Monomer (EPDM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Ethylene Propylene Diene Monomer Market was valued at 2.07 million tons in 2025 and estimated to grow from 2.16 million tons in 2026 to reach 2.67 million tons by 2031, at a CAGR of 4.34% during the forecast period (2026-2031).

Demand momentum is tied to electric-vehicle battery sealing, net-zero roofing membranes, and early hydrogen fuel cell adoption, all of which reward EPDM's thermal stability up to 150 °C and outstanding ozone resistance. Competitive positioning increasingly hinges on bio-based feedstocks and advanced catalysts that lower carbon footprints without compromising polymer properties. Regional supply security, particularly abundant propylene integration in Asia-Pacific, underpins volume leadership and buffers cost volatility risks. Feedstock price swings and rising thermoplastic vulcanizate (TPV) penetration pose cost and substitution pressures, yet differentiated EPDM grades continue to defend premium applications where dielectric stability, chemical resistance, and lifecycle durability are non-negotiable.

Global Ethylene Propylene Diene Monomer (EPDM) Market Trends and Insights

Surging Demand for EPDM Roofing Membranes in Net-Zero Buildings

EPDM membranes deliver service lives exceeding 50 years, giving developers a favorable cost-in-use equation against shorter-lived thermoplastics. White-colored formulations reflect solar radiation, helping projects achieve energy-efficiency credits under LEED and BREEAM schemes. Independent European reviews consistently rank EPDM's environmental impact lower than TPO or PVC alternatives, strengthening specification preference in climate-resilient construction. Growing urban heat-island mitigation codes increase demand for reflective roofs, while the material's chemical inertness supports rainwater harvesting and green-roof assemblies. Compatibility with photovoltaic mounting systems further raises adoption prospects in retrofits and new builds that seek combined energy and water performance benefits.

Accelerated EV Production Boosting Seals and Gaskets Demand

Electric-vehicle batteries require gaskets that withstand thermal cycling between -55 °C and +150 °C, remain elastic under vibration, and endure exposure to coolant glycols and fire-retardant additives. EPDM's low compression set protects pack integrity and limits moisture ingress, directly supporting battery warranty targets. Higher-voltage vehicle architectures make dielectric performance critical, and EPDM offers stable insulation in the 800-V systems now moving to mass production. Asia-Pacific remains the epicenter of demand growth due to China's dominant cell manufacturing base and Korea's high-capacity seal producers. Automakers are trialing TPVs to cut weight and aid recyclability, but EPDM still holds the performance edge in under-hood environments where temperatures and chemical exposure exceed TPV limits.

Volatile Crude-Oil-Linked Feedstock Prices

Propylene and ethylene price spikes driven by refinery shutdowns and tight olefin balances erode EPDM profit margins. U.S. polymer-grade propylene spot prices climbed in 2025 on the heels of refinery rationalizations and new polypropylene capacity additions. Asian ethylene values have displayed double-digit percentage swings within months, complicating contract negotiations and inventory planning for tire and gasket producers. Integrated EPDM suppliers with captive crackers partially offset the risk, but merchant producers often absorb margin compression or cede share to substitute materials in cost-sensitive applications.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory 5G Infrastructure Roll-outs Requiring Weather-Resistant Cables

- Hydrogen Fuel-Cell Infrastructure Needs High-Temperature Elastomers

- Competition from Thermoplastic Polyolefin Elastomers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solution polymerization delivered 59.10% of the EPDM market size in 2025 as automakers and roof-membrane fabricators paid premiums for tight molecular-weight control essential to compression-set performance. The process allows precise diene incorporation, giving compounders latitude to tailor cure speed and elasticity for demanding battery gasket profiles. Recent catalyst breakthroughs, such as ARLANXEO's Keltan ACE titanium κ1-amidinate complex, reduce energy consumption, trimming unit production costs without altering downstream compounding recipes.

Slurry/suspension routes, projected to climb at a 4.78% CAGR, are capturing commodity grades for hose and cable insulation as operators retrofit reactors with higher-efficiency agitation systems that cut solvent use. Gas-phase technology remains niche but draws interest for ultra-high molecular-weight grades used in specialty compression seals.

The Ethylene Propylene Diene Monomer (EPDM) Report is Segmented by Manufacturing Process (Solution Polymerization Process, Slurry/Suspension Process, and Gas-Phase Polymerization Process), Application (Automotive, Building and Construction, Manufacturing, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific represented 56.05% of the EPDM market size in 2025, buoyed by Chinese battery-electric vehicle production and Korean capacity expansions such as Kumho Polychem's 220,000-ton site. Regional growth at 4.58% CAGR is supported by ample propylene supply from integrated crackers and steam-cracking complexes, reducing feedstock risk and freight cost. Localization strategies by global seal suppliers shorten lead times for EV manufacturers, creating a virtuous cycle of technical support and demand concentration.

North America's market is growing as Detroit automakers accelerate EV roll-outs and commercial roofing contractors specify EPDM for retrofit energy-efficiency upgrades. Domestic crackers face intermittent propylene tightness, but shale-gas economics continue to encourage olefin investment that promises more stable downstream pricing over the medium term. Federal tax incentives for clean-energy buildings are catalyzing new warehouse roof installations, further underpinning EPDM consumption.

Europe commands a premium application share driven by stringent environmental regulations that favor materials with demonstrated lifecycle benefits. Circular-economy directives encourage in-house devulcanization lines, giving regional compounders a head start in recycled-content EPDM blends. The Middle East and Africa, though smaller, show infrastructure-driven demand recovery, while South America's uptake hinges on petrochemical investment cycles in Brazil and nearby propylene supply. Across all regions, the shift toward higher-voltage power systems and climate-resilient infrastructure favors EPDM's performance attributes, sustaining worldwide consumption even amid feedstock volatility.

- ARLANXEO

- Carlisle Companies Inc.

- Dow

- ENEOS Materials Corporation

- Exxon Mobil Corporation

- Goodyear Rubber Company

- Kumho P&B Chemicals (Kumho Polychem)

- LANXESS

- Lion Elastomers

- Mitsui Chemicals Inc.

- SABIC

- SK geocentric Co., Ltd.

- Versalis S.p.A

- West American Rubber Company LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for EPDM Roofing Membranes in Net-Zero Buildings

- 4.2.2 Accelerated EV Production Boosting Seals and Gaskets Demand

- 4.2.3 Mandatory 5G Infrastructure Rollouts Requiring Weather-Resistant Cables

- 4.2.4 Hydrogen Fuel-Cell Infrastructure Needs High-Temperature Elastomers

- 4.2.5 Circular-Economy Push for EPDM Reclaim and Devulcanization

- 4.3 Market Restraints

- 4.3.1 Volatile Crude-Oil-Linked Feedstock Prices

- 4.3.2 Competition from Thermoplastic Polyolefin Elastomers

- 4.3.3 Carbon-Intensity Scrutiny of Petro-Based Polymers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Manufacturing Process

- 5.1.1 Solution Polymerization Process

- 5.1.2 Slurry/Suspension Process

- 5.1.3 Gas-phase Polymerization Process

- 5.2 By Application

- 5.2.1 Automotive

- 5.2.2 Building and Construction

- 5.2.3 Manufacturing

- 5.2.4 Electrical and Electronics

- 5.2.5 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Spain

- 5.3.3.7 Turkey

- 5.3.3.8 NORDIC Countries

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 Nigeria

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ARLANXEO

- 6.4.2 Carlisle Companies Inc.

- 6.4.3 Dow

- 6.4.4 ENEOS Materials Corporation

- 6.4.5 Exxon Mobil Corporation

- 6.4.6 Goodyear Rubber Company

- 6.4.7 Kumho P&B Chemicals (Kumho Polychem)

- 6.4.8 LANXESS

- 6.4.9 Lion Elastomers

- 6.4.10 Mitsui Chemicals Inc.

- 6.4.11 SABIC

- 6.4.12 SK geocentric Co., Ltd.

- 6.4.13 Versalis S.p.A

- 6.4.14 West American Rubber Company LLC

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment