PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907340

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907340

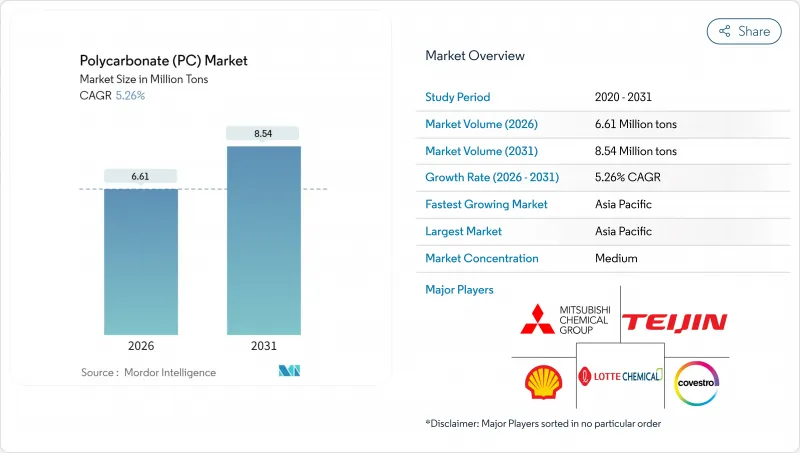

Polycarbonate (PC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Polycarbonate Market is expected to grow from 6.28 million tons in 2025 to 6.61 million tons in 2026 and is forecast to reach 8.54 million tons by 2031 at 5.26% CAGR over 2026-2031.

Demand accelerates as polycarbonate replaces heavier or less durable materials in electric vehicles, 5G infrastructure, and mini-LED displays, while remaining resilient to economic fluctuations due to its impact resistance, optical clarity, and thermal stability. Investments such as SABIC-SINOPEC's 260,000 tpa joint venture in China and Lotte Chemical's USD 3.9 billion Cilegon complex add supply security and lower logistics costs in Asia. North America and Europe follow as regulation-driven buyers; the EU Construction Products Regulation requires flame-retardant facades that favor polycarbonate's inherent fire resistance. Despite raw material cost swings and scrutiny of bisphenol-A, technology upgrades, renewable feedstock grades, and backward integration protect producer margins and sustain growth.

Global Polycarbonate (PC) Market Trends and Insights

Mainstream EV Demand in Automotive Glazing

Rapid electric-vehicle adoption is lifting the polycarbonate market as OEMs replace glass with lightweight transparent panels that cut 40-50% mass and extend driving range. Covestro's UV-stable grades maintain clarity for over a decade, which resolves earlier yellowing issues and encourages panoramic roof integration. Tesla's Model S Plaid illustrates the benefit with a 15 kg weight reduction from polycarbonate roof panels. Design evolution toward autonomous cabins increases glazed surface area, escalating demand for materials that host antennas, heaters, and sensors without losing structural strength. Asian battery-electric platforms targeting 500 km range now specify up to 6 m2 of polycarbonate glazing per vehicle, reinforcing the segment's pull on overall polycarbonate market volumes.

Consumer Electronics Mini-LED Diffusion Lenses

Mini-LED panels require thousands of lenslets per screen, each precision-molded in polycarbonate to maintain uniform luminance across sub-200 µm pixels. Samsung's 2025 flagship televisions use textured polycarbonate optics that raise light extraction by 12% versus legacy LED backlights. Apple's MacBook Pro adoption signals cross-device acceptance, and every 65-inch display consumes roughly 25,000 lenslets, creating large incremental tonnage for the polycarbonate market. Thermal stability from -20 °C to 85 °C ensures refractive-index consistency, while high-fill cavity molding cuts takt time and waste. Component miniaturization centers activity in Korea, Taiwan, and mainland China, but North American fabs are scaling to secure regional supply resilience.

Bisphenol-A Regulatory Scrutiny

The European Food Safety Authority's 2024 guidance slashed tolerable daily BPA intake, excluding polycarbonate from most direct food-contact products. California's Proposition 65 labels broaden consumer awareness, pushing retailers to favor BPA-free alternatives. Medical-device tenders now request BPA-free certification, raising formulation costs for specialty grades yet protecting premium margins once certified. Packaging losses temper overall polycarbonate market growth, but producers are accelerating bio-based bisphenol substitutes and depolymerization recycling to regain food-grade channels.

Other drivers and restraints analyzed in the detailed report include:

- 5G Infrastructure Radomes and Antenna Covers

- Accelerating Adoption of Energy-Efficient LED Lighting Optics

- Volatile Phenol-Acetone Feedstock Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electrical and Electronics held 36.32% of the polycarbonate market share in 2025 and is forecast to log a 6.75% CAGR through 2031, reflecting its position as both volume anchor and innovation hub. Semiconductor cleanrooms need low-outgassing parts, while mini-LED optics and 5G transceiver bodies demand heat tolerance and RF transparency. The CHIPS Act funds of USD 52 billion stimulate the construction of new wafer fabs, each requiring thousands of PC filtration housings and tooling covers.

Automotive ranks second as electrified platforms adopt lightweight right-size glazing and battery enclosures. OEMs value polycarbonate's sensor compatibility for advanced driver assistance systems. The building and Construction Sector shows steady uptake because the EU CPR favors flame-retardant panels. Packaging remains niche outside BPA-restricted regions, with a focus on five-gallon water bottles and microwave-safe containers. Industrial machinery, aerospace, and medical devices complement diversified demand, ensuring that the polycarbonate market is not reliant on a single downstream sector.

The Polycarbonate Market Report is Segmented by End-User Industry (Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging, and Others), Product Type (Sheet, Film, and Other Product Types), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Geography Analysis

Asia-Pacific controlled 64.10% of the polycarbonate market in 2025 and is projected to expand at a 5.61% CAGR to 2031. China's electronics clusters in the Yangtze and Pearl River Deltas consume specialty grades, while domestic producers such as Rongsheng add 520,000 tpa capacity to balance imports. Japan pioneers optical-grade formulations for camera lenses, and South Korea channels demand from smartphone and EV battery giants. India's Production-Linked Incentive scheme spurs the localized production of LED luminaires and white goods, thereby increasing regional consumption.

North America ranks second, driven by EV production in the Midwest and the construction of new chip fabs in Arizona and Texas. Covestro invested a low triple-digit million euros in Ohio to compound thermally conductive grades for charging stations and 5G modules. Mexico benefits from near-shoring as appliance and auto wire-harness suppliers migrate from Asia.

Europe buys polycarbonate for premium vehicles, medical devices, and flame-retardant facade panels. Germany leads volume, while France and Italy adopt thin-wall PC for smart-meter enclosures. EU CPR rules encourage replacement of combustible plastics with self-extinguishing grades. South America and the Middle East & Africa remain small but strategic; Brazil's automotive rebound and Gulf mega-projects in Riyadh and Dubai present pockets of growth that may justify future resin warehouses or compounding lines.

- Axxicon B.V.

- CHIMEI

- Covestro AG

- Formosa Chemicals & Fibre Corp.

- Idemitsu Kosan Co., Ltd.

- LG Chem

- LOTTE Chemical Corporation

- Luxi Chemical Group

- Mitsubishi Chemical Group Corporation

- RTP Company

- SABIC

- Samtion Chemical

- Samyang Corporation

- TEIJIN LIMITED

- Trinseo PLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream EV demand in automotive glazing

- 4.2.2 Consumer-electronics mini-LED diffusion lenses

- 4.2.3 5G infrastructure radomes and antenna covers

- 4.2.4 Accelerating adoption of energy-efficient LED lighting optics

- 4.2.5 EU CPR-mandated flame-retardant facades

- 4.3 Market Restraints

- 4.3.1 Bisphenol-A regulatory scrutiny

- 4.3.2 Volatile phenol-acetone feedstock pricing

- 4.3.3 OEM substitution toward bio-based copolyesters

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Import and Export Analysis

- 4.7 Price Trends

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of Substitutes

- 4.8.4 Competitive Rivalry

- 4.8.5 Threat of New Entrants

- 4.9 End-use Sector Trends

- 4.9.1 Aerospace (Aerospace Component Production Revenue)

- 4.9.2 Automotive (Automobile Production)

- 4.9.3 Building and Construction (New Construction Floor Area)

- 4.9.4 Electrical and Electronics (Electrical and Electronics Production Revenue)

- 4.9.5 Packaging(Plastic Packaging Volume)

- 4.10 Recycling Overview

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By End-user Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 By Product Type

- 5.2.1 Sheet

- 5.2.2 Film

- 5.2.3 Other Product Types

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 Australia

- 5.3.1.6 Malaysia

- 5.3.1.7 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 Canada

- 5.3.2.2 Mexico

- 5.3.2.3 United States

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 Italy

- 5.3.3.4 United Kingdom

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Nigeria

- 5.3.5.4 South Africa

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share** (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Axxicon B.V.

- 6.4.2 CHIMEI

- 6.4.3 Covestro AG

- 6.4.4 Formosa Chemicals & Fibre Corp.

- 6.4.5 Idemitsu Kosan Co., Ltd.

- 6.4.6 LG Chem

- 6.4.7 LOTTE Chemical Corporation

- 6.4.8 Luxi Chemical Group

- 6.4.9 Mitsubishi Chemical Group Corporation

- 6.4.10 RTP Company

- 6.4.11 SABIC

- 6.4.12 Samtion Chemical

- 6.4.13 Samyang Corporation

- 6.4.14 TEIJIN LIMITED

- 6.4.15 Trinseo PLC

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

8 Key Strategic Questions for CEOs